Swamped with debt from credit cards, healthcare and prescription drugs, America’s seniors are now increasingly turning to reverse mortgages to avoid poverty and survive retirement. That means inheritances are becoming a thing of the past.

Trump’s Tax Cuts and Jobs Act from December 2017 has potentially worsened the inheritance situation because it raised the threshold on medical expense tax deductions and placed a cap of $10,000 on the itemized deductibility of state and local taxes.

Social Security is the major source of income for most of the elderly, with 21 percent of married Social Security recipients and 43 percent of single recipients aged 65 and older depend on this for 90 percent or more of their income, Social Security Administration data shows.

The average senior will get $17,532 in Social Security benefits for 2019. And while many think that's better than nothing, these benefits will replace about 40 percent of the average earner's income before retirement, which isn’t even close to enough for a decent life in retirement. One trip to the hospital for something non-life-threatening, and that’s blown.

Of course, how far that $17,000 goes depends a lot on where you live, but either way, it’s a drop in the bucket. According to Go Banking rate, the most expensive state for retirement is Hawaii with retirement cost around $118,000, and the cheapest is Mississippi, coming in at around $53,000. Not only are inheritances fast going out of style, but one-third of senior households don’t even have any money left over each month, or is in debt after meeting essential expenses, according to the Institute on Assets and Social Policy.

Related: Turkey Blames The West For Pre-Election Lira Volatility

That’s where reverse mortgages suck away your inheritance.

It’s home equity that allows seniors to fund retirement these days. But it’s a highly painful solution for most because that debt is repaid with the sale of their homes, typically after death. So while children are less likely to inherit much of anything, at least they won’t inherit mortgage debt in this case.

Despite not being able to offer their children an inheritance--the dream of any proud parent--Americans are still oddly optimistic when it comes to retirement.

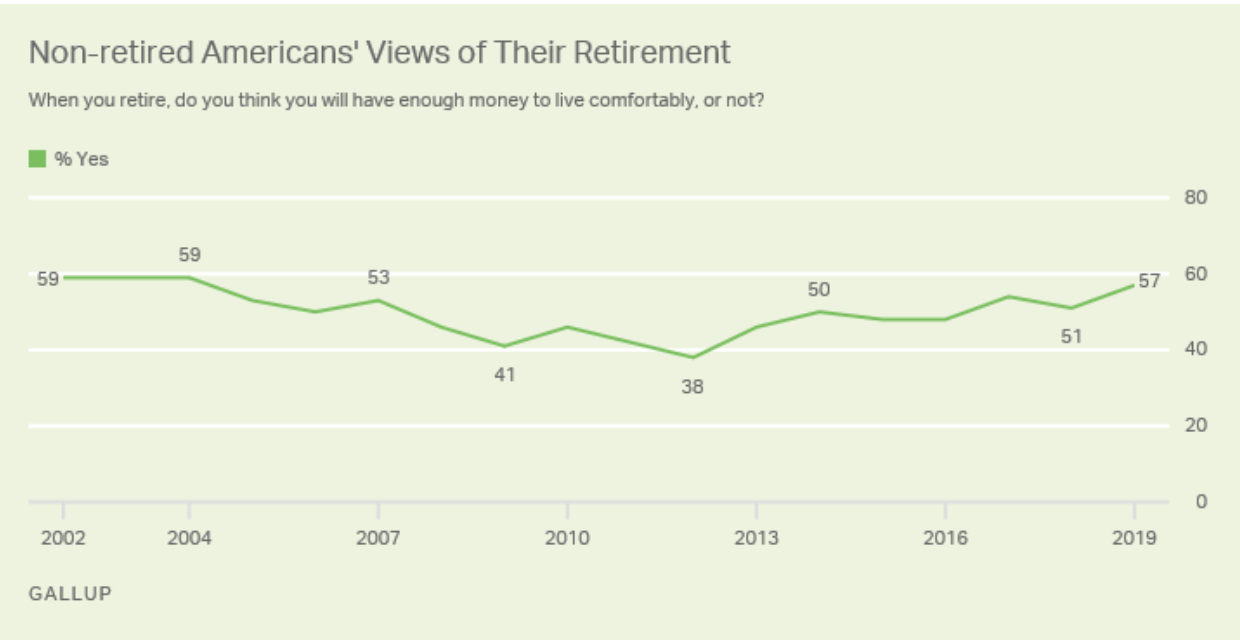

According to a recent Gallup survey, a near record 57 percent of non-retired Americans now expect that they will have enough money to live comfortably in retirement, while 41 percent do not. That’s even with 57 percent of retirees relying on Social Security as major part of their income, and 33 percent of non-retirees expecting to do the same.

(Click to enlarge)

Source: Gallup

Indeed, it makes us question their ability to add numbers--but optimism is always a good thing.

At the same time, new data shows that homeowners aged 62 and older have seen their collective housing wealth increase by 2.7 percent for the first quarter of this year, hitting a record $7.14 trillion, according to the National Reverse Mortgage Lenders Association (NRMLA).

But that’s not the only data to look at it. Those gains were offset by a massive $6.5-billion increase in senior-held mortgage debt.

Any way you look at it, senior assets are melting away.

By Michael Scott for Safehaven.com

SInce 2007-9 most have forgone credit cards and switched to debit cards.

Healthcare is free.

Prescriptions are about $6 for half the year and then become free.

My wife is taking one drug that is normally 4K+ per month but now free.

Is senior debt increasing? It certainly could be but it is not attributed to reverse mortgages. Please confirm your facts before making broad-based assumptions. Thank you.