This rise of populism is creating murky financial waters for both emerging and developed markets. Case in point, Italy, where the new populist government is willing to give the people what they want: A break from austerity. But it’s a dangerous move that represents “irresponsible fiscal policy”, Michael Hasenstab, chief investment officer at Templeton Global Macro, told CNBC.

Hasenstab describes populist-led fiscal policy as “probably one of the most important political variables we have to look at” when considering investments.

Italy’s new coalition government is anti-establishment—and anti-austerity, and it’s promising all sorts of things that the country can’t afford, including tax cuts, basic monthly wage guarantees and more.

Italy’s populist leaders don’t have enough wiggle room to take on more debt, and they’ll find that out when Italian bond yields rise further. From an investors’ perspective, this is what will bring down Rome.

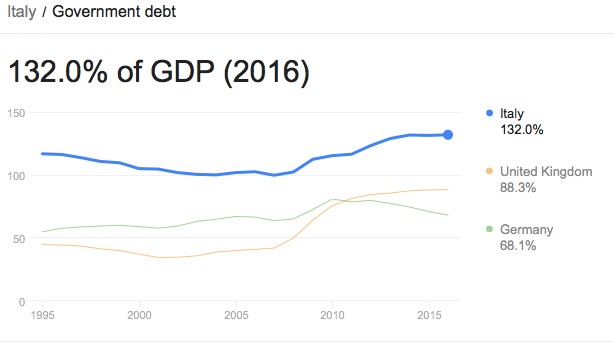

Italy’s national debt is at 132 percent of GDP and it’s got one of the slowest growth rates in the euro zone, with unemployment at 11.2 percent. And the European Union has mandated austerity since the beginning of the decade. The new government doesn’t feel like bowing to the EU’s monetary guidance, and it’s rebellion is increasingly popular with a public that has grown tired of living under austerity.

(Click to enlarge)

Italy’s 2.3-trllion euro national debt is worse that Greece. The EU says Italy is courting disaster, facing a massive debt restructuring challenge. And it’s not just a threat to Italy, but to the euro itself. Related: IMF Warms Of Potential Economic Meltdown

Still, Italy’s populist government is bent on fighting the EU. As recently as last week, it said it sought to triple the 2019 budget deficit plan of the preceding government.

Italy’s financial irresponsibility is sparking cries of everything from “complete insanity” to “sleepwalking into a next crisis”, Reuters reports, citing senior EU officials.

“When Tria talked about planning a deficit of 2.4 percent for the next three years in the Eurogroup, jaws dropped everywhere,” Reuters quoted one senior euro zone official as saying. “The mood was that this was really a terrible signal.”

And while Italy may be the worst-case scenario, it’s not the only venue where populism is threatening fiscal policy.

Germany is also on Hasenstab’s red flag radar because the far-right is increasingly posing a challenge to the mainstream government. It’s more than just a fleeting concern, too. A new study indicates that populist attitudes are on the rise in Germany—and its coming from the political center.

According to a Bertelsmann Foundation study cited by DW, one in three voters now sympathizes with populist policies.

So who’s not on Hasentab’s red-flag watchlist? Oddly enough, India and Indonesia. Both countries have unenviable current account deficits; and both are experiencing currency issues, but Hasentab says that despite all, both are “the type of investment we are looking for”.

In fact, the World Bank this week said that Indonesia’s weak rupiah is actually a source of strength, Bloomberg reports.

“With a flexible exchange rate now, moderate devaluation makes imports more expensive, exports cheaper, and the dollar value of profit transfers lower,” Rodrigo Chaves, World Bank country director for Indonesia and Timor-Leste, said in a statement on Wednesday. “These elements reduce the current-account deficit automatically.”

The Indian rupee, however, hasn’t enjoyed any such statements from the World Bank, and on Wednesday it closed at its weakest level, opening even weaker Thursday, having lost some 15 percent this year already. Some analysts are warning that the rupee could fall as low as 75 per dollar this year, pushed down by trade wars and rising crude prices.

But this isn’t populist-promoted fiscal irresponsibility.

Related: Markets Open Slightly Lower Ahead Of Monthly Job Data

Hasenstab notes that India's current account deficit has been negatively affected by rising oil prices, not fiscal irresponsibility.

"We still have a very long-term positive view for both India and Indonesia. And we talk about a current account deficit, but really, both of those countries have dealt with oil at a higher price," he told CNBC. "Both countries are pursuing some very sound, be it fiscal policy, or in India's case, really revamping the monetary system ... inflation targeting, tax reform."

He might agree with the World Bank’s statement on Indonesia—for India, too. Both countries he describes as a “long-term anchor”.

But hedge funds and other investors love the clarity of political situations, like the clear rise of populism in Italy, because it helps to better pinpoint investments. In this case, the new buzz word for political risk is “populism”, and now we’ve got a list.

By Josh Owens for Safehaven.com

More Top Reads From Safehaven.com: