Global financial markets turned in mixed performances this past quarter. While equity markets generally rose over this period, bond markets did not fair so well.

Global financial markets turned in mixed performances this past quarter. While equity markets generally rose over this period, bond markets did not fair so well.

International portions of portfolios suffered sizable currency-related set-backs due to the Canadian dollar (CAD) suddenly spurting upward. Though the Canadian currency still remains below its year-ago highs against the euro, it surged 8.58% against the US dollar (USD) this past quarter. While investors may be dismayed that the CAD and Canada's domestic export industries can be so vulnerable to the sometime erratic whims of foreign capital flows, our research continues to support the opinion that the CAD is overvalued. Further comments on the CAD and its expected impact upon future portfolio returns are found in the conclusion section.

Where is the Risk? As always, we focus upon opportunities, ... but not without first understanding risks. That said, risk can be a difficult concept to understand. Risk to us simply means vulnerability to significant market setbacks. This may be as a result of expensive investment valuations, unstable financial conditions, imbalanced global macroeconomics, geopolitical or other factors, either individually or all taken together.

Of course, such indications are not necessarily predictive over the short-term. Therefore, when we say high risk, we do not mean to imply that any near-term developments can be forecast. It simply means that an above normal level of vulnerability exists ... that probabilities of reasonable returns are declining.

Markets may in fact continue to benefit from a decline in the fear of such risks. If investors are very confident, as usually becomes the case in later stages of economic or credit expansions, they are likely to ignore growing risks. However, when negative developments sufficient to change investor sentiment finally occur, asset markets have little to support them as they have been buoyed by not much more than confidence.

Quite frankly, the confidence expressed in financial markets has shown itself to be quite resilient in recent weeks and months. Though bond markets were virtually in a free-fall at one point this past quarter, only minor fears have emerged. Risk spreads have not widened substantially, nor have the "carry trade" currencies strengthened sharply. Yet, all the same, we continue to identify heightening risks, or better explained, risk levels, without adequate or reasonable promise of compensation.

A good example to illustrate the dynamic between vulnerability and expected returns -- in other words, risk -- is the recent housing bubble in the United States (also impacting parts of Canada). Once housing prices were rising, after some time this trend became a confident and continuing expectation. As long as housing prices were expected to continue rising, it made sense to some buyers to borrow heavily (and to others, to lend cheaply or innovatively). Generally, this had the effect of further boosting housing demand, which in turn further supported prices. It became a mutually reinforcing cycle to the upside.

Second Quarter Report | ||

| Market Update • During the past quarter, international equity markets in Canadian dollars declined 1.8%, US equity markets fell 2.2%, while Canadian equities (MSCI Index) rose 6.0%. With respect to fixed-income markets, a Canadian bonds declined 1.3% and international fixed-income returns suffered mainly due to Canadian dollar strength. • The Canadian dollar strengthened sharply against the US dollar (USD) over the past quarter by 8.6% -- a record by some estimates. In the meantime, the Canadian dollar remains under its highs set against the euro over a year ago. The USD has | continued to weaken against the euro. Investment Posture | |

However, gradually, several "risk" factors began to cumulate. Housing prices became expensive relative to household incomes, and secondly, potentially unstable financial conditions developed as overall debt levels soared.

While it may be obvious that such trends are not sustainable indefinitely -- in other words, that risk levels are rising unacceptably -- such concerns can seem very silly to buyers who remain confident that housing prices must continue to rise. As with all historical financial bubbles, something eventually transpires that ends the party and extinguishes optimistic expectations. The exact trigger or catalyst may not be predictable, but what is probable is that whenever such a trigger happens, markets are likely to be vulnerable and stumble. This certainly proved to be the case with US real estate prices. For the most part, the bubble is now over and difficult years likely still lie ahead.

