After a disappointing start to the year--the sector’s favorite benchmark, SPDR S&P Bank ETF (KBE), was down 1.3% YTD vs. a 1.64% gain by the S&P 500 prior to the earnings session-- banking stocks are looking to stage a major rebound with bumper earnings on deck by the so-called megabanks. And so far, they have not disappointed, which comes as a surprise given the particularly tough backdrop of a low-interest rate environment.

JPMorgan Chase & Co. (NYSE:JPM), Citigroup Inc. (NYSEC) and Wells Fargo & Co. (NYSE:WFC) have returned their Q4 2019 earnings scorecards on Tuesday morning in the pre-market session with the first two impressing while WFC has, unsurprisingly, lagged its peers.

High Expectations

Expectations for the sector were already high as the start of a bank-heavy reporting period kicked in.

And the giant banks so far seem up to the task.

JPMorgan, the largest U.S. bank by assets, kicked off the session in style after managing to crush Wall Street estimates. JPM has reported Q4 Revenue of $28.3B (+8.4% Y/Y), beating Wall Street’s consensus by $610 million while fourth-quarter profit climbed 21% to $8.52 billion, or GAAP EPS of $2.57, thus exceeding analysts’ consensus estimate by $0.22.

JPM’s trading division shot the lights out, managing to more than offset the impact of low-interest rates across retail and commercial banking. Bond trading revenue grew a robust 86% to $3.4 billion, easily beating the $2.61 billion estimate with fixed-income desks roaring. Stock traders did not disappoint either, posting a 15% increase in revenue to $1.5 billion and $150 million above the estimate.

JPM shares jumped 2.1% in early morning trading and moved to the green for the first time in the new year.

The country’s fourth-largest bank, Citigroup, has not been a slouch either, posting equally impressive results thanks to the exemplary performance by its fixed-income division.

Citi posted fourth quarter revenue of $18.38B (+7.4% Y/Y) thus beating the Wall Street consensus by $430 million. Earnings for the quarter clocked in at $5 billion, or $1.90 per share vs. $1.84 per share expected by Refinitiv. Fixed-income trading revenue of $2.9 billion was good for a 49% Y/Y increase and more than double the growth clip forecast by analysts surveyed by Bloomberg.

The bank’s consumer business performed well, with its global consumer banking division raking in $8.5 billion in sales, or a 5% Y/Y increase.

Unlike JPM, however, Citi’s equities trading division underperformed with revenue of $516 million, representing a 23% decline compared to the previous year’s corresponding period. Citi’s management chalked up the poor performance to a tough derivatives trading environment.

Citi shares have come off the blocks flying, gaining nearly 3% in the morning session.

Last year, the shares put up their best performance in two decades after finishing the year with a 53% gain. Those gains easily outpaced those by its five rivals though JPM and Bank of America (NYSE:BAC) gained more than 40% each.

Wells Fargo was the laggard of the group, which is becoming the new norm given its checkered history of major scandals. The mortgage-lending giant is still reeling from a scandal of a decade ago in which its staff created millions of fake customer accounts in a bid to attain lofty sales goals.

Wells Fargo’s fourth-quarter results missed both on the top-and bottom-line estimates.

Revenue of $19.86B (-5.3% Y/Y) was $250 million below the Wall Street consensus estimate while net income of $2.87 billion was more than 50% below the $6.06 billion the company posted a year ago.

Related: Last Chance To Buy Apple Before 2020 Run

Alarmingly, WFC’s efficiency ratio continued to deteriorate, with the fourth quarter’s metric clocking in at 78.6% compared to 69.1% in Q3 and 63.6% a year earlier. The bank efficiency ratio is a quick measure of its ability to turn resources into revenue. The lower the ratio, the better with 50% generally regarded as the maximum optimal ratio. A rising efficiency ratio indicates either decreasing revenues of increasing costs--both of which WFC is symptomatic of.

Newly installed CEO and President Charlie Scharf, who took over the reins at the company three months ago, decried the company’s high-cost structure but expressed optimism that there were many areas where the bank could still return to growth.

WFC shares have plunged 4.1% after the earnings call and are looking to repeat another poor year after they underperformed their peers in 2019.

Room To Run

After a strong year in 2019, the banking sector has overheated and many stocks in the space appear overvalued. The financials finished last year as the third-best performing sector. The million-dollar question now is: can the banking sector sustain the momentum? More importantly, are there any bargains in the sector?

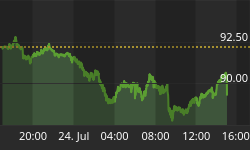

Newton Advisors has told CNBC’s Trading Nation that the group as a whole is overvalued, but Goldman Sachs is still a better bet than the likes of Citi and BAC which are approaching 52-week highs. Newton thinks Goldman Sachs still has room to run and is displaying good momentum.

GS shares have rallied 7% in the year-to-date, one of the sector’s better performers thus far.

(Click to enlarge)

Source: CNN Money

The good part: the sector is flush with cash, and banks are likely to start returning tons of it to shareholders via dividends and buybacks.

By Anes Alic for SafeHaven.com

More Top Reads From Safehaven.com: