The Pittsburgh Post Gazette has the sad story of a man whose lifetime of saving evaporated with the collapse of Metropolitan Savings Bank.

Raymond Przybilinski socked away $521,000 from a lifetime of driving trucks, working overtime when he could and playing the piano or accordion late into the evenings at weddings, hotel bars and social clubs.

The money was destined for his five children. But that was before more than half of the family nest egg disappeared on Feb. 2 as state banking regulators seized Metropolitan Savings Bank in Lawrenceville, citing "unsafe and unsound" operations. When Mr. Przybilinski tried to take his money out, the man in charge of Metropolitan Savings' assets informed him that there was only $200,000 left to withdraw -- the amount protected by the federal government.

School of Hard Knock Lessons

- If a bank is offering above market rate interest on CDs and deposits there is a reason behind it. That reason is risk. And with excessive risk comes eventual disaster.

- With credit spreads widening, margin calls being issued, and absurd lending to build condos in Florida and other places smack in the face of record inventories, there are going to be more bank failures like this.

- Know and understand the FDIC limits or your life savings can be wiped out.

- If you have money at a bank in excess of the FDIC limits, do something about it now, while you can.

Moral Hazard

The moral Hazard in this is called risk. Banks are willing to take risk with customers money far beyond what is prudent. And the smaller the bank the less risk banks should take. But because of FDIC insurance both banks and depositors do risky things because of those government guarantees. But as we have seen above, guarantees are available only up to certain limits.

But should there be guarantees at all? Probably not, except on checking accounts and other demand deposits. Why checking accounts? Because logic dictates checking account deposits are supposed to be available immediately on demand and should not be lent out.

Logic? Who cares about logic? Banks are allowed to lend out checking account deposits even though they pay no interest on those accounts. Customers assume the risk and banks literally sweep up the profit. This is a sweet deal for the banks and is accomplished ironically enough via sweeps.

Sweeps are a mechanism by which "excess capital" is swept from some accounts into other buckets based on patterns of expected behavior (not all customers are going to demand all of their money all at once). Money in the accounts where the money was swept is allowed to be lent out. In essence, the money sitting in your checking account right now is not really sitting there at all. It's lent out all over the place (in theory overnight but in practice for god knows how long or for what).

Massive Surge in Sweeps

The above chart came from a study about bank reserve requirements by the Federal Reserve Bank of New York in May 2002.

The complete research paper is a 16 page PDF called Are Reserve Requirements Still Binding?

... retail sweep programs are an inefficient and costly way to avoid reserve regulations. The proliferation of these programs therefore underscores the need for reform.

Conclusion

In this paper, we have presented evidence that reserve requirements are rapidly losing relevance. Although a sizable minority of banks are still bound by reserve requirements in an accounting sense, in an economic sense our evidence suggests that such requirements have had a lessening effect on banks for at least several years. ....

The study does not say it explicitly but I will. There are essentially no bank reserves. Wait a second, I take that back. The combination of fractional reserve lending and sweeps really means there are negative reserves. Far more money has been lent out than really exists. For more on this idea please see the sections "The Fed is Keeping the Top Spinning" and "Money vs. Debt" in Fleckstein (and others) State the Deflation Case with a tip of the hat to Minyanville professor John Succo for both sections.

Inquiring minds might now be asking "Exactly how are M1 and M2 affected by sweeps?" It's a very good question. The answer can be found in Money Supply and Recessions.

For now let's return to the moral hazard. When banks offer above market rate interest rates on CDs the money pours in. It goes pouring in explicitly because of government guarantees. Banks in turn take high risks with that money to be able to afford the high rates. All kinds of projects are thus funded that have no business being funded, like Florida condos for example.

Consider the Business Summary of Corus Bank.

Corus Bankshares, Inc. operates as the holding company for Corus Bank, N.A. that offers consumer and corporate banking products and services. The bank's deposit products include checking, savings, money market, and time deposit accounts. Its loan portfolio primarily comprises commercial real estate loans, including condominium construction and condominium conversion loans; commercial loans; and residential real estate loans. The bank focuses its lending activities in various metropolitan areas in Florida and California, as well as in Las Vegas, New York City, and the Washington, D.C.

Corus bank is operating in nearly every major housing bubble area.

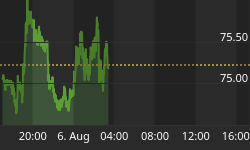

Consider the chart of Corus Bank.

Corus Bank - Cors

High Yield Rates for 1 yr CDs

One can find high rate CDs on Bankrate.com.

The following table is as of August 2007.

By guaranteeing those CDs, money flows to the highest yields simply because of those government guarantees. Who in their right mind would be lending Corus Bank money at such minuscule returns over treasury rates were it not for those guarantees?

Depositors can't really be blamed for this. It's only logical to seek out the highest rates. But one misstep as Raymond Przybilinski found out, can cost a person his life savings. And all sorts of absurd condo projects are getting funded because depositors plowed money into guaranteed CDs and savings accounts.

All things considered, FDIC insurance is a moral hazard except for non-interest bearing checking deposits that banks should not be permitted to be lend out. And anyone wanting risk free returns should buy US treasuries.

