I posted earlier today some thoughts that I tweeted right after the CPI figures were released this morning, and added a few ancillary thoughts as well. I figured that may be all that I would write today, since CPI is clearly the most important release of the day and because I am hard at work on our Quarterly Inflation Outlook piece.

But then I saw a number of headlines such as this:

- "Retail Sales Edge Up, Inflation Flat as Energy Prices Fall"

- "Tame Inflation, Strong Factory Data Lift Futures"

...and I realized I had to write today.

It isn't true that core CPI was "as-expected" or that inflation was "flat." Of the 78 economists polled by Bloomberg about the monthly change in core CPI, one called for 0.0%, eight expected +0.1%, and the balance expected +0.2%. The average works out to be 0.184%. This is consistent with poll results on the question of the year-on-year core CPI rate, which saw one economist at +2.1%, nine at +2.2%, and the rest at +2.3%. So economists generally were looking for a "soft" +0.2% print.

What we actually got was +0.242%, the third-highest print since 2008; this caused the year-on-year core rate to be 2.314%, compared to 2.255% last month. That is, last month we barely rounded up to 2.3% and this month we had to round down. This is about as big a miss as you can have, without actually printing a +0.3% and causing everyone to wig out.

(Incidentally, while it's relevant for short-term trading of TIPS and inflation swaps, headline inflation is not a policy target. We focus on core inflation, for policy purposes, when headline is higher than core, and we focus on core inflation when headline is lower than core. Policymaker pronouncements that discuss headline inflation are potential hints that a central banker is looking for an excuse one way or the other. Today's headline inflation is not a good predictor of next year's headline inflation, but today's core inflation is likely to be reasonably close to next year's core inflation.)

Also rising on a year-on-year basis: Rent of Shelter (2.216% vs 2.104%). The bubble is now unwound, rents are rising at near the pace of other prices, and we can no longer look to housing as being a restraining force on core inflation going forward.

Services less energy services rose to 2.449% versus 2.325% (see Chart below, source Bloomberg). This is 57% of the CPI basket. Again, there is nothing to suggest "tame" inflation here. As I wrote back in February, inflation is as "contained" as an arrow from a bow.

The implication of the chart above is interesting. The only reason that core inflation was as low as it was in the years leading up to 2008 was that commodities ex food-and-energy commodities (which category adds up to 19.4% of the CPI) were basically not inflating (see Chart below, source Bloomberg). This is where the "globalization" effect happens, since it's much easier to import goods than services, but some evidence suggests that this effect has largely run its course.

So "Commodities ex-food-and-energy commodities" is rising at 2%. What if "Services less energy services" returns to, say, 3.5%, where it happily existed in the 'Naughts, while commodities inflation stays steady? Core inflation in that case would rise to 3.1%. Moreover, with every central bank in the world printing money (by the way, M2 growth is back to 9.2% year/year) there is no reason to think that the standard of the mid-2000s is where inflation should stop.

In this context, it would be stupid for the Fed to consider further quantitative easing at its next meeting in June. Therefore, I fully expect it!

One-year inflation swaps are around 1.50%. Two-year inflation swaps are at 1.75%. Five-year inflation swaps are at 2.2%. I think these are all very low.

So why are people suddenly so calm about inflation, whereas a couple of months ago everyone was all lathered up?

Partly, it's because people tend to remember the stuff they buy more than they remember the services they buy. Partly, it's because gasoline prices have receded about 20 cents in the last few weeks, so there's a near-term reinforcement of the idea that inflation isn't so bad. Partly, it's because almost every economist and the Fed itself is saying that inflation isn't a threat while global growth is in trouble. And partly, it's because price changes over the last few months have been very regular and much less scattered. Consumers tend to encode volatile prices as rising prices; also, they tend to remember the price changes of the stuff that's gone up better than they remember the price changes of the stuff that's gone down. Over the last few months, both the volatility of monthly inflation rates among the many subindices the BLS calculates, and the dispersion of those rates, have been unusually low. So much so, in fact, that my measure of "inflation angst" is at an all-time low for the period over which I have calculated it (see Chart, source Enduring Investments). The chart shows the amount by which inflation feels higher than it actually is, due to these cognitive effects.

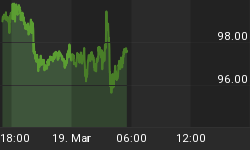

Meanwhile, Europe is getting worse again. Greece decided to pay off a bond that was covered under UK law and which hadn't been subject to PSI - which, as you all remember, was something they swore wouldn't happen. But the country had to scrape together lots of green stamps and supermarket coupons to make the payment, and with the country's politics in disarray it seems the can wasn't kicked as far down the road as everyone thought. Greece has gone from "of course they won't leave the euro," to "it's impossible anyway" to "they're not allowed to" to "see, that was no problem," to "I wonder when they will." And, as expected, the effect is spreading to other periphery countries. Spanish 10-year yields rose to 6.35% today, the highest level since November (see Chart, source Bloomberg).

Stock prices fell today, extending the recent mini-slump. The only reason to own stocks here, and I think the only reason prices are as high as they are, is that you want to own anything but fixed-rate bonds with the 10-year rate at 1.74%! Inflation-indexed bonds (TIPS) are better, but still are more risk than return at this point (10-year TIPS yield is -0.41%). So the argument for stocks as "anything but bonds" is a reasonable one. But it's an even more powerful argument in favor of owning stuff that people actually consume, and yet commodities have been dripping steadily all month. The combination of low recent returns to commodity indices and continued robust money growth has our expected return models projecting 10-year real returns of 5.4% for commodity indices, compared to 2.3% for the S&P, with similar risk.

We are confident in our valuation models. But no, that doesn't stop it from hurting right now!