The biggest trade spat in recent history has just turned from a skirmish into a full-blown trade war, and Wall Street darlings are bearing its full brunt.

The rapidly escalating trade tensions between the United States and China following Beijing’s retaliatory tariffs on Monday morning have rocked financial markets and wiped off more than $1 trillion from global equities in the worst one-day sell-off since January.

Concluding a 5-day stretch of steep losses, the Dow Jones Industrial Average (INDU), having dropped more than 700 points at one point, managed to pare back some losses to still finish a whopping 617 points lower, or -2.38 percent. The index has now lost a cumulative 1,114 points over the last five trading sessions, or 4.2 percent.

Leading the rout were the Dow’s biggest names, especially those with a heavy presence in the Middle Kingdom:

- Apple, Inc.(NASDAQ:AAPL)—fell 5.8 percent on the day; now 20 percent off its 52-week high

- Boeing Corp.(NYSE:BA)—finished the day 4.9 percent lower and now trades 24 percent off its 52-week high

- Caterpillar, Inc.(NYSE:CAT)—dropped 4.6 percent to finish the day 22 percent below its 52-week peak

- Intel Corp.(NASDAQ:INTC)—the chip giant slipped 3.1 percent to close 25 percent below its 52-week high

- 3M Corp.(NYSE:MMM)—lost 1 percent and is now 21 percent off its 52-week high

At the closing bell, the broad market benchmark, S&P 500 Index (SPX), had tumbled 2.41 percent while the tech-heavy Nasdaq Composite Index (COMP) cratered 3.41 percent to complete its worst day so far this year.

(Click to enlarge)

Interestingly, even the American small-cap benchmark, Russell 2000 Index (RUT), was not spared, losing 3.18 percent. That’s a bit anomalous because small-cap companies are supposed to withstand market shocks like trade spats better than large companies. That’s mainly because they don’t rely on international markets as much, with only 20 percent of their revenue derived from foreign markets compared to 33 percent average for the S&P 500.

(Click to enlarge)

The Wall Street plague rapidly metastasized to international markets.

The pan-European STOXX 600 Index (STOXX) closed 1.2 percent lower while the iShares MSCI China ETF (MCHI) lost 3.81 percent on the day and 7.78 percent over the past five sessions. Emerging markets were badly walloped, too, with the iShares Emerging Markets ETF (EEM) closing the day 3.33 percent lower.

Indeed, Monday’s sell-off marked a major global equities market reset with everything getting slammed. Country-based ETFs including Germany, Brazil, South Korea and Mexico were all down 2-4 percent.

All in all, global stock markets shed ~$1 trillion on the day.

Half-hearted rebound?

Equity markets across the globe have opened Tuesday’s session on a brighter note, with all major markets staging a tentative rebound.

The Dow Jones is up 190 points or 0.75 percent at 10.30am ET while the S&P 500 has gained 0.76 percent. Meanwhile, the Nasdaq Composite is up 0.99 while the Russell 2000 has gained 0.55 percent.

