After a huge rally like we had on Friday, it's often prudent to wait for at least one trading day to see whether the move will be instantly repudiated, or whether the repudiation will take place over time.

Here's how I see the results of the Euro summit. A bunch of heads of state agreed to a package that increases by a little bit the total amount of capital committed (not the €120bln of the headlines, as the headlines included some programs already planned), makes some concessions to help Spain, and makes some important improvements in the way money is to be dispensed and the seniority of the claims of the EU authorities in such a case. Nothing has been approved by any legislatures, and nothing is to go into effect very soon.

It's a useful step, but merely a step; the perception of success was enhanced by the convenient fact that the conditions of quarter-end raise the costs of incredulity. Better to go along, for at least the last day, and keep from ruining a quarter of good trading! That's why a modest step forward was worth 20 S&P points, as well as 40-50bp rallies in the 10-year bonds of Italy and Spain, which in turn produced a palpable sense that this time, the Eurocrats sounded the right note.

It was better, to be sure. Subordinating the bailout money to the claims of holders of sovereign debt was critical, since otherwise yields would have gone to the moon in very short order. Make no mistake, if push comes to shove the authorities will still do a cram-down, but at least they seem to understand why they don't want to make it obvious now.

I always find amusing how important "narrative" is to the markets. Investors cling to a popular narrative point even when it makes little sense. I heard on Friday that Merkel "conceded when surrounded by foreign leaders." Really? What in Merkel's history or makeup would make you expect that she would cave in to foreign leaders, especially just one day after she had been so hostile to Eurobonds? Isn't it much more likely that she doesn't see the new deal as being a big deal, since it doesn't involve much new money?

But the market jumps were so powerful psychically that moves were mostly sustained today even though the predictable chinks appeared in the story. Crude oil jumped 9.4% on Friday, as well as copper, coffee, gold, and other commodities as the dollar dropped sharply. They sustained most of those gains today as the DJ-UBS closed +0.2%, even though the buck rallied some. It makes sense, if commodities have been beaten down so badly on the disaster scenario, that any whiff that the scenario might not come to pass should send them skyrocketing. Not that I think that commodities really need global growth to accelerate in order to do just fine, but the asset class is out-of-favor, widely scorned, and under-owned for the first time in several years so it shouldn't take much to provoke a rally.

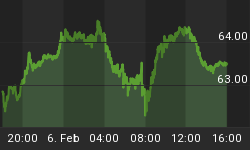

Equities, up sharply on Friday, added another +0.25% today (on the S&P), again extending the prior gains as the narrative continues to beat. Bonds, on the other hand, reversed their Friday selloff to rally today, almost wiping out Friday's loss. It seemed the bond guys were the only ones to notice that the Manufacturing ISM printed its lowest level (and first sub-50) since 2009 (see Chart, source Bloomberg).

The last couple of months have seen a rather sharp fall. There are more important data this week than ISM - Employment on Friday, for example - but this is somewhat disturbing, especially after the Milwaukee and Chicago purchasing managers' reports late last week both exceeded expectations slightly. The 2-month change in the ISM is actually the worst 2-month fall since December 2008, worse even than the post-Japanese-earthquake setback. So it's not just the level, and not just the direction, but the rate of acceleration that's disturbing. Again, though, it's just one piece of a data collage.

As for those predictable chinks, how about this one: Finland declared that it, along probably with the Netherlands, will prevent the ESM from buying sovereign bonds in secondary markets. Well, whoops! The decision to use the new entities to stabilize markets was kinda sorta one important development to come out of the summit. And, while technically the summit wasn't about Greece, it can hardly be productive that, hard on the heels of a new Greek government being installed (and one elected on a platform of renegotiating the austerity measures so as to remain in the EZ), the ECB told Greece not to hope for any concessions or aid such as Spain has received.

I suspect that we are going to see, shortly, yet another re-think about the prospects for Europe. But while it's easy for me to see that I am still not excited by the prospects for equities, it is harder for me to see where bonds are likely to go, near-term. The knee-jerk reaction, conditioned over decades, to every piece of bad economic data is to buy Treasuries. But at 1.59% for the 10-year note, we are clearly not just pricing in weak economic data. With core inflation at 2.3%, and 10-year inflation expectations at 2.40%, we are clearly not pricing in deflation or disinflation. I can't think of any reason to buy bonds here, and even if I was running an LDI program that needed to be 100% in fixed-rate bonds to be immunized, I'd buy inflation-linked bonds as a surrogate that has pretty much only upside (relative to nominal Treasuries!) from here. But that reasoning was the same at a 2% 10-year note, so the glass remains dark to me. I will say that our "Fisher decomposition" model (which sounds a little bit like a mortician's dissertation, come to think of it) is indifferent on being short the bond market through being long inflation or being short the bond market through being short TIPS - it is simply short nominal rates, but importantly at a leverage ratio below 1.0. I suppose that matches my view: bearish on bonds, bullish on inflation breakevens (e.g. through RINF or INFL, neither of which I currently own), but very cautiously in all cases.