For weeks we've been saying the prevailing economic environment would not allow a dramatic selloff in metals. Of course, that didn't keep mainstream media from discussing a so-called "metals meltdown" and a "commodities collapse", or from making premature judgments about inflation. Spikes in corn, wheat and orange juice should put an end to these comments for a while, not to mention the small rally in oil. While Friday's bounce could be short lived if it's based primarily on potential OPEC meetings and cuts, there were technical indications that a reversal was due.

But, even if oil markets are still crashing and burning, the smoke is clearing around what was supposedly a breakdown in commodities only to reveal the spot price of gold still above $600 and silver still above $12. In fact, last week this was one of the few, if not the only, weekly update suggesting that the bounce off these levels was a buy signal. In fact, we've been sticking our neck out for more than a month saying that the environment simply has not existed for a huge precious metals selloff to the September lows.

With the recent dollar rally showing its limited upside, as anticipated here in previous updates, gold and silver stayed resistant to selling most of the week and finally put in impressive moves on Friday to close back above recent support/resistance levels. The big question now, though, is how much upside, if any, we should expect to see from here.

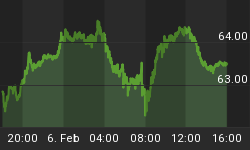

The daily charts below reveal that GLD is now very close to resistance at its 50-day moving average. A convincing move to $63 in the ETF would echo the signal that the spot market has cleared a path to $640 gold, but it will take more than technical impetus alone. Silver has even more room to run if it can retake $13, where it will likely see significant resistance. Both metals probably still have players who recently bought at higher levels, as well as some who will have just seen decent gains, and if the metals turn back south on their exit, $600 and $12 will again be the key psychological support levels to test.

The first update of this year included multi-year trend lines to which a conservative estimate predicts the precious metals will likely revert, either through selloff, a worse-case scenario, or sideways action. These charts are still operative and serve as reminders that overly fast gains in the metals will most likely evaporate just as quickly, even while the upward trend remains intact.

In the short term, if next week's data continue to nourish the sentiment that the economy has rounded the bottom, a veritable soft landing, then metals have a realistic shot at overtaking resistance. The hotter the economy appears to become, the more willingness investors should have to get back into mining stocks and the greater the inflation concerns will become. Oil is probably set for more upside next week if the weather is cold and this should help metals given that traders are too complacent towards inflation at the moment if their judgment is based on oil prices alone. A upside CPI surprise could send dollars after gold. Recent reports indicate the rate of increase in the money supply as measured by M2 rose somewhat dramatically over the last quarter of 2006 and there generally appears to be an abundance of liquidity. However, with the week kicking off with earnings reports from several financials, there could be renewed worry over the effects of the still inverted yield curve.

We should note that the yield curve, which is said to predict events 12 months into the future, just quietly celebrated the one-year anniversary of its late-December 2005 inversion without much, if any, mainstream attention. True, the yield on the 2-year note is now approaching 5%, and the quarter point difference from the Fed Funds rate has some still hoping for a single cut from Ben Bernanke, but none seems likely with GDP estimates being revised upward and housing fallout contained. Ironically, the economy's new perkiness is mildly re-inverting the curve as rate cut expectations plummet and investors seek outsized returns from record-breaking stock markets. Particularly if oil makes a big move, the securities may be due for a bit of a rally in the near term.

Over the past two months, we've articulated a firm position that expectations of a Fed rate cut were overdone. Since then, Fed Funds futures have priced out any possibility of a cut, bond yields have moved closer to the target rate, the dollar has rallied, commodities have come in, and equities have moved towards the hands of investors betting on strong earnings rather than simply depending on handouts from the Fed. The liquidity coaxed out of the bond market over the last quarter has helped fuel record-breaking private equity buyouts and a nice little bull market in the precious metals.

Now that we've been validated, perhaps it's time to reemphasize our position all along, which was that we don't actually anticipate any change in the fed funds rate in the foreseeable future. In fact, we've commented before that, because of its tenuous situation between the health of the economy and the value of the dollar, the Fed would probably rather make behind the scenes, open market adjustments rather than create international headlines by changing interest rates. And interest rates are a crude tool, anyway.

But, since the rise in bond yields coincided with rapid expansion of the money supply by the Federal Reserve, the Fed may soon be forced to look at easing the economy and removing some liquidity. It's purely speculation, and maybe even outrageous to even wonder, but could the plan offered by George W. Bush in his address to the nation last week regarding Iraq present the solution to liquidity by way of higher oil prices, runaway inflation, and possibly even a normalization of the yield curve, while sparking the next leg of the metals bull? Now that the president has widened the scope of the war in Iraq in words and action and is promising a "bloody" year ahead, will violence in Baghdad and aggression towards Iran finally deliver the recession no one any longer expects?

Stranger things have happened. In fact, without dwelling on or regurgitating our own political sentiments, we can admit that comparisons have already been made between the conflicts in Iraq and Vietnam, politically and militarily and economically. The undisputed fact is that issuance of massive government debt in the 1970s, along with a swelling in the monetary base, created huge inflation, drove up interest rates, swung the economy into recession, and, of course, brought on the biggest gold spike ever.

The situation today appears similar, though juxtaposed at lower nominal interest rates, so, maybe it's almost time for those comparisons to the 70's bull market that sprang up everywhere a few years ago to stage a comeback of their own. The growing cost of the Iraq war continues to produce huge budget deficits and the Fed's own data indicate that money supply has increased at a rate of 5% for the last year and 10% over the last four months. The fact that the current deficits are a smaller part of GDP may prevent the economy from spinning out of control, but with demand for metals keeping steady pace or even exceeding supply over the past several decades, it wouldn't take the same double-digit interest and inflation rates to have a situation in gold similar to what was seen in the 70s. And that, folks, was what you could call a bull market!