What does the negative silver lease rate really mean?

Antal E. Fekete

Gold Standard University

aefekete@hotmail.com

On Thursday, September 20, 2007, the lease rate of silver suddenly dipped into negative territory. It fell to minus 0.1 percent per annum. I wish Ted Butler stopped bitching about silver manipulation, and instead explained the behavior of silver lease rates and the silver basis to his readers. In particular, he should explain negative lease rates, and negative basis or backwardation. It may be more helpful in promoting an understanding of the silver market than telling fairy tales about raptors and dinosaurs.

I have a long-standing disagreement with this silver analyst. I hold the view, in opposition to Butler's, that silver is a monetary metal second only to gold in importance. Supply-demand analysis of price is not applicable to silver, still less to gold. The reason is that both supply and demand are undefinable in case of a monetary metal. There is no way to quantify speculative supply and demand. Speculators make split-second decisions and from sellers may become buyers, or the other way round.

Making predictions for the silver price on the assumption that it is allegedly scarcer than gold does not make sense. Silver has been, is, and will continue to be cheaper than gold for a monetary reason that is the very opposite of the scarcity argument. The monetary stockpiles of gold are much larger than that of silver. Therefore there is less of a threat for the value to drop on account of new additions to the stockpile in the case of gold than in the case of silver. It is not the absolute change in mine output that has an impact on the value of a monetary metal, but the relative change as a percentage of existing stockpiles. For this reason gold is more valuable than silver: the huge stockpiles of gold make the impact of a change negligible. Ergo the value of gold is more stable. In technical language, the marginal utility of gold declines more slowly than that of silver.

As a consequence, the specific value of gold is higher. This means that the value of the unit weight of gold is higher than that of the same weight of silver. Once this fact has been firmly established by the markets, it is not likely to change. The monetary metal with the higher specific value is more portable both in space and time. In more details, the cost of transporting the unit of value as represented by gold is lower. For example, if the bimetallic ratio is 15, then the cost of transporting the unit of value as represented by silver is about 15 times higher. Roughly the same rule applies to the cost of storage as well. This makes gold superior to silver as a monetary metal. It is more suitable as a vehicle to transfer value over space as well as over time.

But silver is still a monetary metal, and for certain application such as parcelling out value in ever smaller bits, for example, silver could be superior to gold. And, of course, when it comes to enumerating industrial applications, silver has a very impressive list. In many cases there is no substitution for silver. However, do not make the mistake to think that gold has no industrial applications. It does but, because of its high specific value, these applications are mostly submarginal and as such they are ignored.

In 1922 Lenin gave a textbook example of such a submarginal application of gold. At a meeting of Communist party activists he famously said that, after the final victory of Communism world-wide, gold will be used for the purpose for which it is so superbly fitted, namely, to plate the walls of public urinals. He did not say that his plan could not be realized in the workers' paradise because workers would pick the gold plate of urinals just as fast as the government was installing them.

Another common mistake people make when comparing gold and silver is to say that gold is "not consumed" and therefore practically all the gold ever produced is still available while silver is "consumed" and, hence, is getting scarcer relative to gold all the time. The truth is that both gold and silver are consumed, for example, in the arts (including jewelry). The difference is in the cost of recovery, recycling, and refining relative to the underlying value. Precisely because the specific value of gold is higher, the cost of recovery for gold is lower, so much so that gold in the form of jewelry is often lumped together with monetary gold for statistical purposes. By contrast, silver plate could not be lumped together with monetary silver because of the substantial cost of recycling expressed as a percentage of the underlying value.

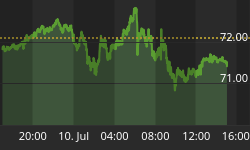

Returning to the silver lease rate, this was not the first time it dipped into negative territory. The 30-day lease rate was pretty consistently negative between May 25 and August 4, when it shot up and reached a high of plus 0.4 percent on August 31. The fact that negative silver lease rates are not impossible but a well-observed fact of the silver market has exploded the myth of a world-wide shortage of silver. Come to think of it: lessors of silver are willing to pay lessees a premium for borrowing the metal. But before you rush over to ask lessors for free silver, you had better come to a correct understanding what negative lease rate means. The collapse of the silver lease rate on September 20 to negative territory meant panic short covering in silver. The shorts anticipated an imminent and substantial rise in the price of silver and were running for cover.

How did they know that the silver price was poised to rise? They were not led by crystal balls. They acted on the historic correlation between gold and silver prices which customarily move "in sympathy" with one another. On September 10 the gold price was getting ready to break the resistance level at $700, while the silver price lagged far behind in relative terms. The peak price of gold for the past 27 years, $730 an ounce, established in July, 2006, was well within earshot. The corresponding peak price for silver, $15, established at the same time, was not. Thus gold was well-placed to make a new high soon, silver selling at $12.75 was not. Nevertheless, if gold moved, it was reasonable to assume that silver would play catch-up. In the event the price of silver moved some (on Friday, September 21, it closed at $13.50) and, according to analyst Clive Maund, "was set to go through the roof" (www.safehaven.com, September 19, 2007).

The point is that if this happens, as it very well might, the price move will not have been caused by any kind of shortage. The notion that we have a silver shortage is preposterous. Most of the silver produced by the mines and sold by the U.S. Treasury during the past 60 or so years still exists in monetary form. Monetary silver is owned by private individuals who entrust it to commercials skilled in making monetary silver yield a return. This is the reason why silver and gold are monetary metals: they can yield a (more or less consistent) return to their holder if traded adroitly and professionally. This fact may not be too well known, but it is true nevertheless. "Demonetization" has done nothing to destroy the unique ability of monetary metals to earn a return. Without a doubt, the best way of making this happen is through playing the short side of the market. Sitting on a long position of silver will not hatch the silver egg, nor is it a very intelligent way to make silver yield a profit. A better way is covered short selling which to the uninitiated appears to be naked short selling. It is not.

