Market Wrap

Week Ending 4/11/08

The Economy

The U.S. Bureau of Economic Analysis reported that the U.S. monthly trade deficit increased from $59.0 billion in January to $62.3 billion in February.

Imports increased more than exports. The January deficit was revised higher than its previously published value of $58.2 billion.

Exports

Exports increased $3.0 billion in February to $151.4 billion, mostly due to an increase in goods exports. Services exports also increased.

-

The increase in goods exports were more that offset by increases in industrial supplies and materials; foods, feeds, and beverages; and other goods. A decrease in capital goods was a partial contributing factor.

-

The increase in services exports was mostly accounted for by increases in travel and royalties and license fees.

Imports

Imports increased $6.3 billion in January to $213.7 billion, reflecting an increase in goods imports. Services imports also increased.

-

The increase in goods imports was due mostly to the increases in consumer goods; automotive vehicles, parts, and engines; and capital goods.

-

The increase in services imports was largely accounted for by increases in other transportation, travel, and other private services.

FOMC

The Federal Open Market Committee (FOMC) issued the minutes from its last meeting. The news was less than inspiring. Some highlights follow:

FOMC MEETING MINUTES

"Payroll employment declined substantially; oil prices surged again, crimping real household incomes; and measures of consumer and business sentiment deteriorated sharply in their discussions of the economic situation and outlook, FOMC participants noted that prospects for both economic activity and near-term inflation had deteriorated in view of increasingly fragile financial markets and tighter credit conditions, rising prices for oil and other commodities, and the deepening contraction in the housing sector.

The outlook for economic activity had weakened considerably since the January meeting, and members viewed the downside risks to economic growth as having increased an escalation of an unhealthy dynamic that was developing in money and credit markets, in which liquidity and collateral concerns were spreading."

ECB

European Central Bank President Jean Claude Trichet said that he's not ready to cut interest any time soon. The ECB kept its key rate at 4 percent.

"We are experiencing a rather protracted period of temporarily high annual rates of inflation."

G-7 Meeting

The G-7 is meeting this weekend. Speculation abounds as to what the central issues will be that are discussed. They have a number of topics to choose from: Israel's massing of troops along the Gaza Strip, the saber rattling over Iran, the price of oil, the downturn in the world economy, rising global food prices, and the spreading credit crisis - to name but a few.

Of interest was President Bush's meeting with the euro zone finance minister Mr. Jean-Claude Juncker. After the meeting Mr. Juncker was reported to have said:

"The American president repeated that the American administration is in favor of a strong dollar, which is in the interest of the U.S. economy."

Stocks

The recent rally in stocks came to an abrupt end today. The Dow closed down just over -2% for the week, and the broader market, as measured by the S&P 500, was down just under -3% on a weekly basis.

There are those who say the bear market (or recent correction) is over and that a new bull leg up has begun. I beg to differ. As the chart of the Dow below shows, the falling upper trend line has so far offered stiff resistance that has not, at least as of yet been bettered. Until resistance becomes support the trend is down. Also, notice that on the recent rally volume declined, and that on today's fall volume increased.

Bonds

Interest rates have been steadily coming down for some time now, in a successful endeavor to reward buyers of U.S. government debt.

This has provided a wind-fall for bond owners, specifically the Japanese and Chinese who hold over 40% of all Treasury debt.

The first chart below shows how steep the yield curve has become, as short term rates have fallen much farther and much faster than long term rates.

The second chart shows the inverse relationship between the stock market and the bond market.

Currency

The euro is presently undergoing a consolidation. As the chart shows, after every recent rise the euro spends a good deal of time consolidating the move up before proceeding on another leg higher.

Notice, however, the negative MACD cross over and the negative histograms, which suggest more downside action is likely; although MACD appears to be rounding off and the histograms are receding.

The U.S. dollar is a poster boy for what you don't want your currency to do - fall precipitously. Since 1913 the dollar has lost 95% of its purchasing power, which the chart below clearly indicates the rest of the world is aware of.

We can only imagine what the chart would look like if the dollar was not the reserve currency of the world. As it is, the chart goes from the upper left hand corner to the lower right hand corner - as bearish of a signature as one can get.

There is some short term hope, however. One, the dollar is oversold, with a plethora of players all on the same side of the trade, which can suddenly capsize the boat and flip it the other way.

ROC is moving up from negative territory into positive territory. Stochastic readings are still headed down. MACD is still under a positive cross over. The signals are mixed.

Commodities

On the daily chart commodities have rallied up into their 50% retracement level, which is providing overhead resistance.

MACD has put in a positive cross over and the histograms have turned positive as well.

The weekly chart of the CCI Index tells a bit of a different story. MACD is under a negative cross over and the histograms have turned negative as well.

