The three major currencies of central Europe have appreciated strongly against the euro so far this year, boosted to varying degrees by rising interest rates, strong economic growth, and positive investor sentiment - the latter buoyed by the final confirmation that Slovakia will adopt the euro next January. However, there are some preliminary signs that the region's strong growth rates are about to slow. Interest rates may be at their peak in Poland and Hungary, and a rate cut may be in the cards in the Czech Republic. All of which suggests that the Polish zloty, Czech koruna, and Hungarian forint may also have peaked for now.

With Euro-zone membership coming up next January, Slovakia's central bank is focused on keeping its policy rate level with the ECB's refi rate. As a result, the bank yesterday left its two-week repo rate unchanged at 4.25% and will follow any subsequent ECB moves in the run-up to January 1. In the Big Three, however, the picture is more complicated. All three have been hit by a surge in inflation thanks to rocketing food and fuel prices. June's (EU-harmonized) annual rate came in at 6.7% in Hungary and in the Czech Republic, and at 4.6% in Poland. Currency appreciation has helped to restrain import price pressures somewhat in all three countries, but the Hungarian and Polish central banks remain biased toward tightening. However, the Czech central bank has shifted to a more dovish stance, and may even lower its policy rate next week.

Chart 1

Having hiked by a total of 100bps since the start of the year, Poland's central bank today left its main interest rate on hold at 6.0% for the second consecutive month. Polish growth remains robust (with the finance ministry's latest forecast of real GDP growth at 5.5% this year) and while inflation is not as high as in Hungary or the Czech Republic, there are concerns that the zloty is masking the strength of domestic inflationary pressures. Today's statement from the Monetary Policy Council specifically noted that the bank stands ready to hike rates further if needed to bring inflation back to the 2.5% target.

Chart 2

Hungary's central bank has also hiked by a total of 100bps so far this year, but last week left its base rate at 8.5% for the second consecutive month, citing the anti-inflationary impact of the strong forint. However, the bank also said that it would hike again if needed to meet its 3.0% inflation target. Growth is weakest in Hungary, with the government forecasting just 2.4% real GDP growth this year, but sentiment has been boosted by the Slovak effect, by the announcement of a major auto sector investment project, and by an improvement in the fiscal accounts. (This year's budget deficit is now expected to come in around 3.6% of GDP, down from 5.5% last year and 9.2% in 2006.) Hungarian exports also seem to be holding their own. Still, grumbles about forint strength may get louder, particularly if Czech rates start to come down.

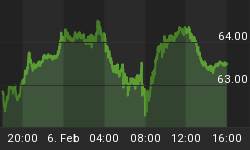

Chart 3

In contrast with the neighbors, the Czech Republic's central bank has raised rates only once this year - 25bps back in February - and its benchmark two-week repo rate of 3.75% remains below that of the ECB. Still, the perception of the koruna as a regional safe haven has made it among the world's best performing currencies against the euro and the dollar this year. However, signs of an economic slowdown are clearest in the Czech Republic, where exports have started to stagnate and the finance ministry has trimmed its GDP growth forecast for this year to 4.6% (vs. 6.6% in 2007). PM Topolanek has argued that the koruna's appreciation has outpaced productivity growth and so threatens the economy. Last week central bank Governor Tuma stated that the bank would stop discussing rate hikes and focus on whether to hold or cut at the August 7 meeting. He raised the concern that the currency's strength could push inflation below next year's target of 3.0%. Another member said today that the board may discuss a 50bps rate cut next week.

The Czech koruna has slipped about 4.5% over the past week as the markets have been convinced that a shift in strategy is imminent. Although July's inflation data (which will be released August 8 but doubtless made available to the August 7 board meeting) may seem to preclude a cut, the central bank is focused on the outlook for 2009. Assuming the bank's August inflation outlook shows the headline rate dropping next year, Czech interest rates likely are headed downward. However, it is unlikely that the Polish and Hungarian central banks will be in a rush to follow suit.