The U.S. housing market is crumbling--a worrying indication that an economic catastrophe could be brewing. Yet, nobody seems sure why this is happening in an economy that remains hale and hearty by most measures.

But don’t rush to your banker just yet hoping to get an easy deal. Rejections for mortgages and refinancing applications have, unfathomably, shot up to record levels.

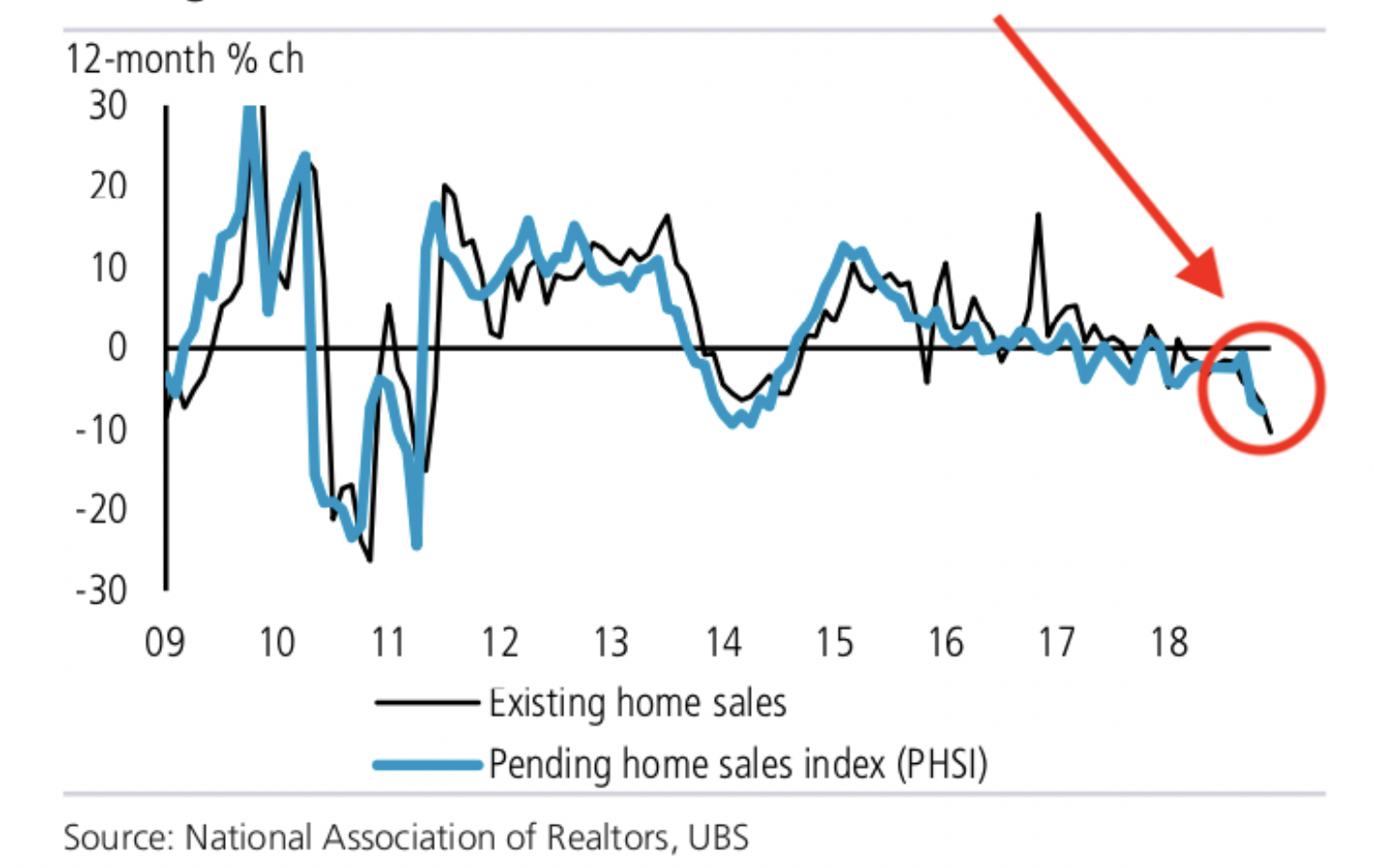

U.S. existing home sales (which make up about 90 percent of U.S. home sales) fell off a cliff in 2018, with mortgage lenders recording a sharp fall in applications, originations and profits.

