Is the Goldilocks economy back in the driving seat? Probably not, though the unfolding market frenzy would have you believe so despite the fact that it’s coming hot in the wake of some of the worst turmoil in recent memory.

After a brief encounter with the big, bad bear, optimism has returned to the markets with a vengeance and greed rules once again. Suddenly, the late-cycle narrative seems so passé and money managers are gobbling up negative-yielding debt and other risk assets like it’s 2017 again—all thanks to a return of dovish monetary policies.

Buckle up for the ride; risk-on markets are here again.

(Click to enlarge)

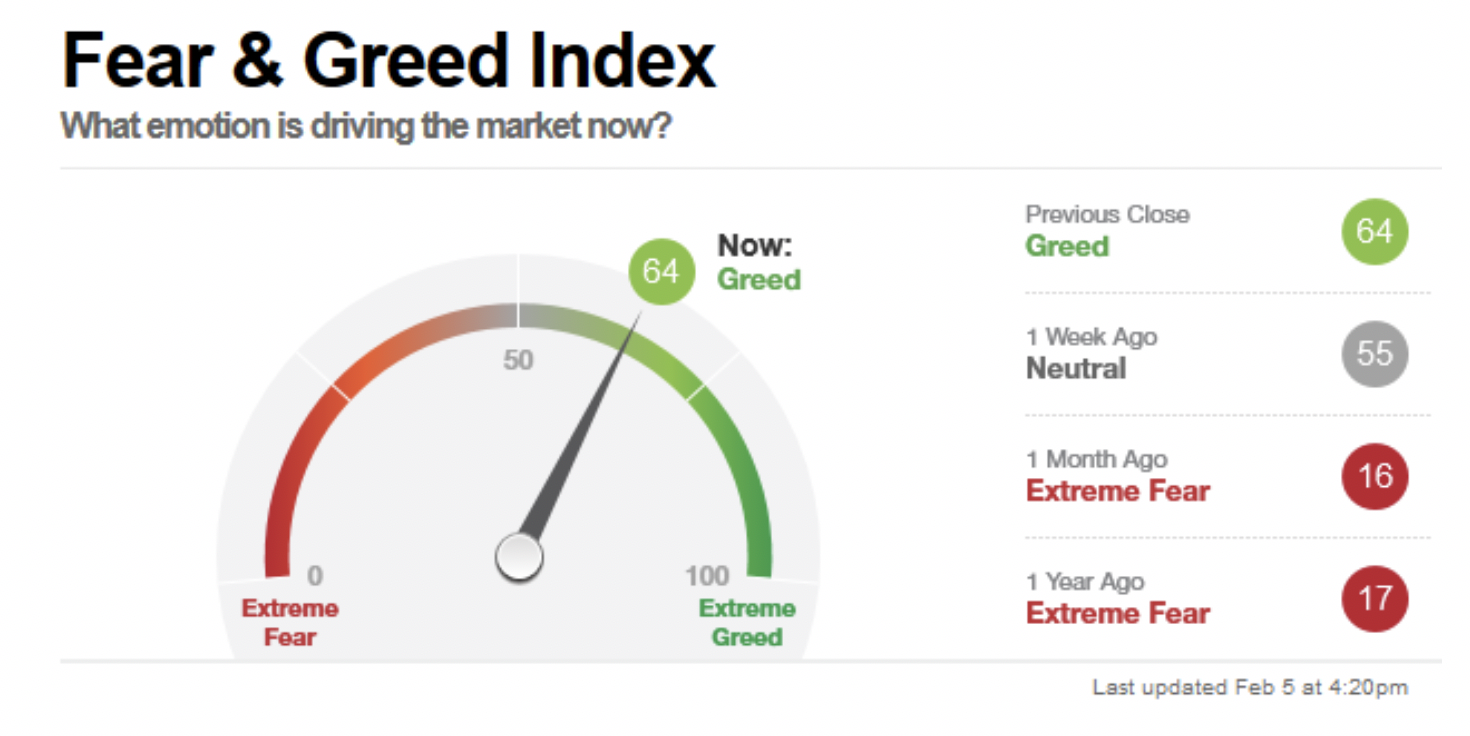

(Click to enlarge)

Source: CNN Money

End of easy money?

Something funny happened towards the end of 2018. According to a survey conducted by Bank of America Merrill Lynch on global fund managers, for the first time since the Great Recession, investors wanted companies to prioritize paying down their mountains of debt as opposed to dividend hikes or bigger buybacks.

The office of Financial Research had earlier flagged corporate debt as a potential problem after years of easy money had led to overleveraged balanced sheets. A cross-section of analysts predicted that 2019 would be defined as a big year for deleveraging. Related: Slack Seeks $10B Valuation For Direct IPO

But so far, the evidence coming in suggests just the opposite-- that the era of easy money remains very much alive.

Investor appetite for high-yield bonds is showing no signs of waning even after hitting a crescendo in 2018. This was clearly demonstrated over the past week after investors pumped billions of dollars into high-risk investments.

Crisis-prone Greece had little trouble amassing blockbuster orders for its $2.5 billion-euro ($2.9 billion) bond sale, while serial-defaulter Ecuador was able to sell $1 billion in new bonds as the government continues talking to the IMF for a new round of funding. Meanwhile, the frontier nation of Uzbekistan is getting ready for a debut international offering, no doubt encouraged by the blossoming risk-on environment.

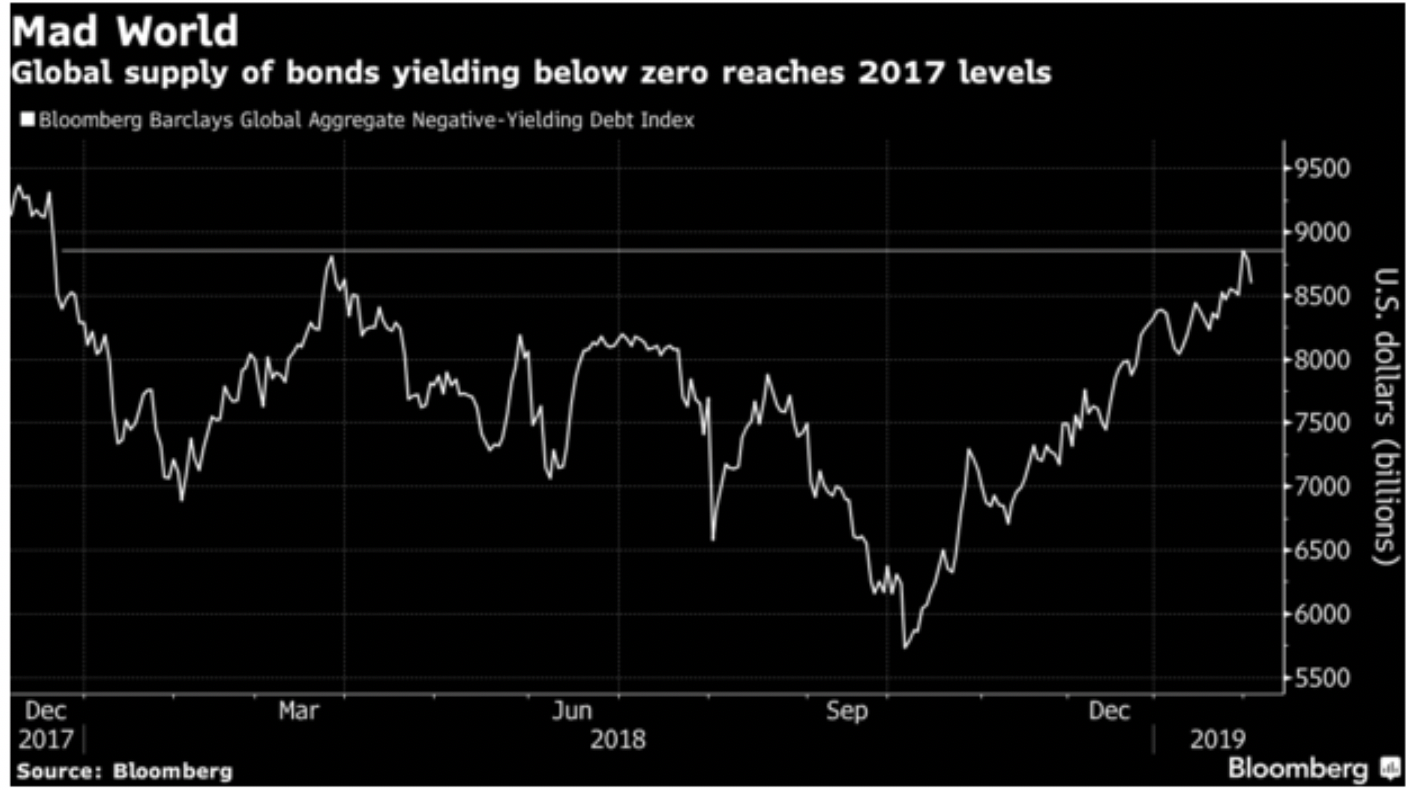

Here in the U.S., high-yield investing is looking to make a rebound as the market hopes that the easy-money policy will prolong the business cycle that was earlier feared to be on its last legs. That asset class has already posted the biggest monthly gain in seven years and the world is now awash in negative-yielding bonds to the tune of $8.6 trillion, a level they last touched two years ago.

(Click to enlarge)

Source: Bloomberg

Negative bond yields is an anomalous situation where bond issuers are actually paid to borrow. This happens when bond prices keep climbing, usually due to high demand, and depress yields. Bond yields move inverse to prices. At some point, the price of the bond increases sufficiently implying negative yield for the purchaser.

Bad news is good news

So, has the fiscal environment improved so dramatically to warrant such a gung-ho attitude?

Short answer—‘no’; on the contrary, what we are witnessing is a replay of the post-crisis thinking where the market views bad economic news as good news for the investment markets.

Related: Italy’s $1.7 Trillion Debt Could Threaten The EU

The thinking here is that the unfolding economic malaise (bad news) will encourage more dovish policies by the Fed and other central banks that will prove enough to offset any economic slowdown and even boost risk assets (good news).

As James Athey, senior investment manager at Aberdeen Standard Investments, has aptly noted:

“Markets have shown repeatedly in the past the extent to which they can ignore economic and political reality when they feel that central bank policy is a tailwind. ”

If you’re inclined to more risk-taking, Wall Street seems to agree with you. According to BNP Paribas, the case to be tactically bullish can be made squarely on the dovishness of central banks. Meanwhile, Morgan Stanley, chief economist Chetan Ahya has also given risk-takers the greenlight predicated on a recovery of global markets and easing trade tensions between the Washington and Beijing.

Others like HSBC, though, have warned against complacency over the ongoing monetary largesse by pointing out that markets could quickly reverse gains if upbeat economic data pushes the Fed and ECB back to the tightening path.

By Alex Kimani for Safehaven.com