For many index investors, the art of stock picking is an exercise in futility given that most stock pickers tend to lag the market. While it’s certainly true that most actively managed mutual funds more often than not underperform broad-based indexes such as S&P 500 or the FTSE 100, a stock picker can reduce the risk of making bad picks by looking at monopolies, duopolies and oligopolies (MDOs).

MDOs generally boast wide economic moats and better profit margins than their peers in the same sector. They also tend to be less sensitive to poor business cycles and weak economies, meaning an investor can hold them through recessions with minimal capital erosion.

True monopolies and duopolies tend to be rare outside government regulated utilities; oligopolies, on the other hand, are scrutinized by antitrust regulators but still face less regulatory gauntlet than the other two groups.

Oligopolies are markets dominated by just a handful of companies.

Here are five oligopolies in five different sectors that you should include in your portfolio.

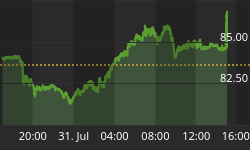

#1 eCommerce: Amazon Inc.

Market Cap: $879.46B

YTD Share Returns: 18.1%

Amazon Inc. (NASDAQ:AMZN) is undoubtedly one of the most recognizable brand names in the retail and ecommerce world. AMZN has been an amazing stock to own, returning 430% over the past five years though its has lagged the S&P 500 this year with returns of 18.1% vs. 25%. The underperformance can be chalked up to its Q2 and Q3 profit miss coupled with light holiday guidance with the stock tumbling 12% since the July earnings scorecard.

Nevertheless, the long-term bullish thesis for AMZN remains intact. From its modest roots as an online bookseller two decades ago, Amazon has enjoyed explosive growth to become the undisputed ecommerce leader in North America with 43.5% of the US ecommerce market, over 300 million active users and sales of more than 3 billion products each month. During the last quarter, the company’s revenue climbed 24% to $70B and has guided for Q4 net sales of $80B-$86.5B. Operating cash flow increased 33% to $35.3B, while free cash flow clocked in at $23.5B vs. $15.4B for last year’s corresponding period.

What makes Amazon a tough customer to beat in the ecommerce sector is its cloud business, Amazon Web Service. AWS contributes nearly 60% of Amazon’s operating income thus allowing the online seller to seriously undercut other retailers by offering low prices on most of its products. Although AWS growth has lately been slowing down due to intense competition from rival public clouds such as Azure and Google Cloud, it’s 35% revenue growth clip to $9B last term is still impressive given its sheer scale. A month ago, AWS famously lost the hotly contested $10B JEDI contract to Microsoft Corp.’s Azure but seems to have partly made up for it after winning a new customer in Wester Union.

Amazon has lately been in Washington’s crosshairs with threats of antitrust investigations. Some, however, see it as nothing more than president Trump’s idle bluster and personal vendetta against Amazon CEO Jeff Bezos and see the investigations going nowhere.

No less than 42 analysts rate AMZN stock a Buy.

#2 Personal Computing: Microsoft Corp.

Market Cap: $1.15T

YTD Share Returns: 48.9%

Whereas many people consider Microsoft the biggest name in PCs and personal computing, the company is in fact an oligopoly in several markets. Microsoft is an oligopoly with Apple Inc.(NASDAQ:AAPL) in personal computing devices/operating systems; a leader in enterprise software alongside Oracle Corp. (NYSE:ORCL) and IBM Corp. (NYSE:IBM) and a video game giant together with the likes of Sony Corp. (NYSE: SNE) and Nintendo Co.

Indeed, Microsoft did face antitrust allegations by the government of the United States back in 2001 for unlawful monopolization of Intel-based personal computers. Microsoft lost the case but won the appeal thus forestalling a looming break up of the company. Nowadays, the symbiotic nature between Microsoft and its hordes of vendors as well as the scale of corporate lock-in means that attempting to extricate the all-powerful Windows System from even a small corner of the PC and corporate world would require a truly Herculean effort-- just ask Linux. The company though faces little danger of a fresh round of antitrust litigations.

MSFT is enjoying a phenomenal run with the stock tucking on gains of nearly 50% in the year-to-date and 219% over the past five years.The biggest reason why the stock has been flying is due to the company’s continuing success in the transformation from a company that sells on-premise licenses to one that does business in the cloud. A decade ago, Microsoft was in grave danger of becoming a tech also-ran after being left out in the mobile revolution thanks to its stubborn ‘Windows First’ mentality.

Luckily, the company finally came to its senses and agreed to ball in the cloud, creating a very successful platform-agnostic hybrid cloud operation. The strategy has been paying off--last term, Microsoft posted 14% topline growth to $33.1B with a well-balanced performance across all its segments.

