The following article was sent to members on Oct 6th.

What does GOOG have in common with BHP?

During the summer meltdown in stocks and credit we pointed to two sectors, large cap tech and materials, which investors should target for long exposure and monitor for signs the market was stabilizing. The thesis behind large cap tech was that their strong balance sheets and relatively high cash levels would be attractive for investors rotating out of the non-transparent leveraged balance sheets of banks and broker dealers. When liquidity is tight those that possess it stand to benefit. Conversely, the thesis behind materials was that they were at the front line of the global cap-ex and infrastructure story and would be the first to know if central banks were providing sufficient liquidity to unlock investment capital which would show up in the performance of these cyclical companies that also benefit from a weak dollar which raises the value of their underlying commodity assets.

Ironically the rationale was quite different but the sector performance has been quite similar.

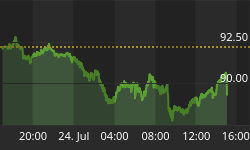

Consider the correlation of the following sector leaders with polar opposite businesses since the 8/17 Fed discount ease low:

The charts speak for themselves and considering the degree of these parabolic moves in sector leaders as the major indices run into resistance at the previous highs we think it's now prudent for investors to be cautious and look for a pullback.

Are these cyclical stocks discounting a rapid pick up in economic growth or are they discounting a rapid pick up in inflation?

We doubt portfolio managers are piling into the likes of BHP and MON because they anticipate another leg higher in the global growth rate, but instead are betting on beta with the wind of the Bernanke put at their backs. We are skeptical Bernanke will continue to provide excessive stimulus with the dollar falling apart and commodities going parabolic thus we are getting defensive on this particular wager. The credit market remains tight per the relatively wide LIBOR T-Bill spread (~125bps) implying banks are still hoarding cash with still a few hundred billion in leveraged loans that need to be retired. Recent collapsed LBOs such as SLM, HAR and ACXM indicate credit is still difficult to obtain at levels sufficient to service by falling cash flow yields. While many deals will get done at a price, bank balance sheets are contacting and last week's write offs by C and UBS demonstrate the destruction in book value as collateral is liquidated at discounts. With so much debt supply hitting the market it is unclear whether the expansion of credit and balance sheets can continue without substantially increasing the money supply. This is the bet these materials stocks reflect but considering we are looking for a major low in the greenback in the coming months we are cautious on materials up here as we do not think they can sustain this rally in these relatively tight monetary conditions.

Technology is also highly cyclical and subject to decelerating earnings growth when the economy slows. Some of the more speculative names such as GOOG AAPL RIMM are essentially options on beta. As performance driven portfolio managers and quant funds need exposure to the market, they trade in and out of these names increasing the momentum feedback dynamic. In fact, last week AAPL traded more dollar volume than the hedge fund's favorite trading instrument, the heavily traded QQQQs. This helps confirm the notion that these tech momo leaders are simply a proxy for high beta market exposure and when these names roll over it could signal risk appetite is waning. Tech held up well during the credit market turmoil but if the credit cycle reversing manifests into an economic slowdown the cyclicals will likely suffer and these high beta tech names could retrace these recent gains just as fast as they made them.

Bottom Line: We wanted exposure to the tech and materials sectors when the market was near its lows in August despite the differing rationale. A barbell strategy with some more defensive sectors, such as health care and consumer staples, yielded a nice risk/reward return over the past 30 days or so. That being said the nature and degree of the rally coming off easier monetary policy and a weaker dollar has us cautious up here and looking for a sharp reversal when momentum shifts which in turn could put the recent gains in the broad indices in jeopardy.