Having been born in the early 1970s, I remember coming of age politically to two important lessons. We will never forget, I heard pundits, politicians, and academics sayings, that:

- The U.S. should not engage in any military action that is not definable and achievable;

- Inflation should be contained at an early stage, no matter what the cost.

As such, it is with great disappointment that the two unforgettable lessons of my early childhood have seemingly been forgotten, and I haven't even turned 35. Sidestepping the politics of the war, I'd like to focus on inflation. I'd like to explore why we have abandoned our previous caution and why the later part of this decade threatens to look a lot like the late 1970s.

As my good friend, Michael Nystrom, and I were discussing today, one of the biggest problems - and most frustrating problems - that America faces is that so few people see or care about how credit & money supply growth are creating imbalances in our economy. Because so few people care about monetary policy and economics, pundits, politicians, and academics take advantage of peoples' ignorance to point them at the wrong causes of the problem (except, of course, Ron Paul, who's a brave politician who points out the importance of strong money). Backing up and taking a more generalized view, we can see the cycle of money supply growth and inflation in action. The model I have developed for this purpose is the Zentay Cycle (a very modest name indeed). As many readers may recognize, this cycle owns a great debt to the Kondratieff Cycle, after which it is modeled. The difference, or rather extension of the Kondratieff Cycle, is that the Zentay Cycle seeks to bring in politicians and bankers and explain their participation and reactions within the various seasons of the cycle.

Spring of the Cycle - This is the season in which I came of age, from around 1984 to 1992. The Spring is the most intellectually pure stage of the cycle. The harsh Winter of higher interest rates and economic recession has passed (Volcker raising interest rates and forcing the 1980-81 recession), but society remembers the lessons from persistently high inflation. Central bankers are conservative and are supported in their calls for interest rates high enough to fight off inflation. Bankers and investors agree with central bankers. Bond vigilantes sell long-term bonds at any hint of inflation or whenever central bankers appear to be less conservative than is necessary. High interest rates from the Winter have left the consumer landscape with low levels of debt. Politicians may try to raise taxes or increase spending, but they only have limited success, as central bankers and pundits claim that higher taxes will slow economic growth and increased spending will cause inflationary deficits. Gradually, the high government debt levels from the Winter come down somewhat. At the start of the Spring, businesses have high debt levels and low price-earnings ratios. They begin to reduce their debt levels over time. Average interest rates begin to move lower, as the fear of hyperinflation recedes. Shockwaves of fear appear from time to time (such as 1987 and 1991), but in general the Spring is an improvement from the Winter. Central bankers are respected and increasingly well regarded. Politicians are neither popular nor unpopular. Bankers are moderately successful. Average citizens do okay, not great.

Summer of the Cycle - This is the happiest time of the cycle, from around 1993 to early 2000. The shockwaves of fear dissipate. Average interest rates come down more, government debt levels are contained, and economic growth accelerates, creating a wealth effect throughout many levels of society. The more wealth is created, the less conservative participants become. With economic growth, consumer and businesses are more willing to add debt. The debt and credit creation adds more growth and the perception of productivity gains. These productivity gains allow central bankers to relax their conservative stance towards interest rates. Lower interest rates lead to lower costs of capital, the perception of even more productivity gains, and more debt and credit creation, with all the ensuing short-term benefits. Faster economic growth leads to government surpluses. Businesses do very well, keep debt levels reduced, and see their price-earnings ratios expand. Central bankers and politicians are wildly popular. Bankers are successful. Average citizens do well. Class tensions ease. Everyone is generally happy.

Fall of the Cycle - This is the time when problems in the cycle begin to emerge, from around mid-2000 until 2007. A recession or market crash creates a slowdown in economic growth and aggregate demand. Central bankers, less conservative because of their success and popularity in the Summer, lower interest rates to "save" the economy. Debt, credit, and money supply increase even more dramatically, which temporarily leads to a mini-summer and the perception that nothing is wrong. However, productivity levels begin to decline as the burden of debt leads to systemic imbalances. Mild hints of capacity constraints and inflation appear from time to time. As the mini-summer begins to fade, more serious problems emerge. Politicians are increasingly unpopular. Businesses add more leverage, oftentimes through innovative and off-balance-sheet mechanisms. Bankers continue to be successful through increased leverage, but average citizens struggle. Class tensions begin to escalate towards the end of the cycle. Skepticism towards leaders and centralized institutions is rampant.

Winter of the Cycle - In an effort to prevent the onset of Winter, central bankers try to lower rates dramatically, and begin to do whatever they can to create more credit and money supply, but economic problems remain. Politicians, unsatisfied with the results from the central bankers' actions, call for more government spending and government-induced demand-side solutions. Central bankers continue to call for restrained spending by politicians, but central bankers are less and less popular and lose credibility. Taxes are increased to cover the expenses of government programs. Productivity falls. Inflation begins to increase persistently as capacity constraints spread and demand-side solutions exacerbate these constraints. Pundits wonder at the cause of inflation and many short-term solutions are proposed with little success. Economic growth flounders and unemployment increases. Bankers lose money as confidence in the financial sector falls and long-term interest rates rise. Businesses and banks suffer from lower economic growth and the higher leverage incurred during the Fall. Bankers, too, turn on central bankers. Class tensions are high as different parts of society fight over the validity of different government-sponsored solutions. The Winter is long and hard. Exhausted by the duration of the Winter and already wildly unpopular, central bankers come to the realization that the only way to end the Winter is the opposite of their past solutions. Rather than creating more credit and money supply, they seek to dramatically reduce credit and money supply. Interest rates go up significantly, economic recession is harsh, citizens suffer, businesses and banks are hurt, but the end of inflation and Winter is achieved.

If the Zentay Cycle is in fact correct, I believe we are at the cusp of generating higher inflation. Productivity gains from the Summer are fading, credit and debt levels are too high, central bankers are beginning to try very hard to increase liquidity, and politicians are starting to talk about demand-side solutions. However, employment levels are already high, capacity utilization is high, and other parts of the economy show little excess capacity. Certainly housing is in decline and has excess capacity, but housing seems to be the exception rather than the rule. For example, more oil is being consumed worldwide than produced. Fertilizer companies are reporting significant demand and an inability to meet some customers' orders. Hotels are often full and prices are going up. Airlines are operating near full capacity and starting to raise rates for the first time in many, many years. The important core-driver of unit labor costs is now increasing 5% a year. In other words, economic volatility is NOT reducing costs.

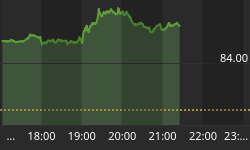

Just look at the daily price of dry-bulk shipping for an idea of what is happening to global prices:

Unfortunately, those in power have not seemed to have learned the lessons of the past. The late 2000s is unlikely to be identical to the late 1970s. "History," Mark Twain said, "doesn't repeat itself, but it does rhyme."