When it comes to the metals, bears hibernate for years, but bulls just retest the 5- and 50-day moving averages! This week's retail sales data will be critical... New figures for CPI and PPI will also be watched closely. Given the delicate balance of forces and the high level of emotion in this market, any surprise in these numbers is likely to set off a big move... Either way, metals have still not failed the support levels consistently outlined in this update over the past several weeks and highlighted ... until they do, the outlook will remain decidedly bullish, even if a sustained rally is still always just over the horizon. ~ Precious Points, Don't Go Gentle Into That Goodnight, June 10, 2007

So Goldilocks is back, but where's gold? Stocks are sailing again, how about silver?

A few weeks ago this update proclaimed that to return to its glory days, gold would need a rebound in the U.S. economy and an uptick in inflation. The rebound happened, and aside from the consequences eventuated by a rapid adjustment in bond yields, precious metals appear to have their sites on higher price levels. The perpetual show of support at the 50-day moving average continues to be the pleasant manifestation of a positive fundamental picture, as well as a profitable trade ... but metals aren't out of the woods yet!

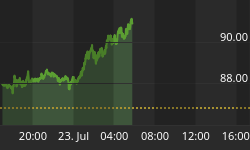

The charts below show that, despite the broad market rally, gold and silver failed to close above their 5-day moving averages, the key level watched by this update in recent weeks. This obvious resistance level will be the first obstacle to a sustained rally, followed by even stronger resistance further overhead if it's breached.

The addition of $6 billion by the NY Fed during another week of heavy maturation evidences the growing demand for base money, though the trend in supply of sloshing funds is still down for the month. Look for a reversal of this trend as an early indicator of a rally in the metals, though last week's tame inflation figures do not portend a surge to new highs in the short term.

What does appear to be coming in the future is higher interest rates. Alan Greenspan, one of the more high profile figures articulating this consensus recently played down concerns that the Chinese would dump U.S. Treasuries, which would obviously produce a catastrophic surge in bond yields. Much more insidious and highly likely is that, despite the dead cat bounce in bond prices, China and other sovereign holders of U.S. debt will buy fewer and fewer U.S. bonds going forward and this will create an upward bias in yields. Referring to the global liquidity boom which he traced back to the end of the Cold War, Greenspan was quoted to have said, "Enjoy it while it lasts."

Clearly the former head of the Fed is referring to the fact that even though domestic rates have held steady, the trend in global rates has certainly been higher. The news that China was a net seller of U.S. Treasuries in April was no surprise, as they'd already publicly announced the change in their foreign reserve strategy away from U.S. Treasuries and this lack of demand has already been a major contributing factor to weak Treasury auctions and higher interest rates. Syria and Kuwait ending their currency board pegs to the dollar didn't help matters. It used to be that countries raced to devalue their currencies to gain a short lived competitive trade advantage. It now seems we've moved to an era where countries compete for much needed foreign investment through strong currencies and higher returns for bond holders.

It certainly seems the Fed would like to raise rates to keep the dollar and U.S. securities competitive with the likes of Germany, Britain, and this is consistent with Bernanke's desire to foist responsibility for domestic housing on the NGO's. Maybe housing and subprime aren't bad enough to force a cut, but growth is not robust enough and inflation not rampant enough to force a hike - and those other problems would only become much worse in a rate hiking environment. Perhaps it is that the stronger dollar and higher rates coupled with the stronger data attracted some new buying from some of these parties. There's no denying, however, that the direction of the trend is away from financing the U.S. debt through purchase of Treasuries and that this is the main reason for the spike in interest rates and even though this has lately tended to support the dollar, will ultimately reverse and sink the greenback as deficits grow.

That the evaporation of rate cut expectations, as well as these other forces, are responsible for the ramping up of interest rates is consistent with the fact that TIPS spreads still do not indicate increased inflation concerns despite the rise. A potential threat to intermediate term metals prices is that an inflation surge now will cause a further spike in bond yields, resulting in an equity selloff and at least a soft patch in metals. Though current core inflation is hovering at the high end of the Fed's acceptable range, headline inflation, which is widely believed to more closely reflect reality than the Fed's cherry-picked data and focus on price inflation, suggests inflation is rampant and worsening. And ultimately, even the Fed, by its own admission, is committed to money supply inflation, just not too much, too fast.

So as we continue to tread water in what was expected to be a period of ennui in the metals markets, we'll continue to monitor key support and resistance levels, as well as moves in the bond markets and trends in the Fed's open market activities. Probably most valuable of all, however, are the trend cycle charts, forums, and realtime chatrooms available only to TTC members. The current subscription fee of $50/month is only available for two more weeks until prices go up ... yet another sign of very real inflation!!