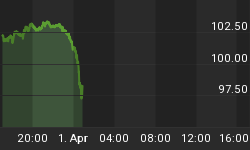

Other pundits have already observed it, I am sure, but the equity market these days is trading as if it is tuned into a news feed that is either six months behind, or six months ahead. I sure wish I knew which it was, but the point is that stock prices are trading up or down with complete disinterest in what related markets are doing or - heaven forbid - what the political economy is doing. The S&P ripped above 1200 today before fading into the close. The data was lackluster: Retail Sales was slightly soft, and there was nothing interesting (if there ever is) about PPI.

On the news front, the ECB announced that it had a $575mm take-up in their regular 7-day dollar liquidity-providing operation, at a rate of 1.1%. As the story linked to above notes, it is the first time banks have taken an allotment from this auction since August 17th, and two banks did so this time. In what is I am sure a coincidence - and I really mean that this time - Moody's cut the ratings of SocGen and Credit Agricole, two French banks, while leaving BNP untouched (but still on review).

Meanwhile, the brilliant Treasury Secretary Tim Geithner described the current situation as "an economy at this early stage of the crisis given the shocks we face." While we all know that he meant that in a good way, trying to generate a groundswell of support for the latest "really, this time it will work" jobs package,[1] it's still an amazingly undiplomatic thing for a Treasury Secretary to say three full years after the crisis began and without ever having experienced the "Recovery Summer" we have been promised repeatedly. Let's face it, folks: if even Tim Geithner knows we are in a crisis, and if he is so sure we already know it that he considers it an okay thing to say, then we really might be in for some turbulence.

And the stock market powered blithely upward. The low-to-high range on the S&P was 40 points, or about 3.4%, but far more of that on the upside and with very little volatility. We went down in the morning when a headline hit that exaggerated the vote the Austrian parliament took with respect to the EFSF (the parliament declined to fast-track approval, but initial headlines said they rejected the EFSF), then when the headline was corrected it was a slow, low-volume, but inexorable trade higher.

That sort of behavior makes me wonder about quant funds or 140-40 strategies that care much less about market direction than about inter-security relative value. Commodities drooped a little, bonds were roughly unchanged, and TIPS fell slightly (the Treasury will announce the size of the July-21 reopening tomorrow, and the yield is now up to a hearty 0.07%!). But equities bounded ahead 1.4%. Equity investors are clearly listening to another news wire than the one that the other markets are listening to. I just wish I knew if they were prescient, or nostalgic.

.

In contrast to the rest of this week, Thursday is full of data. Empire Manufacturing (Consensus: -4.0 vs -7.72 last) is only a marginal surprise from setting a new 2-year low (below -10.44). Initial Claims (Consensus: 411k vs 414k last) is befuddling both economy bulls and bears by simply going sideways; for the year, the average Claims has been 415k and we are right in the middle of the year's range as well. Something below 400k or above 420k is needed to get a reaction. Later in the morning we'll see August's Industrial Production and Capacity Utilization (Consensus: 0.0%/77.5%) figures and the September Philadelphia Fed Index (Consensus: -15.0). Remember that Philly Fed last month plunged to -30.7, which was a big shock and one of the wake-up calls that growth had slowed abruptly in August. It will be closely watched and another figure in the mid -20s will be construed negatively (at least, in the fixed-income markets where they may notice).

I've left CPI for last, although it is unlikely to be a market mover. The consensus call is for +0.2% on headline inflation (keeping it steady at 3.6% year-on-year) and +0.2% on core inflation (raising core to +1.9% y/y). Core inflation on a year-on-year basis should rise even if we get a 'soft' 0.2% (meaning, it is rounded up rather than down) because of base effects, and should exceed 2.0% through the end of the year for the same reasons. Indeed, if we continue to get relatively innocuous 0.2% prints then core inflation will still be around 2.5% by the end of the year.

Although people tend to think that I have a vested interest in projecting higher inflation, I always point out that from 2003 until 2010 I argued that core inflation would be pressured lower. And in the current circumstance, I have to confess that the current level of core inflation is running ahead of where my company's models suggest it should be. That is, our projections for core inflation in 2011 were significantly too low, rather than too high. I had seen full-year core for 2011 around 1.6%-1.7%, and we are going to go bounding over that figure handily.

The fact that inflation is appreciably above where my model projected it could indicate there is downside risk to the numbers going forward, but what it is more likely to mean is that the models were calibrated on a different sort of environment than the one we are now experiencing. Of course, that's absolutely true - we've never experienced this sort of environment, so it isn't in the historical data - and a good analyst here doesn't lean too heavily on calibrated models. There is some art involved in the forecast...or at least, a heavy dose of caution.

An important observation can be made regardless of the exact forecast going forward: if the Fed is going to do QE3 (which in fair disclosure I thought they wouldn't do until I listened to the speeches following the last FOMC meeting, and read the minutes), they will prefer to do it sooner rather than later since it is easier to be dovish in the face of 1.9% core inflation than in the face of 2.5% core inflation. The economists at the Fed aren't spectacular, but they can project as well as I can where core inflation will be if 0.2% numbers keep printing. It is no mystery to the FOMC that they are going to have backward-looking inflation up over their target quite soon. And in this case, they are clearly going to be leaning on nostalgia when they make the call next Wednesday on whether to do QE3.

So maybe, maybe, equity investors are being prescient about the Fed's nostalgia?

[1] Since Krugman keeps saying, no matter how much is spent on jobs packages and green jobs and alien invasions, that the amount of stimulus is far too little, (see for example here, although the estimate of the post-Depression stimulus is absurd as pointed out here) I think we ought to discuss all such packages in Krugman units. So if we really need $30 trillion in stimulus, then let's call that one Krugman. $3 trillion can be a mini-Krugman. And $300bln can be a micro-Krugman. So the latest jobs package is about 1.5 micro-Krugmans. Hardly seems worth it.