Over the weekend, the Spanish crisis was semi-resolved with the EU agreeing in principle to give money from the ESM (which isn't operational yet) or the EFSF to the FROB (the Spanish banking entity). The €100bln will likely be senior to other Spanish government obligations, although this is not clear.

In fact, there is a fair amount that isn't clear. Equities shot higher by 20 S&P points overnight, only to fall back to +7 before the NY open and finishing the day down 16.7 points, -1.3% on the day.

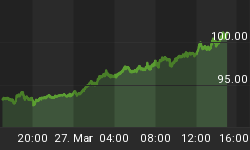

Stocks may have been taking a cue from Spanish and Italian bonds, which were smashed today. Spanish 10-year yields rose 30bps (see Chart, Source: Bloomberg) while Italian 10y BTP yields rose 12bps.

It may seem like the market is lodging a no-confidence vote, but I am not so sure that's indeed what is happening. Yes, in general it has been a good trade over the last couple of years to bet that the grand plans will come to nothing, and quickly, but this is still the most decision-like announcement that we have yet seen come out of one of these weekend meetings. Yes, this only helps the Spanish banks, and Spain is likely to still need money while the ESM/EFSF now has €100bln less in capacity. But depending on the details, this isn't a horrible attempt to address a very specific problem. The question, of course, is whether this is a specific problem, or a general one! (Pete Tchir had a great line; he said "Fixing Spanish banks is a bit like drowning one lawyer - a good start.")

But the rise in Spanish government bond yields doesn't necessarily mean investors view the announced measures as a failure. Rather, it might indicate that investors view the announced measures as a success and likely to happen - since once element of that program would be (probably) the subordination of the claims of Spanish government debt holders. It is entirely rational to mark yields higher when debt goes from a senior position in the capital structure to a junior position in the capital structure. The question is, what does it do next? That will be the real indication that the announcement quelled some of the fear that had developed...or did not.

Let's not forget that Greece goes to the polls next weekend, so even if you thought the result of this weekend's meeting was terrific, we still might be sitting here in a week staring down a Euro exit or breakup.

.

Book Review: Finance and the Good Society

Today's is a short article, so I thought I would take a few paragraphs to review briefly a book I just finished reading: Bob Shiller's Finance and the Good Society.

I took up this book expecting, frankly, that it would be far too left for my personal tastes. I have great respect for Dr. Shiller, and like many other people I thoroughly enjoyed Irrational Exuberance. I was less impressed by Animal Spirits: How Human Psychology Drives the Economy, and Why It Matters for Global Capitalism, which he co-wrote with George Akerloff, but still judged that to be a book worth reading. In general, while I enjoy the application of behavioral economics insights to real world problems, I feel that Dr. Shiller sometimes goes a bit off the rails with redistributionist rhetoric.

The reason that redistribution schemes don't tend to work well in real economics can be illustrated with a simple, familiar example. Suppose that in a poker game, whenever a player won a pot he collected only a fraction of the pot; specifically, the larger his stack of chips already is, the smaller a share of the pot he gets and the more is distributed to the shorter stacks. Obviously, such a scheme is redistributionist, but if the measure of "good" is taken to be the Gini coefficient or some other objective measure of the evenness of the wealth distribution then this may seem to be a positive improvement to the normal way of winner-take-all from each pot. But advocates of this sort of policy tend to overlook what will happen to the game: if you are sitting on a big stack, you will tend to avoid playing most hands, since your benefit from victory is less the larger the stack you start with.[1] The economic equivalent is that in heavily-taxed societies, the wealthy do not provide as much capital to the system - and so it isn't a priori clear if more-progressive tax rates will create a more-balanced distribution of wealth. Unless you force them to ante, via a wealth tax...but let's not go there.

Anyhow, I'm drifting off-topic: Finance and the Good Society pleasantly surprised me. What is great about the book, and surprising I suppose, is that Dr. Shiller spends a great deal of time explaining why the practice of modern finance is mostly good. In Part I, he devotes one (short) chapter each to CEOs, Investment Managers, Bankers, Investment Bankers, Mortgage Lenders and Securitizers, Traders and Market Makers, Insurers, Market Designers and Financial Engineers, Derivatives Providers, Lawyers and Financial Advisers, Lobbyists, Regulators, Accountants and Auditors, Educators, Public Goods Financiers, Policy Makers in Charge of Stabilizing the Economy, Trustees and Nonprofit Managers, and Philanthropists. In each chapter, he explains why this particular role is necessary. Honestly, it's worth the price of the book just to read an outstanding explanation of why Derivatives Providers, Financial Engineers, and Mortgage Securitizers aren't inherently evil.

In Part II, Shiller dwells on the problems of modern finance. These we know all too well due to the events of the last five years: problems like "An Impulse for Risk Taking," "Debt and Leverage," and "Some Unfortunate Incentives to Sleaziness Inherent in Finance" among others. But unlike in his book Animal Spirits, he does detail some policy prescriptions (including how certain institutions could be redesigned to have the proper incentives). I must be very clear that I don't agree with all of his policy prescriptions, but I tended to agree with his assessment of the problems.

All in all, this is an even-handed book that makes a distinction that has been rarely made in the post-crisis witch-hunt: hate the sin, love the sinner. The people involved in finance are, in general, good people and the structures, in general, work well most of the time. Improvements can be made, and when the serial crises are over in a few years, hopefully we can discourse intelligently on these improvements. Dr. Shiller has made a good contribution to that discourse with this book.

[1] In fact, if the proportion of the pot that you get to keep if you win is p, and the expected amount that you have to invest in the pot to win, as a share of the total pot, is y, then you will only play in a hand if your expected probability of winning the hand is at least y/p. Therefore, you will only play if you can win very large amounts of money relative to the amounts you bet, or if the odds of your winning are high. In normal poker where p=1, you will bet if your "pot odds" are better than your chance of winning. But in "taxed-winnings" poker, you need much better pot odds relative to the chances of winning.