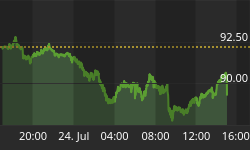

There is widespread belief that gold's recent non-performance was attributable to a stronger dollar, stock market rally, and/or central bank manipulation. While it is true that gold's rise was tempered by the bounce in the US dollar, we believe that gold's nonperformance was attributable more to the fact that gold and gold shares were the only place where there were profits. In fact, our studies show that in the long term, gold is influenced not by transient factors such as central bank musings, but rather as a store of value when investors lack confidence in financial assets. Currently, gold is mired in a tight trading range of $305 to $318 an ounce. After recording a 2½-year high at $330 in June, the pullback is simply a normal correction process. We believe that gold is about to breakout of this trading range and is in the nascent stage of a multi-year bull market driven by a declining US dollar, global bear market and Middle East geo-political tensions.

The Dollar Standard

For thousands of years, gold has been an integral part of the world's monetary system, providing the backing for money. Gold financed wars and subsequently the rebuilding of those countries. Gold formed the basis for the international monetary system from 1946 to 1971. In the era of the gold standard, gold was a reserve asset and central bankers were forced to adhere to financial discipline. Despite public sales, gold is still the second largest reserve asset held by central banks. The last vestiges of the gold standard disappeared when Nixon severed the link in 1971 and in the process devalued the dollar, ending the right to demand gold for dollars. Gold and the dollar were worth whatever the financial markets say they are. Exchange rates were allowed to float and the US dollar became the underlying standard for many countries.

During the subsequent two decades of floating exchange rates, the powerful US economy kept the dollar strong and gold prices low. Gold declined as US dollars were created in abundance without the need for 100 percent backing or redeemability. An excess of monetary stimulus such as eleven interest rate reductions within a year and a half and double-digit monetary base growth also caused a glut of dollars. Ironically, most of those dollars ended up on the balance sheets of foreign central banks, because they too wanted part of the American dream. The US dollar reached a fifteen-year high and dollarization became the norm.

Through the issuance of so many dollars, the greenback became the largest asset class held by the world's central banks. This allowed the United States to create the world's biggest bubble and accumulate one of the world's greatest debts. The rise and fall of America's financial strength has left them with too much capacity, too much debt and an economic engine that refuses to turnover. The Americans must now finance a record $450 billion current account deficit and a near record $200 billion budgetary deficit with almost zero interest rates. It took time, but foreigners are now tired of financing America's twin deficits. So far, the flight from the dollar has been orderly but there is no guarantee that it will continue. At some point the dollar collapse will crack the veneer of complacency and lead to a crisis of confidence in the markets. We are concerned that the exodus could escalate since this mountain of foreign-owned dollar securities is extremely vulnerable.

The slide in the US dollar comes at an awkward time for policymakers. With a declining dollar, the pressure on the Fed to maintain a sound money policy whilst providing the liquidity to rebuild the economy, raises the inevitable "guns and butter" question. The Fed has created unprecedented amounts of new liquidity in order to soften the impact of the deflationary debt levels without creating real value in the economy. Further, with the Fed keeping interest rates low, it signals that it will continue to subsidize the American way of life with twin deficits. The prospect of another slide or debasement of the dollar lessens the appeal of holding dollars as sound money. Yesterday the dollar's strength dampened inflation; today a falling dollar will revive it and that's hardly a rosy outcome for world financial markets coping with mammoth US deficits. Inflation is caused by the erosion of a currency's value when too much money chases too few goods. It can happen again. And what is to fill the vacuum left by the dollar? Gold, of course. After all it has worked for the last few thousand years. In the new world where markets are secondary to government actions, where markets are illiquid and capital is scarce, we expect gold to regain its status as a store of value. "Sooner or later", wrote Robert Louis Stevenson, "we sit down to a banquet of consequences".

