When it comes to the savings habits of Americans, you are more likely to hear one side of the story--that they are not doing nearly enough of it.

For instance, this alarming Bankrate report says that wholly 20 percent of Americans are saving nothing at all. Another one by the consumer financial services firm deadpans that nearly a quarter have no emergency fund to speak of yet they are not losing sleep over it.

But the truth of the matter is that while one corner of the savings universe is perpetually cash-strapped, the other has gone for overkill and is drowning in too much cash. And you can’t blame them since it seems desirable to have more than enough cash than what you strictly need for emergencies.

Opportunity Cost of Coash-Hoarding

Holding lots of cash in your bank account might actually seem like an enviable problem to have for many. In the current environment of rising interest rates, commercial banks are slowly but surely increasing interest rates paid out to customer deposits so as to remain competitive. Related: Wells Fargo Rocked By Another Major Scandal

Online banks are currently paying the best rates, going as high as 1.85 percent annual return. Further, you pay zero taxes on interest earned if the savings account is titled in the name of a tax-deferred retirement account such as IRA or Education Plans (the others should submit form 1099-INT if interest earned in one year exceeds $10). And, your bank probably won’t penalize you unless you are talking about really massive cash deposits above $50 million and too many people start parking huge amounts in their accounts).

But there really is such a thing as having too much cash—in fact many Americans could be falling victim to this seemingly innocuous trap.

According to new data from NerdWallet, the average American adult is currently holding $32,286 cash.

Given a median wage $44,564 per year and the fact that a large chunk of the adult population does not save at all, that stash suggests that there’s a sizable portion of the adult population hoarding much more than six months’ worth of expenses. In fact, a good 39 percent of Americans say they aren’t investing at present.

There are various reasons why Americans are clinging tightly to cash. For starters, it lets them sleep better because there’s little to zero risk of losing your cash (FDIC insures cash deposits of up to $250,000). The same can hardly be said of investments like stocks whose short-term returns cannot be guaranteed.

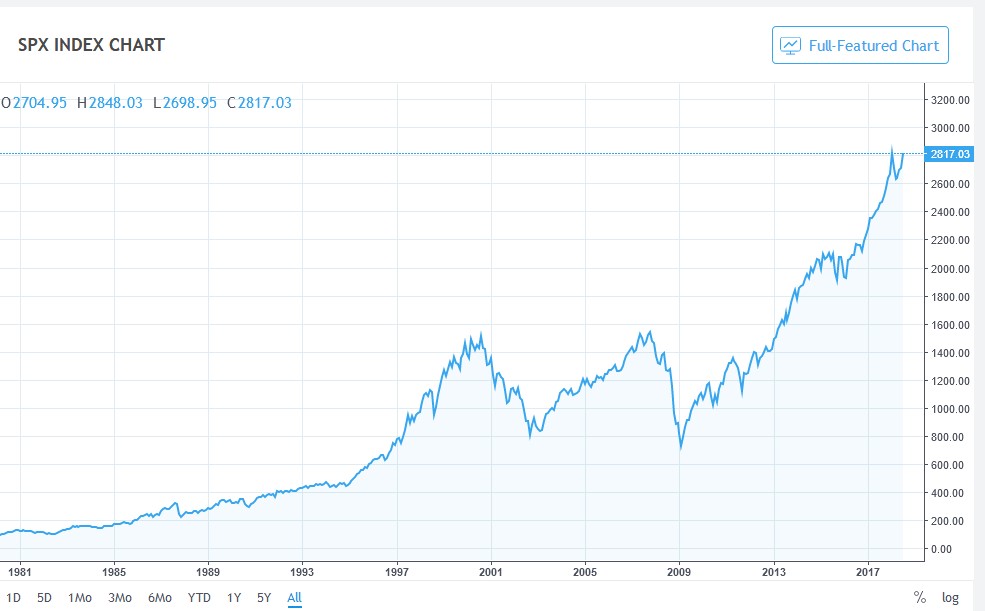

The biggest problem with keeping too much cash in the bank is simply because of the opportunity costs. In other words, you leave too much money on the table and fail to make your money work hard enough for you. Even buying CDs compares poorly with investing in equities over long periods of time. A good certificate of deposit might score up to 3 percent on a five-year term. That’s just a third of the nine-percent average return by the S&P 500 over the past thirty years. Assuming you leave your $32,286 cash lying in a savings account that scores an average annual 2 percent return for 30 years, your money will grow to $58,481.

Related: How Will A Global Economic Crisis Impact Bitcoin?

Now let’s assume that you take the same cash and buy the S&P 500 ETF (SPY). This time let’s say the stock market is not so generous and is only able to generate a seven percent annual return. Your $32,286 investment will still manage to grow to a much bigger $245,769 pile, more than four times bigger the bank investment. If the market continues with its long-term trend, your cash pile will swell to $428,360--more than seven times bigger.

That’s the power of compounding, where a difference of just a few percentage points in yields can boost your returns quite dramatically over periods of time.

(Click to enlarge)

Source: TradingView

Getting Started with Stock Investing

Nearly 30 percent of respondents in the NerdWallet survey admitted that they hang onto cash because they don’t know how to invest.

For a beginner, buying an index fund like the S&P 500 ETF(for large-cap stocks) or the Vanguard S&P 500 ETF(for small-cap stocks) is a good place to start. Index funds track existing indexes and are passively managed meaning low fees for you.

The best part is they save you the trouble of trying to identify individual stocks that are potential winners, though the tradeoff is that some individual stocks can provide much higher returns.

By Alex Kimani for Safehaven.com

More Top Reads From Safehaven.com