Of course, one always hopes that sensibilities will prevail and that overheated financial markets will not become so excessive that the following fall-out will prove unnecessarily difficult. However, to this point, despite the credit market tremors of the past quarter, there has been little sign of concern within broader financial markets. All the same, we definitely observe several major shifts ... but, apparently invisible or ignored by market participants to this point.

There are plenty of risks that are going unheeded at present. In a speech to business people on the risks facing the global economy, former US Treasury Secretary Lawrence Summers said earlier this year, that geopolitics was at the top of his list. "There is a near complete disconnect between geopolitical risk and risk that is priced and perceived in financial markets. It's like something out of Dickens, you talk to international relations experts and it's the worst of all times. Then you talk to potential investors and it's one of the best of all times."

Other sober analysts share similar views. Says the International Investment Fund (IIF) "There are a number of downside risks, including geopolitical tensions with possible implications for energy prices, sharp slowdown in the U.S. growth or flare up in inflation, spillover effects from credit and financial market shocks, and disorderly adjustment of large global current imbalances." "The spectre of a disorderly adjustment of global imbalances lingers as an important element of unease in the current world economic scene. [...] the lack of a coordinated policy action by major economies aimed at adjustment could hasten a disorderly depreciation of the dollar." (Capital Flows to Emerging Market Economies, May 31, 2007, pg.5, 7.)

The OECD, (Organization of Economic Cooperation and Development) in its recent Economic Outlook says that its "analysis suggests that risk may be under-priced." (Economic Outlook No. 81, May 24, 2007, pg. 2.) We could quote other respected sources that are concerned about rising risks. Crucially, a recent World Economic Forum report (Global Risks 2007) concludes: "... levels of risk are rising in almost all of the 23 risks on which the Global Risk Network has been focused over the past year."

The Canadian Dollar Revisited. We have been wrong in our short-term view on the Canadian dollar against the US dollar. However, we can still find no fundamental reason to change long-term expectations. Against the euro, the CAD still remains below its highs of 15 months ago. All the same, the rise against the USD since its year-to-date lows has been violent. In a space of approximately only 4 months, the CAD surged 12.1%. This is usually the stuff of manias and lesserdeveloped countries. Only once before in the past 4 decades, has the CAD dollar showed such compressed strength. But, that was in 2003, after a deeply-undervalued CAD had languished near its all-time lows for some time. For the CAD dollar to rally from already over-valued levels with such vigor, smacks of heavy speculative flows. Indeed, we believe that this is the case. Recent surveys show that foreign investors have built up record long positions in the Canadian dollar. Also, not to be overlooked is the near unanimous "bullish" pollings among US investors rating Canada as the most promising foreign country.

The Canadian Dollar Revisited. We have been wrong in our short-term view on the Canadian dollar against the US dollar. However, we can still find no fundamental reason to change long-term expectations. Against the euro, the CAD still remains below its highs of 15 months ago. All the same, the rise against the USD since its year-to-date lows has been violent. In a space of approximately only 4 months, the CAD surged 12.1%. This is usually the stuff of manias and lesserdeveloped countries. Only once before in the past 4 decades, has the CAD dollar showed such compressed strength. But, that was in 2003, after a deeply-undervalued CAD had languished near its all-time lows for some time. For the CAD dollar to rally from already over-valued levels with such vigor, smacks of heavy speculative flows. Indeed, we believe that this is the case. Recent surveys show that foreign investors have built up record long positions in the Canadian dollar. Also, not to be overlooked is the near unanimous "bullish" pollings among US investors rating Canada as the most promising foreign country.

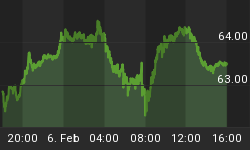

However, none of our fundamental analysis with respect to the Canadian dollar's value has changed. In our view, the CAD is overdue for a longer-term down-cycle against the USD. Figure #2 on this page puts the CAD recent rise in perspective. As such, though currencies can add volatility, we see no reason to believe that long-term prospects for internationally diversified portfolios have diminished. In fact, if anything, they are now heightened.