The New Money

Dollarization is disappearing. After Mexico in 1994, East Asia in 1997, Russia in 1998 and Brazil in 1999, the full faith and credit of the United States is under scrutiny. The malaise that spread to Latin America is just beginning. More recently the Argentinean collapse and the $30 billion IMF bailout for Brazil has lessened the appeal of dollarization. Volatility in the financial markets, an over-valued and over-owned US dollar and forty-year low interest rates have forced central banks to diversify their portfolios from dollars, prompting them to buy euros and gold instead.

The Bank of China recently raised its gold reserves to 500 tons, which is only 2 percent of total reserves. Asian central banks hold between 1 and 5 percent of their foreign exchange reserves in gold, while European central banks hold 30 to 40 percent and the US at 55 percent. With over half of the world's foreign exchange reserves in Asian vaults, they are the next big buyers of gold. Japanese investors to date have bought more than 60 tons or three times more than in the first seven months of last year. In a subtle announcement, Malaysia and a handful of other Islamic countries plan to use gold dinars to settle bilateral trade from mid 2003 so as to reduce reliance on the US dollar.

According to Islamic law, gold dinars have a specific wealth of gold equivalent to 4.22 grams of pure gold and its value is around $42(US). To be sure, the trillion-dollar lawsuit against the Saudis in the United States will accelerate this trend. It has been reported that since 9/11, Middle East investors sold up to $200 billion of US assets of an estimated $1.2 trillion in dollar securities.

With the economic case for a strong dollar gone, and little room for fiscal stimulus, we believe that we are on a threshold of a lower dollar, stocks and bonds. Gold is a winner in this environment and cannot be printed, does not default, or threaten to default. The lack of confidence in the financial system and the specter of another Iraqi war are pushing gold prices up. Investors are seeking an alternative and gold has emerged, not only as a store of value but also as a new standard. Indeed our bullishness has been based upon the overdue decline of fiat money and the reestablishment of gold's role as the basis for a monetary standard in a world lacking an anchor. Gold cannot be created like fiat money. Even Fed Chairman, Alan Greenspan called gold, "the ultimate form of payment in the world".

Gold- the Alternate Asset Class

Throughout history, gold has reacted inversely to other asset classes including the Dow Jones Industrial and the S&P 500. Gold will become an important part of a balanced portfolio. It is the safest possible asset, its intrinsic value unaffected by central bank musings or the world's politicians. As the US dollar falls, the gold price usually rises. The prospect of years of recovery from the bubble years suggests gold is a good alternative to stocks and the dollar. In 1985, the US dollar fell 35 percent against a basket of currencies. Gold went up 66 percent from $300 to over $500 per ounce in the same period. To date, gold's performance is up over 14 percent, better than an 11 percent decline in the Dow Jones, 18 percent fall in the S&P 500 and outperforming other currencies this year. We believe gold has begun its second leg of a multi-year bull market that will see $375 per ounce near term and $510 per ounce next year. Gold has finally reasserted itself as a savings and investment vehicle and will appreciate further against under-performing currencies, bonds and stocks.

Gold's return to a safe haven role caused Morgan Stanley's global strategist, Barton Biggs, to recently advocate a 5% weighting in portfolios. Biggs wrote, "this large differential could only be solved by much higher prices, the point is that, it is not inflation or deflation that is the principle driver of gold, but the return from other long-term financial assets, particularly equities." Mr. Bigg's view is that capital returns reached a zenith a year and half ago, and the stock and bond outlook will lag that of gold.

Debt, debt and too much debt

Today, personal savings are too low, and corporate and household debts are too high. Mortgage debt stands at 7 percent of household discretionary income. Debt problems are of concern as consumer credit outstanding rose at 5.9 percent annual rate in June. Household, corporate and credit debt is now almost $30 trillion or 2.9 times GDP. There are also increased numbers of consumers defaulting. For example, the shares of Capital One, the US credit card group tumbled 40 percent after Federal regulators ordered it to increase its reserves by $240 million, to cover potentially bad loans. Credit card companies wrote off $4.9 billion in bad debt in the first quarter of this year, up from $2.6 billion during the same period, according to the Federal Deposit Insurance Corporation (FDIC).

