Prior to the holiday weekend the markets learned the median price for existing home sales declined 8% from the year-earlier period. More concerning was the inventory of unsold homes climbed 11% resulting in a backlog which would take more than 11 months to clear based on the current rate of sales. While a record average gasoline price of $3.875 a gallon may have distracted many economic observers, we should not forget the prior positive economic impact related to the housing boom. Approximately 74% of all new jobs created between 2000 and 2005 were related to housing in some way (agents, brokers, construction workers, architects, etc). As of this writing, there appears to be no sector of the American economy ready to step forward and fill the void being rapidly vacated by housing. As a result, calls for an end to stimulative Fed and government policies may have been premature.

Investors Are Taking A Step Back From The U.S.

After a sharp correction in any asset market, it is not unusual for investors to play the bounce all the way back to the market's 200-day moving average. This is known as basic support and resistance trading. For the market to clear the 200-day moving average (resistance) you need fundamental buyers to step in and help make the final push higher. As a market approaches the 200-day moving average many investors ask, "Do I really want to own this based on the long-term fundamentals?" In the case of the S&P 500, the initial answer appears to be "no".

The S&P 500 Fails To Clear Its 200-Day Moving Average (red line)

After a significant and protracted downturn, long-term investors should wait for any market or asset class, including the S&P 500, to clear its 200-day moving average before committing significant amounts of capital. If the March bottom turns out to be "the bottom" and the start of a new bull market, there will be plenty of time to profit from the new trend.

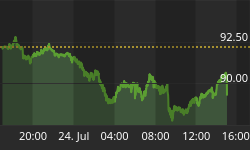

The dollar has been unable to sustain any type of trend-breaking rally with the negative economic clouds hanging over the U.S. As shown in the chart below, a serious move toward the dollar's 200-day moving average has not been within reach, which means it remains firmly in a downtrend.

Dollar's Recent Rally Is Faltering

The U.S. bond market has an important tug-of-war going on between safety and inflation/debt. Similar to the U.S. dollar, U.S. government bond investors show confidence in the U.S. as a whole and the government's ability to meet its obligations when they buy bonds. In the current downturn, the desire for safety has prevailed to date. With massive trade and budget deficits, along with a falling dollar, it is only a matter of time before investors begin to question the safe haven status of U.S. government bonds. As economic and currency risks rise, investors will command a better return on their U.S. government bonds. A higher return on government bonds means higher interest rates for mortgages, credit cards, business loans, etc. Higher interest rates would not be welcome in an economy saddled with debt. There is nothing yet too alarming about the chart below, but it bears close watching.

10-Year Treasury Yield: Rising Bond Yields Are Bad For The Unbalanced U.S.

The charts below of U.S. financial and housing stocks show little to get excited about as of the market's close on Friday, May 23, 2008.

Financials: A Dead Cat Bounce?

Housing Stocks Continue To Hit A Wall At 200-Day Moving Average (red line)

Commodities Are Strong, But Economic Weakness a Concern

While commodity investors are well versed in the India-China demand story, it is prudent to acknowledge the historical correlation of annual GDP (YOY % CHG) and the CRB Index.

Commodities: What Is Driving Prices?

-

Hedging, investment, and speculation

-

Loose monetary and fiscal policy

-

Weak U.S. dollar

-

Expensive to drill, mine, refine, and ship

-

Regulatory hurdles to adding capacity are high

-

Declining production rates in some markets

-

"Flat World" demand from India, China, etc.

Commodities: What Should We Be Concerned About?

-

Speculation

-

Cyclical nature of demand / economic weakness

-

Volatility even within context of secular bull market

CRB Index Continues To Make New Highs

Crude Oil Adds To Economic Concerns

Gold: A Close Above $955 Would Be Bullish