The commercials are neither stupid nor suicidal. They are professionals who make it their business to call the tops and bottoms in the price moves of monetary metals. It is well-known that they have an excellent track record in calling the market. This is not because they are vicious people who manipulate the market to their own advantage enticing the poor bulls to enter the slaughter-house. They use methods that are well-known, pretty standard among professionals, and can be learned from textbooks. Using these methods they can turn the variable silver price to their advantage (or to the advantage of their clients on whose behalf they trade). It is not a cabal. You can join their ranks if you are willing to study those methods and go through the training which may be too rigorous to your taste.

If you are envious, or have moral objections against other people being able to make money consistently by trading the monetary metals, then you should lodge your complaint with the government which is responsible for "demonetizing" first silver (1873) and, a hundred years later, gold (1973). Before "demonetization" there were no commercials, no speculators, and no scalpers who made money by betting on the variation in the price of monetary metals. Those who had tried to make a living that way went hungry. The prices of monetary metals were stable.

Whenever the price of silver significantly lags the rising price of gold, there may be panic short covering and the leased silver will be returned to the lessors in a hurry. If the lessors were not prepared for this avalanche of silver (because they expected that the leases would be rolled over), then they may not be able to absorb the silver flowing back to them. In this case the silver lease rate drops dramatically and may even dip into negative territory.

It is important to be able to interpret this correctly. As I said, silver is delivered faster by the lessees than the lessors are able or willing to absorb it. Admittedly it is a market aberration, but whatever it means, it does not mean a shortage of silver. Far from it. It indicates a relative redundance of silver that momentarily cannot find lessees in view of an impending rise in the silver price.

The verbiage about silver manipulation is just so much tilting against the windmill. In his latest commentary dated September 18 Butler distinguishes between upside price manipulation or cornering the shorts, and downside price manipulation or cornering the longs. He adds that while the former is fairly common, the latter is exceedingly rare. Downside manipulation results in much lower prices than would otherwise prevail and, when it ends, the price explodes upwards. Butler is right on. A corner on the longs is in fact so rare that it does not even exist, except as a figment of the imagination of some analysts. The longs cannot be cornered, especially in a corner lasting for years.

Rumor-mongering about present or future silver shortages do not bring credit to the analyst. He should go back to his textbooks and study the market in greater depth. Above all, he should learn the elementary differences between monetary metals and non-monetary commodities.

We have had a torrent of short covering recently. It should have caused a meteoric rise in the price of silver, as predicted by the analysts. It just did not happen Yet it may still happen. Suppose it does. Will then the case for market manipulation be established? Of course not. What it would show is not that the commercials can and do manipulate the market and control the silver price that way. It would only confirm what we have known all along, that the commercials have a superb understanding of the silver market and can correctly anticipate impending significant price moves.

* * *

At Gold Standard University we use scientific principles to study paraphernalia such as the gold and silver basis, the gold and silver lease rates and their variation. In addition, we look at changes in the NAV (net asset value) of gold and silver ETF's (exchange traded funds).

We think the best way to make a profit consistently on silver and gold holdings in troubled times is bimetallic arbitrage. At its crudest, this means selling silver to buy gold when the bimetallic ratio (gold price divided by silver price) falls, and selling gold to buy silver when it rises. In this was we always buy the monetary metal at a low price, and sell it at a high price.

However, as a consequence of concentrated propaganda-gold-sales by central banks and governments, not only the gold price but also the bimetallic ratio is falsified. Therefore there is need for refinement, and for enlisting other clues, in addition to the bimetallic ratio. We believe that such more refined clues can be derived from the variation in the basis, lease rates, the NAV of ETF'S, and the like, for both gold and silver.

Under bimetallic arbitrage there is no profit taking as exchanging monetary metals for irredeemable currency is considered a retrogressive step, utterly dangerous to boot. A simultaneous fall of the gold and silver price is interpreted not as a fall in value of the monetary metals, but as a temporary bounce in the value of irredeemable currencies. The trouble is that it could be a dead-cat- bounce.

* * *

As a preliminary announcement I mention that Session Three of Gold Standard University Live will take place in Dallas, Texas, from February 11-17, 2008. (Please note the change of place and date.) It will have three parts: (1) a course on Adam Smith's Real Bill Doctrine and its Relevance Today, consisting of 13 lectures, from February 11-14; (2) an open-ended debate on True and Fraudulent Hedging of Gold Mines, with industry participation representing both sides of the issue; (3) a panel discussion entitled Gold Profits in Troubled Times where paraphernalia such as the basis, the gold and silver lease rate, the NAV of gold and silver ETF's and the variation of these will be discussed with invited experts. Program (2) and (3) are scheduled for the week-end February 15-17. The registration fee covers participation in the debates during the week-end, but it is possible to register for the week-end program only. Participation is limited; first come first served. Participants pay their own hotel and meal bills; a closing banquet is included in the registration fee.

For the benefit of European friends of Gold Standard University, Session Three will be repeated in March, 2008, at Martineum Academy in Szombathely, Hungary, where the first two sessions were held, provided that a sufficient number of people register. More details will follow later.

For further information please inquire at GSUL@t-online.hu.