The rise and fall of the telecoms have overshadowed the dotcom crash. Telecom debts exceed $1 trillion. And, the industry is at the center of the accounting scandals following WorldCom's bankruptcy, the biggest in corporate history. As in Japan, the telecom debacle will take years to recover and the hangover consequences must be dealt with. First, the oversupply of capacity built during the bubble years must be brought inline with demand and second, the mountain of debt must be reorganized. History shows that a prolonged period of uncertainty looms, as the excesses in the system in capacity, consumption and debt is worked down.

The US trade deficit ballooned to $37.2 billion in June, up 3% from $36.1 billion in April. The threat of deflation has been raised due to the sluggish economy. Interest rates cannot go below zero and the Fed has already reduced interest rates eleven times to fortyyear lows. For some time we have argued that the Americans have entered a Japanesestyle deflation. Asset bubbles are part of our financial history. From tulips to telcoms, investors have experienced the climate of both fear and greed. We have experienced the greed, now the fear. The Japanese experience suggests that the Fed is fighting yesterday's war. Although, deficit spending has slowed the Japanese economy's slide, it has not reversed it. Bush and Greenspan are repeating the same mistake. Between 1995 and its peak less than six years later, the capitalization of the US stock market rose by $12 trillion. Now with a deflated stock market bubble, almost $4 trillion has disappeared. While the numbers are large, it should be remembered that the overall US economy is only about $10 trillion, so a $4 trillion loss has a dramatic deflationary effect. In Japan, the Japanese appetite for gold increased 500% from a year ago as investors worried about the nation's economy and the safety of their banks. Following the hangover, Americans too might find gold's role as a hedge is a good thing.

The War On Wall Street

Two years ago, investors were willing to believe anything, today there are prepared to trust nothing. Now that the swamp has drained, investors are looking for scapegoats. They are blaming everybody but themselves. While the analysts and investors were calling for more growth, few investigated at what expense that growth would come. Greed made investors gullible. No one can protect people from themselves; no regulator, no central banker, no analysts, and no policemen. Investors bought into the "new economy" ignoring basic tenets, such as price earnings multiples and valuations. While there is no denying that there were abuses to the system and these should be punished, we should not assume that the system itself is broken. We are not here to defend capitalism or the wrong doer, but to point out that every bubble has a downside. It's the same old story, whether it was Bre-X, tulips, or the South Sea bubble. Bubbles are a fact of life; it's the remedies that keep changing. We cannot protect every investor from themselves. To be sure, it will be repeated again and again.

Witchhunt On Wall Street

" In the very midst of the collapse, five of the country's most influential bankers hurried to the offices of J.P. Morgan & Co. and, after a brief conference, gave out word that they believed that the foundations of the market to be sound, and the market smash was caused by technical rather than fundamental considerations and that many sound stocks are selling too low." The New York Times, October 24, 1929.

There has been little commentary against the witchhunt on Wall Street. While we applaud the indictments and the effort to penalize the crooks, the constant attacks on Wall Street to root out the evildoers will do little to instill investor confidence and thus provide the needed base for higher markets. To rid the house of termites, one does not demolish the building, when you can bring in an exterminator. Demolishing the building also leaves you homeless. Indeed, regulators should study new rules, close loopholes, and eliminate conflicts. But, this War on Wall Street does little to eliminate the current abuses or crimes. Karl Marx must be rolling over in his grave... what he could not accomplish with a revolution; Enron, WorldCom, and Martha Stewart have with simple greed... thrown a shadow of doubt over capitalism.

Congressional investigators are scrutinizing the central role that Wall Street played in the bubble. Regulators are looking at analysts' behavior, the various "structured" products and the multitude of roles that the banks played by giving large amounts of credit to the select few. We believe that much of the problems can be linked to the repeal of the 1933 Glass-Steagall Act by the Clinton administration that allowed commercial banks to merge with investment banks. While regulators are erecting new barriers, the market itself should be educated in the "tied business" practices of the Street and the wisdom of seeking more independent advice. Investors should not blindly accept advice particularly from an investment bank that may have multiple roles. The question should be asked, what is the independence of that advice? It's not all about the analyst; it's about the system. In such an environment, the Street should support and allow the reemergence of the old-fashioned independent broker. But alas, the Street seems to prefer simplicity and one-stop shopping, ignoring recent lessons, and the lessons of the thirties. Caveat emptor.

