The Dow industrials and major European equity indexes posted their biggest weekly losses in three years, with benchmark S&P 500's seven-week streak of gains. As confirmed in the updated chart below, Commodities prices have dominated all year. Gold started the year with a bang but started capitulating in August. Treasury Bonds started the year in a bullish trend that never really abated and is even exploding higher as the year-ends.

Last week we noted "...the S&P 500 BPI has reached an extremely overbought level, which is why the index has been consolidating the past few weeks. Also noted momentum is trying to turn bearish..." In the updated chart below we note the Bullish Index confirmed last week's technical signals by starting a downtrend as bearish momentum continued.

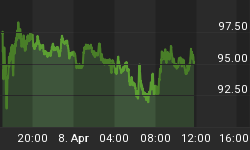

The inverse relationship between the dollar and commodity played out last week as the dollar pulled back from multiyear highs and you can see in the chart below how treasury bonds exploded, plus even gold jumped to its highest price since October.

Market Outlook

The Stock Trader's Almanac talks about how in recent years, the market has been prone to early-December weakness. Thus far, 2014 has followed December's typical seasonal pattern rather closely. On average the DJIA, S&P 500 and NASDAQ tend to drift lower until reaching their respective December lows sometime mid-month, usually around the eleventh trading day. NASDAQ tends to bottom last, around the thirteenth trading day. From that point on they briskly rally into yearend. Trading this month has followed this pattern closely, although the decline has been larger.

The sharp slide in the stock market this week also has the major averages nearing technical support. DJIA and S&P 500 are touching their respective 50-day moving averages right around the level of the September highs. The 50-day MA is often a support level. Since October 2012 S&P has broken below its 50-day 10 times and only twice has fallen to the 200-day and then through that in October 2012 and this year in October 2014. Based upon December's typical seasonal pattern, look for the market to bottom next week, possibly Monday, followed by a strong up day and then a nice rally to wrap up the year.

As the fourth quarter winds down, the chart below confirms that Real Estate and Treasury Bonds are the best performing asset classes in the quarter as they are reaping the benefits of continued extremely low interest rates.

Last week we mentioned "...Until there is a confirmed break below the uptrend line we expect to see stock prices continuing to climb higher for the rest of the year..." In the updated Momentum Factor ETF (MTUM) chart below we highlight the break below the recent uptrend line into a downtrend which is confirmed by bearish momentum. Stock prices need to recover during option expiration next week to get back the momentum for finishing the year strong.

Last week we stated "...The VIX can be expected to bounce from the current low point, but unless the stock market pulls back significantly any upward move in the VIX will be limited through year-end..." As evidenced in the updated CBOE Volatility Index (VIX) chart below, we got the bounce we expected as stocks broke their streak of consecutive weekly gains. In the chart you can see the intersection between the VIX and S&P, but what happens during triple-witching next week will say a lot about if or when the market returns to recent highs. Volatility usually increases during option expiration week and if this behavior continues next week the Volatility Index could easily reach its mid-October level when the stock market crashed.

The current American Association of Individual Investor Survey (AAII) survey result is not at the bullish extreme. But it was overly optimistic enough to live up to its contrarian reputation as retail investors got more bullish last week and the stock market plunged. Historically, the second week in December is a down week for the stocks and the best bet is still moderate price movement over the next week or so with prices spurting higher into year-end.

Third-quarter National Association of Active Investment Managers (NAAIM) exposure index averaged 71.09. Last week the NAAIM exposure index was 86.06%, and the current week's exposure is 89.01%. The current exposure is at the highest level since this past spring as investment managers sell-off losing stocks for year-end tax purposes and buy into high performing shares to put on the books for year-end window dressing. Current exposure still is not as high as this time last year and if investment managers decide to get fully invested this will send the market soaring at year-end.

Trading Strategy

Next week is critical for determining market momentum heading into the end of the year and kicking off 2015. Prior to this past week, the major indexes had not suffered a weekly loss in almost two months. Next week is the final expiration week of the year for regular options and is a triple-witching week when contracts for stock index futures, stock index options and stock options all expire on Friday. The markets usually experience elevated volatility during triple-witching week and if this follows last week volatility surge the probability for stocks to end the year higher is lessened. If stock prices do fall, that should be considered a good opportunity to bid on shares in the strongest sectors like Cyclicals, Healthcare, and Utilities.

Regards,