Wall Street is highly bullish on the company with 26 Buy recommendations and 0 Sell.

#3 Internet Products: Alphabet Inc.

Market Cap:$892.8B

YTD Share Returns: 26.2%

Alphabet Inc.(NASDAQ:GOOG)is a holding company, better known as the parent company of internet search giant Google. The conglomerate runs dozens of businesses including Google, CapitalG, Waymo, Verily, Nest, Calico, GV, Access and X. Google is the biggest and most prominent of these, responsible for a multitude of internet products such as Search Ads, Maps, Youtube, Commerce, Android, Google Cloud, Google Play and Chrome as well as a variety of hardware products. The company also recently acquired fitness gear manufacturer Fitbit Inc. in a $2.1B deal.

Alphabet makes the lion’s share of its revenue in online advertising (84% in Q3) where it shares a virtual duopoly with Facebook Inc.(NASDAQ:FB) though Amazon is fast catching up. According to eMarketer, Google will command 36.2% of US digital ad spend in 2019 vs. 19.2% share by Facebook. Google’s main forte is search ads where it gobbles up 73.1% of ad dollars totaling $40.3B. Google has its extremely popular search engine to thank for its online dominance, commanding 75.7% of desktop and laptop searches globally in the month of August. Related: Even Banks Can't Answer Aramco's Trillion Dollar Question

Alphabet has lately come under pressure after it announced a 23% Y/Y decline in third-quarter earnings hurt by increasing investments in R&D and marketing. Notably, the company’s traffic acquisition costs (TAC) have skyrocketed from $3.5B four years ago to $7.5B last term. TAC is the money Alphabet pays companies like Apple for Google to become the default search engine in their devices. Meanwhile, Alphabet and Facebook face possible antitrust probes by the DoJ.

Nevertheless, Google still enjoy a considerable moat in online advertising and is favored to remain the market leader for many years to come. The company has 32 Buy and 7 Hold ratings on Wall Street.

#4 Social Networking: Facebook Inc.

Market Cap: $569.75B

YTD Share Returns: 52.1%

Facebook Inc. (NASDAQ:FB) is the world’s largest social network with 2.45B monthly users. Like Alphabet, FB is both admired and loathed due its dominance in digital advertising with the company lately coming under intense scrutiny over several data privacy lapses. The company also owns popular apps Instagram, WhatsApp and Messenger.

Despite its struggles, FB continues to be a growth machine: the company reported Q3 revenue increase of 29% to $17.65B, operating earnings were up 24% while net income grew 19%. The company was also more than able to offset a 6% decline in ad pricing with a 37% increase in ad impressions--a true testament to the stickiness of the app.

Facebook is even more reliant on ad dollars than Alphabet, with 98% of its revenue coming from the segment last term. With the global online ad industry forecast to grow at a healthy 10.2% clip through 2024 coupled with FB’s strong positioning in the industry, the company has plenty of growth runways ahead.

FB stock 39 Buy, 5 Hold and 1 Sell ratings.

#5 Mass Media Entertainment: Walt Disney Co

Market Cap:$267.3B

YTD Share Returns: 39.0%

Walt Disney Co(NYSE:DIS) is one of the six U.S. media outlets that dominate the cable entertainment industry (combined market share of 90%).The company position in the industry was significantly enhanced after it completed the merger with 21st Century Fox in a $71.3B deal. The company is also highly successful in the movie-making business, with its 26% share of the domestic box office market placing it in pole position.

Like its cable peers, DIS stock has lagged over the past couple of years due to rampant cord-cutting. The company’s prized gem, ESPN, has been bleeding subscribers at an alarming rate, losing 15 million viewers over the past eight years as users favored skinny bundles. Thankfully, the segment appears to have stabilized.

Netflix Inc. (NASDAQ: NFLX) would have been our favorite entertainment pick had we compiled this list a year ago. However, the company’s latest struggles with subscriber growth coupled with the fact that Disney+ has been enjoying such impressive adoption suggests that Netflix is likely to face even more pressure ahead. Disney launched Disney+, a $6.99/month online streaming subscription service, two weeks ago to little fanfare. However, the project is already looking like a resounding success with the New York Post reporting that the app has been adding IM new subs everyday. Wedbush's Dan Ives sees the new app as a legitimate competitor to Netflix.

Walt Disney has 17 Buy, 5 Hold and 0 Sell ratings.

By Anes Alic for SafeHaven.com

More Top Reads From Safehaven.com: