The ECB fired its "bazooka" today, cutting official rates more into negative territory, increasing QE by another €20bln per month, expanding the range of assets the central bank can buy to now include corporate bonds, and creating a new 4-year program whereby the ECB will loan long-term money to banks at rates that could be negative (based on bank credit extended to corporate and personal borrowers).

My point today is not to opine on the power or wisdom of these policy moves. The main thing I want to observe is this: the inflation market is pricing in what amounts to success for global central banks, with consumer inflation averaging something between 1 and 2 percent per year for the next decade (a bit lower in Japan; a bit higher in the UK). Not only are inflation swaps prices much lower than would be expected from a pure monetarists' standpoint - but options prices are also very low. The chart below (source: Enduring Investments) shows normalized volatilities[1] over the last five years for a 10-year, 2% year-over-year inflation cap. That is, every year you take a look and see if inflation was over 2%. If it was, then the owner of this option is paid the difference between actual inflation and 2%; if it was not, the owner gets zero. So you get to look ten times at whether inflation has gotten above 2%, and get paid each time it has.

The chart shows that whatever inflation is expected to be, the price to cover the risk that inflation is actually somewhat higher is very low. So, not only is inflation expected to be low, but it is expected to be not volatile either.

Look, we're talking about bazookas, helicopters...does something not seem right about pricing in very little risk of screwing up?

Whether you believe my thesis in my freshly-released book What's Wrong With Money?[2] that the likely course of inflation over the next few years is higher and potentially much higher, or you agree with those who think deflation is imminent, shouldn't we agree that bazookas introduce volatility?

Central banks are attempting to do something that has never been done. Shouldn't we at least be a teensy bit nervous, as they line up to perform the first-ever quintuple-lutz, that no one has ever landed one before? That no one has ever landed a commercial passenger jet on an aircraft carrier?

Uncertainty is supposed to lower asset values, all else being equal. So even if you think stocks at these levels are "fair," in an environment with earnings and interest rates where they are now and projected earnings following a certain path, an increase in the volatility of those outcomes should lower the clearing price of those assets since the buyer of the asset (which has positive value) is also assuming the volatility (which has a negative value).

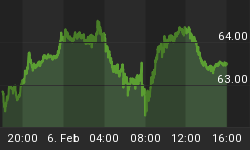

But the market also says that uncertainty right now is low. Yes, the VIX is well off its lows and seems to suggest greater short-term uncertainty (see chart below, source Bloomberg) - but I would argue that the long-term volatility of the economic fundamentals has rarely been this high.

Supposedly you can't roller skate in a buffalo herd,[3] but we also have never tried to do it. There's a reason we haven't tried to do it!

But the Fed, and the rest of the world's central banks, are not only roller skating in a buffalo herd - the world's markets seem to be suggesting that investors are sure they're going to succeed. Regardless of whether you're optimistic about the outcome, I would argue it's nearly impossible to be both optimistic and highly confident!

[1] This means something to options traders but can be glossed over by non-options traders. Essentially the point is that you can't use a regular Black-Scholes model to price options if the strike and/or the forward can have a negative value!

[2] #1 on Amazon in "Economic Inflation," thanks largely to all of you!

You can follow me @inflation_guy!

Enduring Investments is a registered investment adviser that specializes in solving inflation-related problems. Fill out the contact form at http://www.EnduringInvestments.com/contact and we will send you our latest Quarterly Inflation Outlook. And if you make sure to put your physical mailing address in the "comment" section of the contact form, we will also send you a copy of Michael Ashton's book "Maestro, My Ass!"