I have no problem with banks offering above market rates on CDs provided they and the depositors assume full risk. Taking risk and accepting responsibility for that risk is what the free market is all about. That means no FDIC insurance on those rates and no taxpayer bailouts if and when things blow up.

One point I forgot to emphasize in Will Rate Cuts Save The Economy? is the actions requested by Jim Cramer represent a huge moral hazard as well. When there is an implicit guarantee (sometimes known as the Greenspan Put), people and businesses do all sorts of irresponsible things. Proof is easy to find these days. And although Cramer should know better, he went far beyond asking for rate cuts, he went so far as to ask the Fed to buy massive numbers of futures to blow out the shorts. In other words Cramer was begging for PPT intervention and rate cuts by the Fed without once considering the moral implication of what he was asking.

Congress Never Learns Either

In point number 4 of Tuesday's Five Things, Kevin Depew was asking Who's Afraid of Fannie Mae? Let's take a look.

Yesterday afternoon there was talk the Office of Federal Housing Enterprise Oversight, the GSE regulator, was actively working on ways to expand the portfolio caps that legislation this past spring reduced. Why? Because, as FNM interim chief executive Daniel Mudd and FRE Chief Executive Richard Syron explained to the Senate Banking Committee this past spring, the ability to hold onto some of those loans, and to expand them, can keep funding available in a crisis.

Sure enough, a piece on Bloomberg yesterday afternoon reported, "Fannie Mae, the largest source of money for U.S. home loans, asked its regulator for permission to take on more mortgage assets and help ease a crunch in the credit markets, a person with knowledge of the request said." Well, considering that's the same thing Fannie Mae has been saying for the past two years as legislators sought to cap their portfolios it's hardly news. Unless... unless it's not Fannie Mae doing the asking.

Who else might be asking? Politicians being pressured by banking executives who are worried about how serious the situation in credit markets has become. That would mean that in less than three months we've gone from political pressure to limit the portfolios of GSEs, to political pressure to expand the portfolio limits of the GSEs.

So, who's afraid of Fannie Mae? Us. If these portfolio caps are raised, it would suggest credit market problems are far more serious than thought.

Kevin did not explicitly say it, but once again the moral hazard should be obvious. It was irresponsible lending and borrowing that created this mess. Now, to alleviate the problems caused by irresponsible lending and borrowing, Congress does a complete flip flop demands more of the same.

Instead, I suggest it's time for both people and businesses to consider the consequences of their actions and to be held accountable for them. That is the only way to end these moral hazards.

Monetary Statistics Review

By the way I want to personally thank Gary North for reviewing the money supply aggregate I call M Prime (M') in his recent post Monetary Statistics on LewRockwell.com. He posted that article in response to one of his reader's questions. M' just happens to tie in very nicely with this post. Here are a few snips:

Recently, I was asked a question about money statistics. The person asked if I thought a particular unofficial index is better than the official indexes: M1, M2, M3, MZM.

The article by "Mish" discusses a recent article by Frank Shostak. I am familiar with the work of both men. They are thoughtful, well-informed analysts of economic trends. Shostak does this for a living. He actually invests money for clients. Mish is an advocate of Elliott wave theory forecasting. I am not. Shostak is an Austrian School economist, a view I share. But I don't always follow his logic. This may be my fault.

Mish's article makes several important observations about the relationship between the most prominent monetary aggregates and the economy. He finds that M1 is far better than the other three in forecasting recessions.

Mish has come up with a new aggregate, which he calls M-prime. He symbolizes it as M'. Using Shostak's article as a guide, he argues that M' is superior theoretically because it does not include any credit transactions, i.e., "sell this asset and get money." I agree with his assessment. ....

Mish says that we should focus on the rate of change. This is provided by the yellow line. This does seem to be an accurate forecasting tool. ....

Mish did a follow-up on May 9: "Money Supply is Soaring ... Right?"

It takes to task the use of M-3. I agree wholeheartedly.

...

CONCLUSION

I think M-prime is a better measure than the other M's. If I could get access to it every month on Mish's site, I would consult it.

Note to Gary North and other inquiring minds: The biggest difference between M' and M1 is sweeps. And as shown above, sweeps have exploded.

In a previous phone conversation I had with economist Paul Kasriel, Paul stated an opinion that the Fed keeps tracks of sweeps in their review of M1. Of course that is a theory that cannot be proven, which is exactly what Kasriel said to me.

I would like to correct a couple of small things Gary North said. Ewave it is just one of the tools we use. We use many other tools as well such as advance decline, support resistance, and many other technical analysis tools. I would never recommend using E-wave alone. The "we" in this paragraph refers to Sitka Pacific Capital Management. I am a licensed investment manager representative for Sitka Pacific. Sitka Pacific publishes monthly commentary about the markets and one can sign up for free, or view it online at by clicking that last link.

I will see what I can do about more timely updates of M' especially if people are interested in tracking it. By the way, the charts are actually produced by "Bart" at NowAndFutures using specifications from me based on a formula from prior articles written by Frank Shostak. Without help from NowAndFutures, those charts would not be published. So thanks to both "Bart" and Frank Shostak as well. But don't look for fireworks. It moves pretty slowly especially to someone used to watching M3. Also note that our sweeps data is about one month delayed. Thank the Fed for that. But all things considered we are probably lucky the Fed posts sweeps data at all.