The eurozone’s third-largest economy, Italy, is marooned in a deep political and economic crisis, with seeming endless problems: an economy that has barely grown in decades, sky-high unemployment rates, ballooning national debt, an inability to form a stable coalition government and, lately, a looming showdown with the EU over mounting debt.

These have precipitated a wave of populism that has rejected the old establishment and brought in a new guard.

Unfortunately, that has done little to resolve another Italian bugaboo: a massive banking crisis.

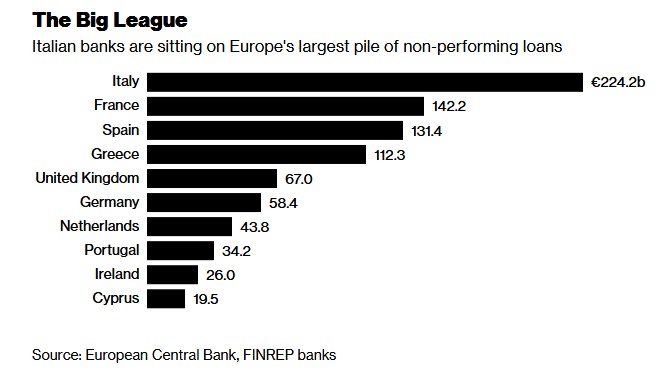

European banks have accumulated about $1.2 trillion in bad and non-performing loans (NPLs) that have continued weighing down heavily on their balance sheets. Italian banks are sitting on the biggest pile of bad debt: €224.2B ($255.9B), with NPLs and advances making up nearly a quarter of all loans.

As if that is not bad enough, the banks now have to contend with potentially heavy penalties coming from Brussels after Italy’s recalcitrant leadership refused to revise the country’s fiscal 2019 budget to lower debt and borrowing.

The sharks can already smell the blood in the water, and investors have been shorting Italian banking stocks to death. Italian banks hold nearly a fifth of the country’s government bonds.

(Click to enlarge)

Source: Bloomberg

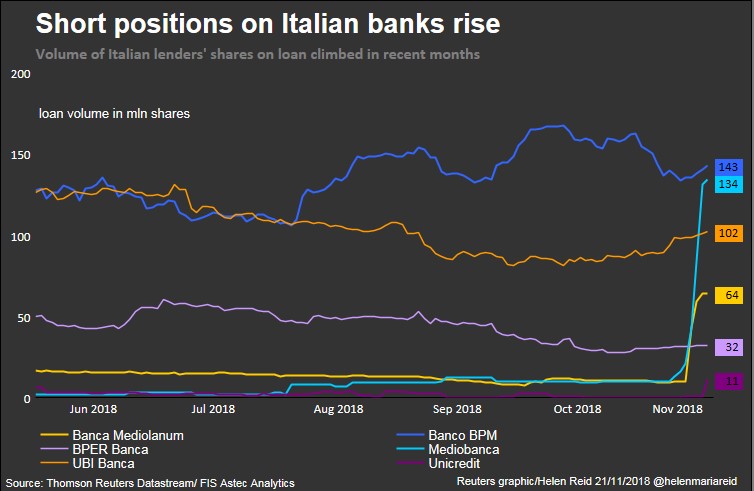

(Click to enlarge)

Source: Reuters

Short sellers have mainly been targeting medium-sized lenders as well as asset manager Banca Mediolanum and investment bank Mediobanca. According to FIS Astec Analytics data, the volume of these banks’ shares on loan—a good proxy for short interest—has shot to its highest in 15 months.

Short interest on Mediolanum’s shares now stands at 8.7 percent of outstanding shares, while Mediobanca has 15 percent of its shares sold short.

Rome Refuses To Back Down

Investors seem justified in their pessimism on the Italian banking sector—if the latest developments are any indication.

A month ago, the European Commission rejected Italy’s 2019 budget on grounds that it flouted EU requirements and Italy’s commitment to lower its expanding budget deficit. The latest budget hiked the deficit to 2.4 percent of GDP--way higher than the targeted 1.8 percent this year. Meanwhile, total debt sits at a staggering 130 percent of GDP, the fourth highest in the world. The EC rules are clear: national debt should be maintained below 60 percent of GDP while deficit should not exceed three percent of GDP

Italy's deputy prime minister Matteo Salvini, however, has sent strong signals that the country will not back down from the current budget or revise it to satisfy EU requirements. He has even accused the bloc of "hypocrisy and double standards.’’ Related: Saudi Aramco Abandons $40 Billion Bond Sale

Speaking to France24 on Tuesday, Mr. Salvini balked at the whole idea saying:

"Who has complied with rules in the past? Not Germany, not France, not Spain. Spain had an average deficit way above the rules. It’s double standards. What is 2.4? That is the point."

Although Mr. Salvini is right in his assessment that the commission has allowed exceptions to the rules in the past (including in 2016 when it turned a blind eye to France’s debt prompting EC president to famously quip "France is France"), not reacting [to Italy] is not an option, as Wolfango Piccoli, co-president of EC advisory firm, Teneo Intelligence, has noted.

The Moment of Truth

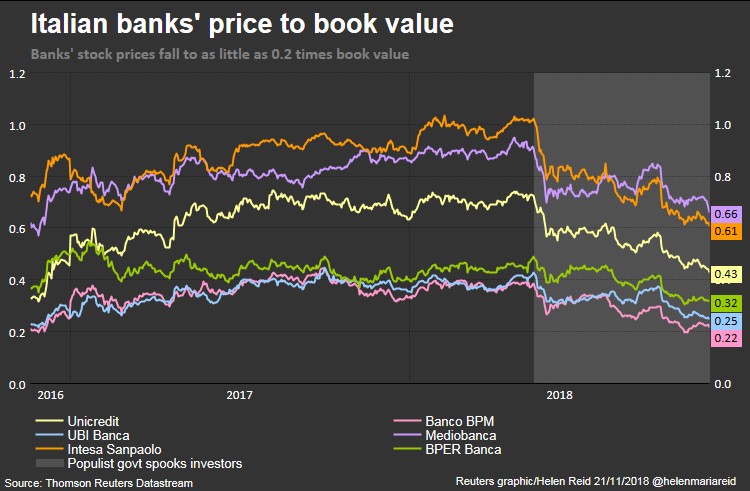

Some Italian politicians have been seeking curbs on the short selling in a bid to prevent a rise in bond yield spreads. While a ban on short-selling might alleviate short-term selling pressure, the moment of truth always arrives in the end… determined by underlying fundamentals. The continuing challenges on the Italian banking sector directly affects returns on shareholder equity, and will continue to reflect on share prices:

(Click to enlarge)

Source: Reuters

By Alex Kimani for Safehaven.com

More Top Reads From Safehaven.com: