After watching 3 days of unrelenting rally from Monday through Wednesday, which pushed the DJIA (Dow Jones Industrial Average) up more than 530 points, the ferocious action reminded me of the symptom of binge eating (see 8/8/2007 Overreactions). The next day, the DJIA dropped 387.18 points (2nd worst of the year), and this purge after binge eating reminded me of a case of bulimia - a case of Market Bulimia.

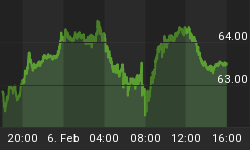

This disorder is depicted on this 10-day, 30-min intraday chart (Chart 1). Bulimic binge eating is known to be responding to depression or stress. It brings on a feeling of happiness, but the sense of loss soon replaces the euphoria. The purging process that follows is an attempt to get back to the equilibrium in order to regain control. And, that's what the market's going through right now; the market's responding to all the stress currently in the system and attempting to return to the equilibrium in order to regain control. It's not out of the ordinary for the market to go through a stretch like this. Chart 1 shows that after huge swings of 279 to 638 points over the past 2 weeks of trading sessions, the DJIA ended almost unchanged (dotted line). Thursday's selloff was merely a symptom of Market Bulimia.

Chart 1

Wall Street that otherwise advocates free capitalism and minimum government regulations, nevertheless, thought differently. After years of prosperity in the environment of low volatility, Wall Street fund managers' golden geese, the market-neutral computer trading models, had stopped laying golden eggs. The panic kicked in. And, rather than leaving the market to work its way back to the equilibrium, pundits and analysts of all sorts came on to plead their cases for intervention. Some even beseeched on behalf of the average homeowners and consumers because, I assumed, they care so much.

Thursday's liquidity crunch was said to have been caused by problems in the subprime mortgage sector. And, the Fed took the bait and came to their rescue. The Fed thus pumped a total of approx. $49 billion into the system on Thursday and Friday through temporary repo of the MBS (Mortgage Back Securities).

And, I wondered... Why?

The system didn't seem in that much of a need for a relief of this magnitude. The MBS propositions submitted to the Fed's trading desk by primary dealers, prior to the Fed's "rescue" mission on Thursday, 8/9/2007, had actually been in decline. Chart 2 below shows a clear declining moving average (thick black curve) of primary dealers' bids from mid July to Wednesday, 8/8/2007 (see red arrow). The demand for the MBS repo had been waning.

Chart 2

2-year longer term view of accepted MBS bids also shows a recent declining trend that started in mid June (see red arrow on Chart 3). However, the Fed's action on Thursday and Friday had pushed the temporary MBS repo into the stratosphere (blue double arrow); it's now at a much higher level than the May-June 2006 market correction period (black arrow). This was perhaps a blatant overreaction to bail out Wall Street. It's questionable whether there's any trickle-down benefit for the average Joes.

Chart 3

The bailout is further evidenced by repetitive patterns of 7-8% limit of the past market corrections. Every correction since the market rebounded in 2004 had been limited to the threshold of 7%-8% (see Chart 4 below). It tells us, plainly, that the domestic market corrections within the 7%-8% range of the S&P 500 Index is considered tolerable and perhaps manageable. Any loss beyond that may get out of control. The 3-day binge buying last week shows that this is a well known fact.

Chart 4

The above referenced 3-day fierce 5%+ rally of the S&P 500 started on Monday, 8/6/2007, just 1 session after the Index closed at 1433.06, the lowest since March. However, by now, the correction from the 7/16/2007 intraday high of 1555.90, had reached almost 8%. The binge buying over the ensuing 3 days was spectacular before the startling interruption arrived from abroad on Thursday. Thursday's global selloff stunned those buyers who'd been buying on the blind faith of the 8% rule. That counter force from around the world was indeed quite a shock to the system here.

The suspension of 3 funds by the French bank, BNP Paribas, re-confirmed that the well published subprime mortgage problem was not only a global phenomenon, but it's also still very much alive. This confirmation from overseas induced the market to purge. Nonetheless, the subprime problem, no matter how much worse it had become, didn't just show up at the party last week; it's been a process. And, there had been little demand for MBS repo's (see Chart 2 & 3) because financial institutions can absorb the loss, and the market will regain control on their own.

What happened last week was merely a case of Market Bulimia. The financial media's overreaction and the Fed's determination to uphold the 8% rule may further exacerbate the disorder.