But it's not the high oil price, stagnant housing market, dissipating consumer spending, or even the declining corporate profits that hammered the market last week. Wall Street may be living (and making a living) in denial, but the market has been fully aware of all that and more. Demand for oil has been relentless while supply has been limited. Home selling activities and consumer spending have been tardy. Corporate profits had already declined $54.4 billion in the 3rd quarter of 2005 (see Chart 1). These are all things that have been coming for sometime now. It's unlikely that the shellacking on Friday was the market's reaction to these same old stuff.

Chart 1

The extraordinary surge of the VIX Index on Friday indicates that the market action was more of a reflex than a true sentiment. The market basically spent the entire week last week backing and filling the gaps (black circle on Chart 2). Friday was no different than the other trading days except that it was an Expiration Friday for equity options. And, in the process of filling Thursday's gap, it suddenly brought many out-of-the-money put options back into play. One of my Google March put options, for example, gained more than 300% during the day on Friday. This left many traders with no other choice but to liquidate their equities to cover the orders. That further exacerbated the market skid.

In any case, except for Expiration Friday related market volatility, Friday was merely a continuation of the market's reaction to the shock that was first felt on Tuesday, January 17, 2006, across the Pacific.

Chart 2

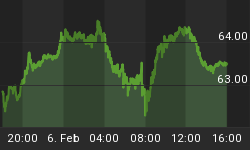

TSE (Tokyo Stock Exchange) Mothers Index fell straight from 2,799.06 on 1/16/2006 to 2,171.45 on 1/18/2006. Although a little pick-up took place on Thursday, 1/19/2006, the Index tanked another 6.64% to 2,138.78 on Friday, 1/20/2006. All said, the Mothers Index has lost 23.59% in the last 5 trading sessions (Chart 3). Many of the companies listed on TSE Mothers Index are start-up Internet or tech companies. The plunge of Mothers Index triggered a global tech-stock selloff.

And, that's what's shaking. That's the news the market's still trying to absorb. The market, hence, may stay quite volatile until what happened on the other side of the Pacific gets sorted all out.

Chart 3

From December 2004 to January 2006, TSE Mothers Index gained more than 76% in just about 13 months. Mothers Index was initially set up in late 1999 to provide venture companies access to funds at early stages of their development. Mothers Index stands for Market Of The High-growth and EmeRging Stocks. This is the high octane, high risk, small cap sector that led the Japanese stock market to its recent plateau, and, of course, its demise. This is where the increasing number of young Japanese on-line traders day trade. About 80% of Mothers Index investors are individuals. Only 3% to 4% of the investors are financial institutions.

And so, before Tokyo Nikkei Average was able to reclaim 50% of the loss from its peak in early 1990, a Japanese stock market bubble had just formed and then quickly ruptured last week. It's not unthinkable that Japan may never return to, or coming close to, its glory days of the 1980s again.

The most recent Japanese business survey available from the Ministry of Finance shows a cross-sector declining trend of general domestic economic condition outlook. BSI (Business Survey Index) shown on Chart 4 is the percentage of companies saying that domestic economic conditions are rising compared with the previous quarter, minus the percentage of companies saying that domestic economic conditions are declining compared with the previous quarter. And, companies, large and small, seemed growing more pessimistic about their domestic economic conditions.

Chart 4

Newer data also confirm this pessimistic sentiment. The 2005 3rd quarter Japanese GDP data shows no visible trend of growth of household consumption (Chart 5). In fact, the annual rate of growth from previous quarter has been in decline 3 consecutive quarters in a row. It might've already topped out after the 2003 4th quarter peak.

Chart 5

Without a strong domestic demand, Japan's economy continues to be dependent of exports. While Japan's trades with Asia have been improving, the bulk of Japan's exports still go to the U.S.. This, of course, takes us right back to the issue of American consumers' spending slowdown as a result of the housing market slowdown. And, that's not going to help Japan's return to its glory days.

One of my household's biggest phone expenses is the overseas calls to Japan. What I've heard from friends and relatives in Japan is quite contrary to what Wall Street is saying nowadays. Japanese Main Street continues to experience a sluggish economy that has promised to rebound but has yet to come through.

Here's Japan's GDP annualized rate of change from previous quarter (Chart 6), taken right out of Japan's Department of National Account's recent GDP report. After a promising 1st and 2nd quarters in 2005, it dipped back into the negative territory again in the 3rd quarter. But then, that's just the story of Japan's economy.

Chart 6

By all means, the size and the capital structure of Japan's economy remains to be a force to be reckoned with, but the current performance and outlook of its economy does not warrant this type of high flying stock market action. For an exporting country that has little natural resources and a growing aging population to be Wall Street's consensus as investment opportunity of the 2006 and beyond is, to put it politely, incomprehensible. The 70s band, Jethro Tull's 1976 album title - Too Old to Rock 'N' Roll: Too Young to Die! - came to mind as perhaps the best way to describe the current state of Japan's economy.