6/8/2014 6:37:52 PM

Market Summary

The performance graph below shows for the first time this year all the major equity indexes are in the green year-to-date at the same time. Stocks and bonds are floating at historically high levels. The equity market has kept moving higher despite mixed signals about the growth potential of the U.S. economy. The next watermark of stocks is 2,000 for the S&P500 index, which is just 2.5% above its current price.

As you can see in the updated performance graph below, May's full-month performance this year was well above midterm-year and all-year averages since 1950. In contrast to the previous two months, technology and finance sectors led the advance with small caps coming on strong. NASDAQ and Russell 2000 strength in May reverses some of the worrisome divergence between large-cap and small-cap indices commonly seen during the latter stages of bull markets. May's strength was broad based as 26 of 29 S&P sectors posted gains.

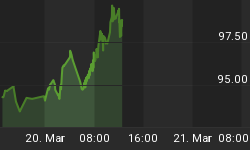

Your June 1st Weekly Setup articles mentioned "After dragging stocks down in March and early April, the technology sector is now leading the market higher." As evidenced in the chart below, the Russell 2000 index had its best week of the year as the DJIA and S&P500 index again closed out the week at all-time highs with the S&P index marking six record closes in the past seven trading sessions. The so called midterm election year cure is not yet in play this year. One disconcerting item of note is trading volume is running 20% below average, this suggest it wouldn't take much to knock stocks of their lofty perch. The ultralow volatility and weak volumes does have some investors worried that this current tranquility is more like calm before the storm.

Your Weekly Update recent discussed "Bond prices generally move opposite of yields as strong demand from foreign and domestic buyers is keeping bonds near their highs for the year. The current low rates are believed to signal economic weakness with low inflation." In the updated chart below you can see treasury bonds have pulled back in response to an uptick in interest rates. Gold appears to be bouncing off a support level that has held up the price all year.

Market Outlook

The Stock Trader's Almanac commented "Solid across-the-board gains in May and new all-time highs by DJIA and S&P 500 improves the odds that the worst two-consecutive quarters of the four-year presidential election cycle could be better than average. Markets have broken free of the typical midterm year pattern since 1950 and now appear to be tracking the Sixth Year of Presidential terms more closely. Should DJIA and S&P 500 follow the Sixth Year of Presidential terms pattern, further gains are likely this quarter and significant weakness will be held at bay until sometime during August and September. However the tapering of Fed liquidity and concerns about when interest rates will rise could still easily derail the market."

Your June 1st Weekly Update mentioned "price breakout as the MTUM has catapulted above resistance and technical strength and momentum indicators signal a bullish trend. The 'bulls' are firmly in control as the bears are hibernating." The current trend favors a continued slow and methodical move upward as the S&P 500 index has not made a 1% move in a single session in almost two months. The market continuing to rise in a low volatility environment has a positive impact on investor sentiment. If the technology and small cap sectors continue leading the market higher along with financials, this is considered a very strong sign bullish momentum will continue.

The CBOE Volatility index (VIX) sank to the lowest level since 2007. As you can easy observe in the graph below, the VIX, which tends to rise when volatility increases or the market drops, has been on the decline for months and is well below its historical average of 20, which some view as a sign that investors are ignoring global economic concerns that could derail the rally. Some Federal Reserve members have expressed concern about investors ignoring potential risks, but one advantage of the low VIX level is the cost of downside protection via the options market is extremely cheap and continuing to fall.

Last week we said "right on queue the major indexes reached all-time highs and the updated survey results below show retail investors jumping on board with increased bullishness. Expect the overall stock market to fluctuate between the current highs as resistance and moderate moves lower on lighter than normal volume as the markets settles into summer doldrums." You can see in the updated American Associate of Individual Investor (AAII) survey results below how retail investors have jumped on board with the major equity indexes at all-time highs. The bullish percentage has climbed to its long term average primarily at the expense of bearish sentiment,which has gotten extremely low. Analysts who regard the AAII survey as a contrarian indicator can make the case that the low bearish reading coupled with the excessively high neutral percentage hint stocks are due for a pull back. The most probable expectation is a price pause in the current bullish move as the major equity indexes absorb overbought conditions.

Previous analysis of National Association of Active Investment Managers (NAAIM) exposure index said "if stocks keep moving higher investors might scramble to get back in, sending prices even higher." The current reading of the NAAIM survey has catapulted up to 90.86% from 70.94% the previous week. Professional money managers have gotten on board with the current bullish trend as their latest index is higher than last quarter's NAAIM 84.40% average reading. Another factor contributing to money managers' putting more funds to work is the need to rebalance their portfolios for the second quarter window dressing due at the end of the month.

Trading Strategy

Last week's Market Update article said "We live in an environment of no place to go but stocks and big money knows it.June is the end of the Best Eight Months of the Year for NASDAQ and the Russell 2000 small cap index... sell any underperforming open long positions and further tighten stops on winners...Nasdaq's 'best eight months' which ends in June. June ranks near the bottom on the Dow Jones Industrials just above September since 1950 . S&P 500 performs similarly poorly.Small caps also tend to fare well in June."

As discussed above, both the DOW and S&P5 500 closed the week at record highs with financials, small caps and technology shares leading the market higher the past month. Look at the updated chart below as we said recently "the small cap Russell 2000 found a support level where the price is bouncing off of and there wasn't a "bull trap" smaller cap stocks typically lay dormant during the summer and awaken in the fall. However, when earning season begins in a month or so you may be able to get some quick gains from making bets on smaller cap stock that are on your watch list." A price pull back is probably a good opportunity to bid on small cap stocks that you like.

As discussed above, gold prices appear to have bottomed out at a support line that has been in place since the beginning of the year. Now is probably an opportune time to look at setting up trades that will profit if gold does bounce off its support level.

As we have discussed recently, "In the current environment, it is prudent to maintain tight stops with proper position sizing for long trades (whether bullish or bearish). As we have demonstrated in our trading newsletters, spread trading works well in this market as the trades are less expensive and positions are protected if the trade goes against you.

Regards,