Recommendations

Gold stocks significantly outperformed bullion in the first leg to $330 per ounce. Typically, the shares led bullion on the pullback. We believe that the second leg will see bullion outperforming the shares until gold moves above $330 per ounce. Investors are expected to be cautious until there are clear signs of a breakout. We continue to advise an over-weighted position in gold stocks.

Over the past year, the mostly unhedged mid-cap gold companies outpaced the senior producers who are mostly hedged. The unhedged mid-cap producers provide 100% of the upside but coincidently provide superior growth in production, reserves and potential. The challenge for the big cap producers is to replace more than two million to five million ounces that are produced annually - it's easier for the smaller mid-cap producers to replace depleting reserves. For that reason we continue to like Agnico-Eagle, Goldcorp and Meridian Gold. Among the big caps, we like Newmont and Barrick but note that the new Kinross will be a strong performer in the future. Given the recent pull back, the gold producers are better buys compared to the exploration juniors. We would be more buyers of the producers than the exploration vehicles here. However, we continue to recommend our portfolio of Top Ten Juniors, which includes Crystallex, Eldorado Gold, Claude Resources, High River Gold, Iamgold, Miramar, Repadre Capital, Northgate Exploration, Philex Gold and St. Andrews Goldfield.

Given the problems in South Africa, we believe North American producers will command an even bigger premium. And, as investors become more concerned about the downside risk of the Dow, gold stocks will continue to outperform. Finally, much has been made about the declining supply of mined gold and the lack of major discoveries. While mine supply of gold is likely to decline, we do not subscribe to the 30% forecasted drop due to the mining industry's propensity to keep old mines running. The old Macassa Mine for example has changed hands more times than a Las Vegas blackjack dealer and is still open. Of more significance for investors is the lack of world-class deposits such as Goldstrike or Eskay Creek since much of the near surface deposits have been depleted.

In the latest quarter, gold producers are aggressively unwinding their hedges, through deliveries into contracts, closeouts or actual buybacks. The Australian producers have reduced their hedge books by 8 percent or 1.75 million ounces to 22.6 million ounces in the quarter while gold output fell 8 percent. AngloGold bought back 2.4 million ounces but still has 10.5 million ounces under hedge. Newmont reduced its hedge book by 734,000 ounces in the quarter to under 9 million ounces. Placer Dome will cut its hedging program by 20 percent to 6.8 million ounces but still have 2.8 years of hedged production. Barrick too has also pledged to hedge less in the market, selling half of this year's output at spot market prices. Unwinding the hedges acts as a powerful buying force on the markets in contrast to the sales, which act to depress the price of gold. We continue to believe that producers will buyback additional hedges since interest rates remain low, narrowing the contango. Hedging has become unpopular as investors are concerned about the lack of transparency, the risk potential and the lack of upside.

In a well-publicized battle, South Africa is introducing the Black Economic Empowerment Charter that will change the mining industry forever. While it took some time, the government is introducing legislation that will give black people a greater share of South Africa's mineral resources. A government trial balloon proposed that 51% of all operations should be in the hands of blacks within 10 years. The threshold is likely to be negotiated down, but the objective remains. The government has also introduced a new Minerals Bill, similar to Canadian mining companies, which will force companies to " use it or lose it". While the industry could live with that, the Money Bill's increased royalties, the proposed transfer of ownership to black empowerment groups and new "social" costs will ensure that South Africa's gold production will remain at 50 year lows. At the very least, until South Africa sorts out the new rules, there will be uncertainty in the capital markets and South African mining valuation multiples will shrink further.