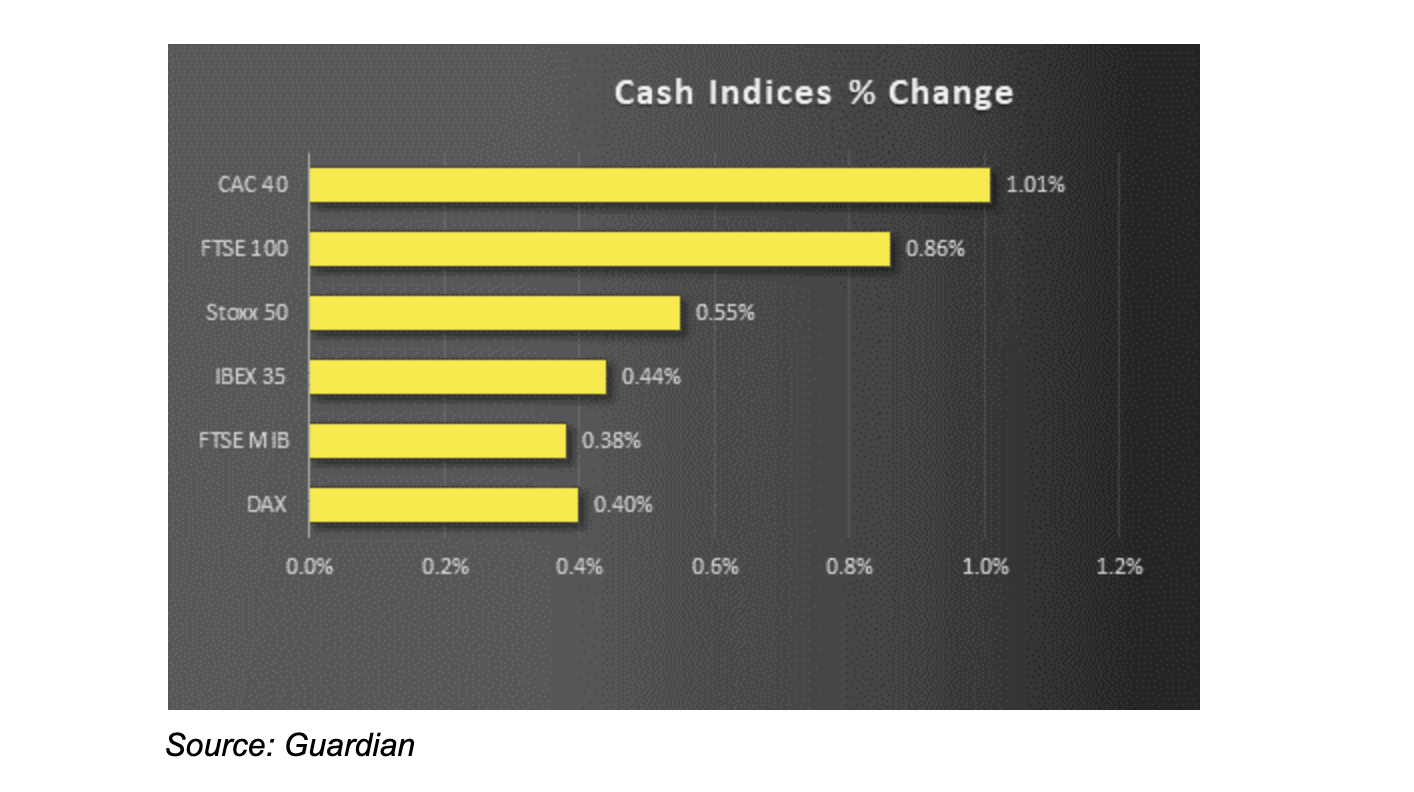

In the international arena, STOXX has rallied 0.64 percent with all regional index’s in the green.

(Click to enlarge)

Commodity prices are also enjoying a nice upswing:

(Click to enlarge)

Source: The Guardian

However, the biggest winners so far are China and emerging markets, with their respective index’s clocking gains of 1.58 and 1.40 percent, respectively, at the time of going to press.

That said, it would be a stretch to surmise that the storm is over from the early rally. Volatile gyrations are usually marked by up and down swings and Tuesday’s is simply a non-spectacular upswing so far.

Rather, it’s quite likely that President Trump’s latest tweets have helped calm the mood.

In one tweet on Tuesday morning, the president kept hope alive after declaring that the two warring nations will strike a deal ‘‘…when the time is right…’’

(Click to enlarge)

In another, Trump expressed hope that China’s central bank will lower interest rates to counter the damage wrought by the trade war, which in turn would force the Fed’s hand.

At first blush, the suggested rate cuts might sound like wishful thinking by the president given Beijing’s ongoing deleveraging drive in a bid to clean up its financial markets and clear out bad debts.

However, some economists actually hold Trump’s position and opine that the PBOC might have to cut rates sooner or later in the face of China’s deteriorating economy. Rate cuts in China would devalue the yuan and make the dollar too strong therefore making America’s exports expensive and uncompetitive. To counter this, the Fed might be forced to follow suit and lower rates as well.

That’s exactly what Trump, and the markets, have been wishing for.

Cautious optimism might, therefore, be the right strategy to adopt at this point. After all, Bank of America’s latest survey found that U.S.-China trade war remains the biggest ‘tail risk’ that could derail the markets. According to the survey, a third of fund managers have hedged their portfolios against a sharp market correction over the next few months.

Retail investors should probably follow suit.

By Alex Kimani for SafeHaven.com

More Top Reads From Safehaven.com: