7/6/2014 9:31:48 AM

Market Summary

The Dow Jones Industrial Average moved past 17,000 and the benchmark S&P 500 index rose to within 1% of 2,000 during the holiday shortened week. As displayed in the chart below, compared to the other major equity indexes, superior performance by the Nasdaq100 and S&P 500 is predominately due to higher exposure to technology shares that have surged since mid-April.

Last week the Weekly Update pointed out "The updated graph records quarter-to-date sector performance. We talked about how energy and utility stocks have outperformed the market recently, but you can see these sectors have been on a tear for most of the past three months." The chart below displays the final results for the second-quarter.

Market Outlook

As we said recently "According to the Stock Traders' Almanac, in the mid-1980s the market began to evolve into a tech-driven market and control in summer shifted to the outlook for second quarter earnings of technology companies. NASDAQ's mid-year rally from the end of June through mid-July is strongest. July is best month of the third quarter for the Dow and S&P. Since the bursting of the tech bubble in 2000, NASDAQ's mid-year rally has a spotty track record with seven appearances in the past twelve years. However, it has been solid for four years straight including a whopping 7.5% advance last year.commodities such as energy and gold are the best performers for the month of June. And as mentioned above, Russell Investments reconstituted its indexes, plus investors' willingness to accept risk contributed to the Russell 2000 outperformance compared to the other equity indexes." Below is the final June sector performance.

The updated Momentum Factor ETF MTUM Heikin-Ashi chart continues to signal the overbought condition needs to be resolved, but stocks continue to churn higher. Though the chart has been showing candlestick bearish reversal signs, this may be a case of regardless of what the chart says; ultimately you can't fight the Fed. Fed Chairwoman Janet Yellen said she is not concerned about asset bubbles. Investors interpreted this to mean the Fed will continue to provide liquidity if it believes that is what is necessary to stimulate the economy.

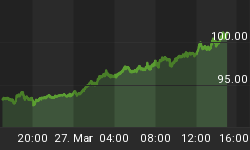

As we have been saying recently "CBOE Volatility index (VIX) closed at its lowest in more than seven years." And other comments related to the updated chart below discussed how as equities rise to stratospheric heights, the VIX is churning lower and lower.

As we recently said "Investors Intelligence Advisors Sentiment survey has reported over 60% bulls for four straight weeks after reaching a multi-year high two weeks ago. Similar lofty readings were recorded in August 1987, December 2004, October 2007 and at the end of 2013. Further excessive bullishness is seen in Weekly CBOE Put/Call Ratio declining to 0.47 last week, the lowest since January 2011.The updated American Association of Individual Investor (AAII) survey below shows bullish sentiment close to the historical average. Neutral sentiment is a lot higher than normal and the bearish reading is well below average, from a contrarian perspective this suggest any surprise will be to the downside." In the bulls favor, bullish sentiment is relatively subdued considering the lofty price levels. This probably means any price pullback will be minor as investors will view that as a buying opportunity.

Previous analysis of National Association of Active Investment Managers (NAAIM) exposure index said "Professional money managers have gotten on board with the current bullish trend as their latest index is higher than last quarter's NAAIM 84.40% average reading. Another factor contributing to money managers' putting more funds to work is the need to rebalance their portfolios for the second quarter window dressing due at the end of the month..." The result end-of-quarter rebalancing act is money managers' 85.48% equity exposure going into the third-quarter.

Trading Strategy

Gold and other dollar sensitive commodities have been taking a hit recently as the dollar has strengthened against other currencies. Looking at the chart below you can easily see how gold was at recent highs with the dollar at its lows. As the dollar started to recover gold prices crashed, now the dollar is pressing against its resistance level. If the dollar does break through resistance and moves higher, that is considered a strong negative for gold and other commodities.

Last week we said "Treasury note yields fell to multi-week lows catapulting bond prices higher." Last week treasury yields reversed course and jumped to a two-month high which led to a Treasury bond price crash. You can see in the updated chart below how treasury bonds and gold moved down in tandem last week. Investors moved funds into the equity market from other asset classes. This helps explain why treasury bonds and gold prices moved in synch last week when they recently have been hedging each other by moving in opposite directions. As mentioned above, a pullback in equity prices should be considered an opportunity to bid on stocks you have been eying that have been a little pricey.