Agnico-Eagle Mines Limited

Agnico's expansion of the LaRonde mill to 7,000 tons a day is on track for completion before year-end. In the second quarter, Agnico made a profit of $3.4 million or $0.05 per share reflecting record gold production. Head grade improved and the facility reached a rate of 5,400 tons per day. Agnico should produce 320,000 ounces of gold this year and raised its estimate for next year to 390,000 ounces compared with 375,000 ounces originally planned. By 2004 Agnico is expected to be producing 400,000 ounces per year due to the completion of the expansion. With six drill rigs turning, Agnico plans 60 percent more drilling than last year and exploration results should be out this fall. Agnico has a dominant land position with over twelve miles on the Cadillac mining belt. At the end of the quarter, Agnico had cash equivalent of $28.3 million, working capital totaling $53.2 million and together with a undrawn credit facility over $123 million of liquidity. Given Agnico's rising production profile, unhedged production and the strong likelihood of additional reserves this fall, we continue to recommend the shares here.

AngloGold Ltd.

AngloGold holds the fourth largest reserves in the world at 60 million ounces, producing about 5.7 million ounces of gold annually. AngloGold has over 22 operations around the world, but almost 60% of its production comes from South Africa. Noteworthy, is that AngloGold has aggressively reduced its hedge book by 2.4 million ounces in the latest quarter, bringing its hedge book to 10.5 million ounces or 17% of reserves. Even with this reduction, AngloGold has over 1.8 years of production sold forward, and a negative mark-to-market position of $295 million. In the latest quarter, AngloGold's average realized price was $7 per ounce lower than the spot price. AngloAmerican owns 53% of AngloGold. While AngloGold has often been touted as an acquisition or merger candidate, the assets are cheap but its hedge book and heavy South African exposure limits its appeal.

Barrick Gold Corporation

Barrick reported earnings of $59 million or $0.11 per share price in line with estimates. The Company has a solid balance sheet with cash and short-term investments of almost $1 billion and an undrawn $1 billion credit facility. Gold production in the quarter was 1.35 million ounces at a cash cost of $178 per ounce, reflecting lower grades at the Meikle Mine. Gold production in the year is estimated at 5.7 million ounces at a cash cost of $172 per ounce. Barrick doubled its resources and exploration program at Alto Chicama in Peru to 7.3 million ounces and continues to aggressively expand that resource. Noteworthy was the strong performance by Eskay Creek in British Columbia, which came from Homestake. The Eskay Creek Mine produced 91,614 ounces at $32 per ounce, reflecting the rich ore grade and should produce a solid 378,000 ounces this year. As mentioned earlier, Barrick has reshuffled its hedge book but remains adamant about sticking to its hedging policy. Barrick's spot deferred position was 17.9 million ounces and holds3.1 million ounces of variable price sales contracts and call options, which is too high at 22 percent of proven and probable reserves. Nonetheless, Barrick's balance sheet, array of quality assets and broad market following, in part, offsets the company's contentious hedging policy.

Glamis Gold Ltd.

Glamis reported earnings of $0.04 a share based on production of almost 64,000 ounces of gold in the second quarter. Gold production increased from San Martin, however production fell at Marigold. The San Martin mine continues to be the major producer with 33,772 ounces produced in the quarter. Glamis completed the acquisition of the El Sauzal mine in Mexico and the company is working to complete the final design and permitting. El Sauzal is expected to be in production by 2005, at an annual rate of 170,000 ounces. However, we believe that the estimates are ambitious and feel that Glamis shares are fully priced at current levels.

Goldcorp Inc.

Goldcorp reported a strong quarter with gold production at 149,000 ounces due in part to a solid contribution from the Red Lake Mine, which produced 130,000 ounces at a cash cost of $60 per ounce. The average mill head grade at Red Lake was 2.45 ounces per tonne, an increase from 2.06 per tonne in the previous quarter, and well above the average reserve grade. Goldcorp should produce 585,000 ounces this year. The Wharf Mine should produce 90,000 ounces at a cash cost of $250 per ounce. The company has $218 million in cash and short-term investments and remains debt free. Moreover, Goldcorp purchased 80,170 ounces of gold at an average price at $323, reflecting its belief that gold is money. Interestingly, Goldcorp has almost 144,000 ounces of gold bullion, exceeding the total gold reserves of thirty sovereign nations. We continue to recommend the shares because of the Red Lake asset, strong balance sheet, unhedged production and the aggressive exploration program in the Red Lake area, which is beginning to bear fruit.