Existing home sales cratered a massive 10.3 percent year-over-year and 6.4 percent month-over-month in December to just 4.99 million units. That was several multiples worse than the 1 percent month-on-month decline that a Reuters survey of economists had projected. It also marked the lowest level of sales in three years and the steepest decline in seven years. Home sales declined on a year-over-year basis in every month apart from February, a trend that grew more aggressive towards the tail-end of the year given the 5.1 percent and 7.8 percent declines in October and November, respectively.

(Click to enlarge)

Source: Business Insider

Meanwhile, banks with large mortgage-lending segments are particularly feeling the heat from the home-buying malaise.

During the last quarter, Wells Fargo, the largest bank mortgage originator, saw its mortgage income plunge 50 percent to $467 million, while originations fell 28 percent to $38 billion. JPMorgan did not fare any better after recording a 46 percent dive in mortgage income to $203 million and a 30 percent decline in originations to $17.2 billion.

What’s going on?

The ongoing trend of falling homes sales is a conundrum that has been puzzling experts considering that it’s been happening against a backdrop of one of the longest economic expansions in history.

The U.S. economy was exceptionally strong in the previous year with better-than-expected GDP growth, low unemployment, wage growth and low delinquency rates among other positive indicators. That sounds like a dream environment for the economically-sensitive real estate sector—only that it’s proving not to be.

Most fingers are currently pointing at the Fed for the unfolding scenario, though the situation is a little bit more nuanced than that.

The Federal Reserve hiked benchmark rates four times in 2018 catapulting 30-year mortgage rates to a seven-year high of 4.94 percent in November. However, the rate pulled back to a more manageable 4.45 percent by year-end. At a casual glance, that increase does not seem far-removed from the average of 3.65 percent about two years ago or even high by historical standards.

The difference in lifetime costs or even monthly payments though is by no means insignificant. For a $250,000 home, the difference in monthly payments and lifetime costs serviced at a rate of 4.45 percent vs. 3.65 percent is $190 and nearly $70,000, respectively.

30-Year Fixed Mortgage Rate--Historical

(Click to enlarge)

Source: MacroTrends

People are renting more

But perhaps a more significant explanation is that U.S. homes have become just too expensive for the average buyer.

Home prices have been ascending for years, with. the median price for existing homes in December clocking in at $253,000, a 2.9-percent increase from the previous year and the 82nd straight month of gains. Related: What Top Financial Analysts Are Saying About Brexit

Saddled with mountains of student debt, millennials in their 20s and 30s simply cannot afford to pay for new homes and are forced to rent for much longer. But it’s not just cash-strapped millennials who are renting—majority of states have seen rents skyrocket over the past few years, a clear indication that this has become a nationwide trend.

It’s not just native U.S. buyers who are balking at high home prices. International buyers led by China, Canada, U.K. and Mexico are purchasing far fewer homes stateside—by as much as 21 percent.

International buyers are a very significant component of the U.S. housing market considering that they tend to buy more high-end properties. For instance, foreign buyers dropped a median of $292,400 on homes in 2017, 17.3 percent higher than the median for homegrown Americans.

Chinese buyers have been snagging the most residential real estate in the U.S. but spent 25 percent less on overseas homes in 2017. It’s feared that the recent move by the Beijing government moves to limit money outflows, including placing a $50,000 limit on individual foreign outflows as part of its capital control, is behind the slowdown.

Why the high mortgage rejections?

Curiously, Fed data shows that the rate of rejections for mortgage and refinancing applications shot up to 19 percent during the second half of the year compared to 15.6 percent previously.

It appears counterintuitive that mortgage lenders faced with severe headwinds in their core business should turn down the little applications that come their way. But according to Two Moody’s insider, appearances can be deceptive. According to the analysts, home-lending standards have actually been loosening lately compared to a few years back. The ongoing squeeze in home originations have been forcing lenders to consider more applications from credit-challenged applicants hence the higher rate of rejections.

On a brighter note, this means that individuals with good credit scores who apply for a mortgage under the current environment stand a better chance at winning approval. There won’t be many takers though at these levels, as the charts below demonstrate. According to the UBS, the number of people who think it’s a favorable time to purchase a home has fallen below that of people who believe it’s a good time to sell a loan—a foreboding signal, and only the second time it has happened in the 26 years the bank has conducted the survey.

(Click to enlarge)

Source: Business Insider

By Alex Kimani for Safehaven.com

More Top Reads From Safehaven.com

since home sales are declining it also becomes a substantial financial risk should you need to sell because of job loss or relocation for a new position..

buying a home today is equivalent to putting a noose around your neck and playing in a tree.