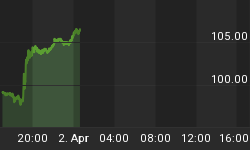

Major indexes closed out their second straight weekly gain, continuing an advance that has lifted the S&P 5.9 percent in seven sessions. For the week, the Dow rose 1.4 percent, the S&P rose 0.9 percent and the Nasdaq rose 0.9 percent. It was the ninth positive week in the past ten for the Dow and S&P. The benchmark index hit its 52nd record close of the year on Friday, the most since 1995 and the fourth-best annual record ever, while the Dow rose for a seventh straight day, its longest streak since March 2013. The Dow Jones industrial average, Standard & Poor's 500 index and the Russell 2000 index of small-company stocks closed at all-time highs this past Friday. The modest pickup in stocks came on a day of relatively light trading following the holiday break for U.S. markets with many market participants still out for the Christmas break. The stock market has been mostly climbing since hitting a recent low of 17,069 on Dec. 16 on worries about plunging oil prices and a sharp drop in Russia's currency. Since then, investors have been encouraged by signs of a strengthening U.S. economy, which the government estimates grew in the July-September quarter at the fastest pace in 11 years. Consumer spending and personal incomes have been rising. The economy has been creating more jobs. As we head into year-end, treasury bonds continue to be the top performer as this asset class has been in a bullish trend all year basically unabated.

Last week we noted "...We still need further confirmation to see if there is a new uptrend, especially considering momentum is still flashing bearish signs..." The updated Bullish Percent Index chart below confirmed the recent uptrend move, but the trend is probably converting into sideways action because prices should consolidate going into year-end.

Last week's analysis said, "...the inverse relationship continues to play out as the previous week's trend reversed. The dollar returned to recent highs while treasuries and precious metals pulled back..." In the updated chart below you can see that Treasury Bonds and Gold stabilized as the Dollar stopped ascending higher.

Market Outlook

Wall Street's "Santa Claus" rally kept delivering gifts a day after Christmas. As we have been saying recently "...The December seasonal pattern performed as advertised with the major indexes generating the best weekly gain in months. Officially the so-called "Santa Claus Rally" is the seven-trading day period begins on the open on December 24 and ends with the close of trading on January 5. Normally, the S&P 500 posts an average gain of 1.5%. The failure of stocks to rally during this time tends to precede bear markets or times when stocks could be purchased at lower prices later in the year...." The markets also have history on their side. December is typically the best month of the year for stocks, while January is the second-best.

Last week we said "...As the fourth quarter winds to an end, the chart below shows that Real Estate remains the top performing asset class. But other sectors that are coming on strong such as the small cap Russell 2000 and DOW Transports signal that investors are confident about future economic performance. Particularly the Russell 2000 is considered a bellwether for near term direction on where the market is headed..."

Last week we mentioned "...the recent downtrend line has been broken with a new uptrend. Also noted is momentum is turning bullish to confirm the market should finish the year on an up note..." In the updated Momentum Factor ETF (MTUM) chart below we highlight where prices are consolidating at recent highs. Also note that momentum indicators are neutral which suggest near term range-bound trading until prices break higher or lower.

Last week's analysis is still valid "...you can see the market returned to recent highs while the Volatility index plummeted. Expect the VIX to continue downward as traders have moved past the recent market hiccup and are more confident in the market heading into next year..." The updated chart below indicates the current VIX move should sustain into year-end.

As we have been saying recently "...the best bet is still moderate price movement over the next week or so with prices spurting higher into year-end..." The current American Association of Individual Investor Survey (AAII) survey result is excessively bullish. As a contrarian indicator, the current reading supports the analysis that price consolidation is due and possibly a price pullback.

Third-quarter National Association of Active Investment Managers (NAAIM) exposure index averaged 71.09. Last week the NAAIM exposure index was 65.12%, and the current week's exposure is 90.59%. Money managers are significantly increasing exposure for year-end window dressing. Basically this means to impress clients, investment advisors want to display top performing stocks on their list of investments, regardless of whether they actually generated a gain on these shares.

Trading Strategy

The equity market appears to be reaching a summit as it has crawled to new highs on relatively light volume during the end of year holiday season. Last week, eight of the 10 sectors in the S&P 500 index rose, led by utilities stocks. The sector is up 27.9 percent this year. Energy posted the biggest decline, deepening its slide this year to 9 percent. As seen in the graph below, Utilities are far and away the best performing sector over the past month. This suggests that investors are taking a 'risk off' trading approach, as utility stocks generally are considered safe, stable and maintain value compared to other shares during market fluctuations. A standard year-end trading strategy is to sell off underperformers and shares that have attained their profit target. Losing trades during the year should be offset against profitable trades to minimize the tax burden. Also, it is good strategy to have a large cash positon going into the New Year to have the option of bidding on stocks that have high profit potential.

Regards,