Kinross Gold Corporation

Kinross reported a slight loss in the second quarter despite an improvement at Fort Knox in Alaska and the Kubaka mine in Russia. Kinross has almost $100 million in cash and further reduced its debt. The company is in the midst of a three-way merger agreement with TVX Gold and Echo Bay and a shareholder vote is expected in October. We continue to recommend the shares of Kinross for the benefits of the merger, the array of assets and importantly, the strategic plan to be a consolidator in the gold mining business. We expect that the 2 million ounces of pro-forma production will receive an upward two thirds revaluation more inline with the majors, and we strongly recommend the shares here.

Meridian Gold Inc.

Meridian reported excellent results in the second quarter of $0.15 per share, reflecting production of 114,427 ounces. The balance sheet is strong with over $125 million of cash on hand. At El Penon, the company announced an extension of the Vista Norte zone by 200 metres and the deposit remains open to the south and at depth. Importantly, the company was successful in acquiring Brancote Holdings, which is expected to be in production next year. The acquisition of Brancote's Argentine Esquel property brings a second major asset to Meridian, ensuring a rising production profile. We expect Meridian to be on the prowl again utilizing its generously valued paper. We continue to recommend the shares, for its production profile, balance sheet and exploration prospects.

Placer Dome Inc.

Placer reported an excellent second quarter, producing almost 670,000 ounces of gold with cash costs at $181 per ounce. At the company's 50% owned South Deep production costs increased from $159 to $191 per ounce. The Company also completed the Porcupine Timmin's Joint Venture with Kinross, which is an efficient use of both companies' facilities. Significantly, Placer has little in its pipeline to reverse a declining production profile. Placer unveiled its deal at Pueblo Viejo in the Dominican Republic, which is a gold/zinc deposit with ongoing environmental concerns. Placer must develop a plan for this 400,000 ounce producer within four years. Recoveries and metallurgy are the other big uncertainties.

Placer has again extended its bid for AurionGold of Australia. Placer has only accumulated 37 percent due to the resistance by management and major Australian shareholders. Placer has little choice but to extend its bid, because under Australia's takeover rules it would be limited to an incremental and lengthy takeover strategy. Moreover, Placer will not have board representation, which further complicates the takeover. Placer must feel like the proverbial bride's maid and the sorry acquisition record continues.

There are repeated takeover rumours about Placer, because the shares have been a laggard performer. Placer Dome shares have been heavily traded. The latest involves a joint bid by Barrick and Newmont. This rumour follows another of two months ago that was floated with Gold Fields and Goldcorp making a joint bid. Joint bids are always difficult and cumbersome. The obvious negatives are Placer's overly large South African exposure, hedge book, declining production and reserve profile. The positives are two million ounces of steady production and a strong balance sheet. We do not put much weight into these takeover rumours and believe that the volume is attributable more to the liquidation of the approximately 25 million shares of Placer Dome received by AurionGold shareholders. There is no question however that Placer's twelve mines would be attractive to different players but tax issues, valuations and rights of first refusal make a piecemeal deal difficult. Nonetheless, any takeover for part or all of Placer is difficult and thus unlikely. What of a friendly merger? We think not, Placer Dome's management makes that unlikely. We thus continue to recommend avoiding Placer due to the declining production profile, maturing mines, accident-prone management and overly large exposure to South Africa.

TVX Gold Inc.

TVX announced second quarter production of 115,000 ounces and earnings of $0.02 per share. Increased production at Brazilia in Brazil offset lower production at Musselwhite. Cash increased to $117 million reflecting a recent equity issue. TVX shareholders will receive 6.5 shares Kinross for every common share of TVX and final approval is expected this fall. The new Kinross will be the seventh largest gold producer in the world with pro-forma production of 2 million ounces per year and we recommend the shares be held for the Kinross deal.