I'm not really sure what to make of the market action the last couple of days. I know Q1 earnings have looked good, but in a number of cases that was related to the very mild Q1 weather. Investors are being very credulous of the view that this represents real, lasting improvement and not a pull forward from Q2. (Remember, I'm not one who thinks the economy is on the verge of collapse, but I also don't think it's on the verge of exploding in a positive way either.)

The Fed was equally credulous yesterday. While there was no surprise in the Fed's lack of action on Wednesday, nor any surprise that the statement was roughly unchanged, there was aggressive improvement in the Fed's projections for 2012 since January's estimates. In January, the central tendency of the FOMC's individual projections for the Unemployment Rate this year was 8.2%-8.5%. In April, that became 7.8%-8.0%. That's an aggressive improvement to a 9-month forecast in only three months. The Fed has proven repeatedly that they are no better at forecasting than Punxatawney Phil, so the forecasts don't mean a lot - but what it should tell you is that they don't seem to have much of a clue, if three months of data can change your 9-month forward Unemployment forecast by half a percent.

Their forecast for 2012 PCE inflation was 1.4%-1.8% in January; It's now 1.9%-2.0%. Combining those alterations, if the Fed had any credibility, would mean sharply higher interest rates, because it shows the Fed thinks growth is faster and inflation is higher than they previously thought it was. In fact, if the Fed was perfectly credible, you'd believe them when they said that short rates will be held down until 2014, and you'd believe that the implication of their forecasts would be a rapid series of hikes thereafter. Ergo, the yield curve should be higher and more flexed: steeper from 2y-5y or 2y-7y and flatter from 5y-30y or 7y-30y. And yet, the 5y yield is down to the lowest level since February and 5y-30y is steeper than it was back then.

The market is basically ignoring the Fed, despite the fact that Bernanke said in the Q&A that it's the Fed's view "that it is reckless to accept higher inflation in exchange for possibly greater employment." Of course he must say that, so it doesn't have much content, but it's still remarkable that the bond market is just brushing off the Fed altogether.

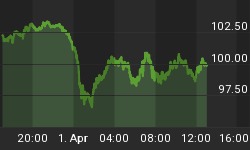

I hope the bond market isn't putting too much stake in the recent worsening of Initial Claims, which surprised on the high side Thursday for the fifth consecutive week (in fact, if you consider the original survey compared to where Claims ended up after revisions, the consensus estimate has been too low in every seek since Feb 17th!). The chart below (Source: Bloomberg) certainly looks like there has been a sudden worsening in the job market.

But I think that would be a mistaken reading. In my view, the recent numbers are likely just payback from the weather-inspired strength in Q1, and my hypothesis is that the true underlying run rate has merely flattened out at 370k-380k. One reason I am not particularly worried about Claims yet is that the Consumer Confidence "Jobs Hard to Get" figure that I referred to earlier this week (and which is shown below) is ordinarily a better indication of true improvements in the employment situation.

It turns out that if you ask the average "man on the street" how the job market looks, he's likely to have a pretty good feeling for it (in contrast to, on the other hand, asking about inflation - which no one internalizes well) because he has some idea of how many of his friends are looking for work. It's a relatively clean number, unlike Claims.

The bond market might instead be reacting to ever-worsening news from Europe. The latest news today seemed to fly under the radar, but I think is striking. In a report in German paper Sueddeutsche Zeitung (summarized in English here), we learn that the ECB is working with Eurozone countries on a plan that would let banks access European Stability Mechanism (ESM) funds directly. Why is this a big deal?

Well, my first question is: since these banks can already access liquidity directly from their national central banks (and thus indirectly from the ECB)...why would the ECB want to have banks access the ESM directly? The obvious answer is that the ECB likely fears the impact that a default would have on its own solvency (which is to say, it would be devastating to the institution) and if banks borrow from the ESM it means the sovereigns backing the ESM...mainly Germany, France, Italy, and Spain...would be on the hook directly. Can you imagine the Fed saying that U.S. banks should borrow directly from the Treasury rather than from the Fed? What signal do you think that would send?

Yeah, that's what I think too.

Whatever the bond market is looking at - whether it's worsening conditions in Europe, or worsening economic conditions (which I think is a misreading) - it clearly isn't what the stock market is looking at. If bond yields are low because of growth fears, then stocks are clearly ignoring that issue. If bond yields are low because of Europe fears, then stocks are clearly ignoring that issue. And frankly, even if bond yields are wrong because the recent worsening data is merely a give-back from a mild Q1, then stocks are still misinterpreting the recent earnings numbers.

I still own equity puts, although they are mostly worthless. I am still short bonds, long RINF and INFL (that is, long inflation expectations), long commodity indices, and long the dollar against the Yen. While I am not invested this way because I am a growth bull, all of these positions except the equity puts get penalized with a weak turn in the economy. Accordingly, I am inclined to trim the bond short and refresh the equity put position while implied volatility remains cheap. I'm still bearish bonds, but the trade hasn't performed and the worst of the bearish seasonal pattern is past.

On Friday, the advance Q1 GDP number will be released. The consensus estimate is for a 2.5% rate, with a 2.3% rise in Personal Consumption. A stronger number probably implies a weaker Q2 as it would suggest more mild weather pull-forward, but the markets won't see it that way!