This suggests that the short term may be positive, while the intermediate term appears negative. Watch the direction of the euro for a hint as to the direction of commodities.

IMF Gold Sale

The proposed gold sale by the International Monetary Fund has received a lot of press lately. They have reported that they would like to sell about 400 metric tons of gold, presently valued at a just over $13 billion.

The supposed purpose is to raise money to fund operating costs. The IMF reports holdings of just over 3200 hundred metric tons, so the sale would represent about one eighth of its total reserves.

The sale of the gold must be approved by the United States Congress. Taking into consideration that many citizens are opposed to the sale, it is difficult to imagine that during an election year Congress would risk raising the ire of the voting public. But stranger things have happened.

However, the chance of the sale going through before the elections seems to be less than likely, and the question also remains as to whether the market has already factored the sale into the price of gold, as the proposed sale has been in the public domain for months.

The bottom line is that it does not appear to be as big of a deal as some make it out to be. There would probably be the usual short term emotional reaction, however, the long term trend is a law unto itself and would reassert itself accordingly.

Gold

Gold had a pretty good week, closing up just over 1%. The signals are mixed, however, both on the daily chart and on the weekly chart; as well as the comparison between the daily and weekly charts.

The daily & weekly chart show RSI headed lower. The daily chart has the 20 ema being broken below and now acting as resistance. On the weekly chart the 20 ema is still providing support.

Volume has declined on both charts during the recent rally up, while it expanded on the move down.

On the daily chart MACD appears ready to make a positive cross over, while the histograms have receded back towards zero. The weekly chart shows a negative MACD cross still in effect with histograms in negative territory as well.

ROC has been headed down on both charts, with the weekly showing a slight up tick. The accumulation/distribution lines on both charts are positive.

The daily chart has the stochastic indicator headed up strongly, while the weekly shows the opposite - the stochastic indicator is head down.

The signals remain mixed on each chart and from one chart to the other. The weight of the evidence points to a short term rally being possible, with more backing and filling needed of the intermediate term trend.

Silver

Silver did not fare as well as did gold this past week, as it lost about .25%.

The daily chart of silver is pretty much a carbon copy of the daily chart of gold. All indicators point in the same direction from one chart to the other.

The same holds true for the weekly chart of silver and the weekly chart of gold, all indicators point in the same direction.

Gold's weekly chart is a bit more negative than silver's, as MACD & the histograms have turned down much harder and further on the weekly gold chart compared to the weekly silver chart.

Silver's out performance is exemplified in the chart below. The daily & week charts follow.

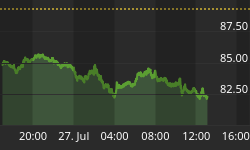

SLV Daily

SLV Weekly

GDX

The precious metal stocks as represented by the GDX were down just under -1.5% for the week. With physical gold up on the week, this constituted a negative divergence in the precious metal sector.

Up next is the daily chart of the GDX, which shows price running into overhead resistance at its 38.2% fib retracement level. The index is also below its 50 day moving average.

MACD & the histograms are turning positive, but ROC is headed down.

The weekly chart of GDX shows that price is still above its 65 ema, but it is getting closer. So far a series of higher lows are in place. As long as higher lows remain intact - higher highs will follow in due time.

Both MACD & the histograms are in negative mode, however, ROC is turning up and about to cross into positive territory. Volume declined on the recent correction down (and on the most recent rally up).

Short term if price can get back over its 50 ma on the daily chart (50.31-presently trading at 48.22) it will have a good shot at filling the gap just above its 50% fib retracement level at 51.50-52.50. Intermediate term more backing and filling appears needed.

Invitation

The latest full-length version of the current week's market wrap is available only at our web site, including this week's stock chart watch list and any buys or sells executed this week that are on the website.

Stop by and check it out. Most major markets are included with the emphasis on the precious metal markets.

There is a lot of information on gold and silver, not only from an investment point of view, but also from its position as being the mandated monetary system of our Constitution - Silver and Gold Coin as in Honest Weights and Measures.

On the main homepage are papers and articles by some of the best out there to be had. There are audio and videos on banking, the Constitution, and cutting edge news. Many articles are archived and others are linked.

Live time quotes on gold and silver and precious metal stocks are available, including charts for most world currencies and futures.

Links to the World Bank, Central Banks, the International Monetary Fund, the United Nations, the Bank for International Settlements, and many other similar and different sources are available.

There is also a live bulletin board where you can discuss the markets with people from around the world and many other resources.

See picture below.

What our money paid for oil and gas is buying.

Hydropolis, the world's first underwater hotel. Entirely built in Germany and then assembled in Dubai. It is scheduled to be completed by 2009.

Good luck. Good trading. Good health, and that's a wrap.

Come visit our new website: Honest Money Gold & Silver Report

New Book Coming in 2008 - Honest Money