Market Summary

The market is experiencing jitters ahead of the presidential election with a series of lower highs and lower lows. For the week, the benchmark S&P 500 Index finished down .07% while the Blue Chip-heavy Dow Jones Industrial Average ended flat. Both the Nasdaq and the small cap Russell 2000 indices fell 1.3%. The major equity indexes are holding on barely above water year-to-date. Gold has been a stellar performer for most of the year but has been crashing as investors expect an imminent rate increase which normally has an adverse effect on commodity prices.

A standard chart that we use to help confirm the overall market trend is the Momentum Factor ETF (MTUM) chart. Momentum Factor ETF is an investment that seeks to track the investment results of an index composed of U.S. large- and mid-capitalization stocks exhibiting relatively higher price momentum. This type of momentum fund is considered a reliable proxy for the general stock market trend. We prefer to use the Heikin-Ashi format to display the Momentum Factor ETF. Heikin-Ashi candlestick charts are designed to filter out volatility in an effort to better capture the true trend. The updated chart below displays stocks recent downtrend. You can see the MTUM has fallen to the support level established in the middle of September right before stocks recovered. If the market doesn't stage a recovery bounce after the November election the downtrend will probably continue heading into the December Fed meeting.

In the chart below after surging higher since the end of September, the U.S. dollar's advance finally slowed with a weekly loss, even though the greenback is up 3% for the month of October. Treasury prices fell sharply this week due to growing worries over the potential for inflation and uncertainty about the outlook for central bank interest rate policy. Gold prices finished higher last week, logging a third consecutive weekly gain and their highest close in nearly four weeks as weakness in the U.S. dollar and a new probe into Hillary Clinton's emails raised the metal's appeal as a safe-haven investment. Colin Cieszynski, chief market strategist at CMC Markets, told MarketWatch that "It looks like the recent selloff in gold is over and it's starting to turn back upward, while the U.S. dollar looks overextended and [is] peaking,".

Market Outlook

The stock market has been unable to find a catalyst to confirm a breakout higher or lower. In early September, it was the fear of a Fed rate rise that caused stocks to gap down for a couple of days. Then when the Fed kept rates unchanged, the following rally seemed strong for a couple of days as well. But the S&P 500 Index has traded within a 3% price range for the past six weeks. Late in the month, there was a scare that Deutsche Bank is in trouble, and that caused some heavy selling last week, but it has not had much follow-through either. In the chart below, since the S&P 500 Index attained all-time highs in the middle of August, all of the major asset classes have stumbled, some more than others. We doubt if the presidential election will be the stimulus to drive the market, more likely it will be investor reaction to Fed policy after the election.

Put/Call Ratio is the ratio of trading volume of put options to call options. The Put/Call Ratio has long been viewed as an indicator of investor sentiment in the markets. Times where the number of traded call options outpaces the number of traded put options would signal a bullish sentiment, and vice versa. Technical traders have used the Put/Call Ratio for years as an indicator of the market. Most importantly, changes or swings in the ratio are seen as instances of great importance as this is commonly viewed as a change in the tide of overall market sentiment. Put/call ratios have rolled back down to sell signals from buying. The current ratio indicates traders are nervous ahead of the November election as they are buying more option put contracts to hedge against lower stock prices.

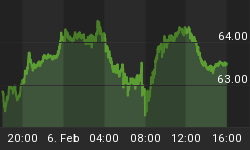

The CBOE Volatility Index (VIX) is known as the market's "fear gauge" because it tracks the expected volatility priced into short-term S&P 500 Index options. When stocks stumble, the uptick in volatility and the demand for index put options tends to drive up the price of options premiums and sends the VIX higher. You can see in the current VIX chart below how the Volatility Index has been fluctuating up and down in a trading range the past month. This behavior confirms the markets' indecisiveness where there has not been a catalyst to break the major equity indexes out of a trading range.

The American Association of Individual Investors (AAII) Sentiment Survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market for the next six months; individuals are polled from the ranks of the AAII membership on a weekly basis. The current survey result is for the week ending 10/26/2016. Optimism among individual investors about the short-term direction of stock prices is below 30% for the 10th consecutive week. Neutral sentiment rebounded, while pessimism pulled back. Bullish sentiment, expectations that stock prices will rise over the next six months, rebounded by 1.0 percentage points to 24.8%. Optimism is below its historical average of 38.5% for the 51st consecutive week and the 84th out of the past 86 weeks. Neutral sentiment, expectations that stock prices will stay essentially unchanged over the next six months, rose 2.7 percentage points to 41.2%. The increase follows what had been a four-week low. It also keeps neutral sentiment above its historical average of 31.0% for the 39th consecutive week. Bearish sentiment, expectations that stock prices will fall over the next six months, pulled back by 3.7 percentage points to 34.1%. Even with the decline, pessimism is above its historical average of 30.5% for the seventh time in nine weeks. As noted above, the percentage of individual investors describing their short-term outlook as "bullish" has now been below 30% for 10 consecutive weeks. During six of those weeks, optimism has been below 28.0%, the breakpoint between the normal range of readings and unusually low readings. Not surprisingly, the S&P 500 and the Russell 2000 have both declined over this period. Causing concern for individual investors is the lack of new market highs, the possibility of the stock market experiencing a larger drop, valuations, the November elections, global economic uncertainty and the pace of corporate earnings growth. Giving other individual investors reason for optimism are the perceived lack of investment alternatives, corporate earnings, low/stable energy prices and sustained, albeit slow, economic growth.

The National Association of Active Investment Managers (NAAIM) Exposure Index represents the average exposure to US Equity markets reported by NAAIM members. The blue bars depict a two-week moving average of the NAAIM managers' responses. As the name indicates, the NAAIM Exposure Index provides insight into the actual adjustments active risk managers have made to client accounts over the past two weeks. The current survey result is for the week ending 10/26/2016. Third-quarter NAAIM exposure index averaged 80.32%. Last week the NAAIM exposure index was 63.70%, and the current week's exposure is 66.47%. As seen in the updated chart below, professional money managers have backed off of lofty equity exposure levels at the end of the summer. The current lower NAAIM number reflects money managers' cautiousness ahead of the November election and December FOMC meeting.

Trading Strategy

Jeff Hirsh in the Stock Trader's Almanac talks about how November begins the "Best Six Months" for the DJIA and S&P 500, and the "Best Eight Months" for NASDAQ. Small cap stocks start percolating in November but don't usually take off until the end of the year. November is the number-three DJIA and number-two S&P 500 month since 1950. Since 1971, November ranks third for NASDAQ. November is also a very strong month for the Russell 2000. November maintains its status among the top performing months as fourth-quarter cash inflows from institutional investors drive November to lead the best consecutive three-month span November-January. In the updated S&P sector graph below, investors appear to be anticipating a Clinton election win as Healthcare stocks have been decimated over the past month. Financials are the only positive S&P group the past month as investors seem to be anticipating a Fed rate increase which generally benefits the bottom line of financial institutions. Now might be good time to look for an entry price for stocks on your watch list or consider low priced option call spreads to minimize trading risks while waiting on the market to rebound.

Feel free to contact me with questions,