President Nixon instated price controls on the 15th of August, 1971. Inflation was a little over 4% at the time. Price controls manifestly did not work (resulting in shortages of all sorts and a deep recession) and were rescinded a few years later. President Ford went to Congress with programs to fight inflation that was running closer to 10% in October of 1974, with a speech entitled "Whip Inflation Now" (WIN). He famously urged Americans to wear "WIN" buttons. That policy too was less than effective, and the buttons, in a history replete with silly gestures by governments, should stand on anyone's top ten list of such silly gestures.

Cynics more thoughtfully wore the buttons upside down and said the inverted letters (which looked like NIM) stood for "No Immediate Miracles." They were right. There was no miracle, just eventual pain and lots of it. Ultimately, Paul Volker defeated inflation, but at the cost of two serious recessions and a lot of economic misery, with unemployment levels over 10% for nine months in 1983.

This week we were given the data that inflation as measured by the Consumer Price Index (CPI) over the last year was 4.2% and unemployment is now 5.5%. Some call for the Fed to raise rates so that we do not have to experience another lost decade like the '70s and then ultimately see some future Volker forced to raise rates and drive unemployment back to 10%. Others suggest that "core" inflation is what should be paid heed to, and urge caution.

This week we look at the cost of what could be a renewed effort to Whip Inflation Now, not just here but in countries worldwide. Will Trichet in Europe raise rates even as the European economy seems to be slowing down? If you think inflation is bad in the US and Europe, take a peek at Asia. And I ask, "What will Ben do?" It should make for an interesting letter.

Whip Inflation Now

Nixon and his advisors thought inflation at 4% was serious enough to institute price controls. Headline inflation in the US is now 4.2%. What kind of economic policy should we pursue to bring inflation back into the Fed's comfort zone of 1-2%? Would it work and would it be worth the pain? To get a handle on the question, let's go to the data from the Bureau of Labor Statistics and see where inflation is coming from.

And let me note, this is the same exercise we could do for a host of countries. The answer will be roughly the same: there are no easy solutions.

Core inflation, or inflation without food and energy, grew at 2.3%. Inflation without food costs was an even 4% and without energy was 2.7%. Clearly energy was the leading contributor to inflation in the past year.

But the recent trend in rising inflation is even more worrying. If you look at just the last three months of data and compute an annualized rate of inflation, you find that overall inflation has risen to 4.9%, energy inflation is running at a staggering 28%, and food costs have risen 6.2%. Meanwhile, core inflation during that period dropped to 1.8%. You can see all the data at http://www.bls.gov/news.release/cpi.nr0.htm.

Now, gentle reader, let's think about these numbers. Food (over 14%) and energy (over 9%) combined make up roughly 24% of the CPI, yet were responsible for over 60% of the recent three-month trend in inflation. By the way, housing was up 4.9% and transportation up 8.7%, so it was not just food and energy.

What would it take to drop headline inflation back to under 2%? Well, one way would be for food and energy prices to fall. Let's look at the possibilities.

As Donald Coxe has noted, North America has had an 18-year run of remarkably good weather in our growing season. You have to go back 800 years to get a string of years that were that good. Yet today food reserves of all types are at decades-long lows. There is very little room for any type of problem.

This growing season is not off to a good start. It looks like the yield on the corn crop will be lower than normal, and that is if we get very benign weather this fall. Given how late much of the US corn crop was planted, and how torrential rains in the corn belt have devastated crops (not to mention flooding cities, and our thoughts and prayers go out to those who have lost their homes to flooding), an early frost would be disastrous.

Because we have devoted so much of our arable land to corn (in a very misguided policy to turn food into ethanol), we have less for soybeans, which is putting upward price pressure on beans and other grains that are used to feed cattle, hogs, chickens, etc. In fact, it costs so much to feed livestock that ranchers are shrinking their herds.. This means more meat is coming into the system now, which is dampening prices. Increased supply will reduce prices in the short term, but next fall we will find that supplies of all types of meat will be short. That will potentially send meat prices soaring. Cereal and bakery products are up 10% over the last year. They could continue to rise in the fall if the corn crop does not yield more than currently projected. It will cost even more to feed your household and feed the animals we need for meat.

Food is the most basic of commodities. Demand is fairly consistent, and supplies may come under pressure. Looking for food inflation to drop back by the fall to 2% is not realistic in the current environment.

What about energy? There is some more hope there, at least on the oil front. High prices have reduced demand in the US, with gasoline usage down about 4%.

I think we have reached a tipping point. The psyche of the US consumer has been permanently scarred. Slowly, this country is going to replace its fleet of cars with smaller, more fuel-efficient cars. Over time, we will see demand continue to fall. We could see further drops in the demand for gas in the next few months.

Much of Asia used to subsidize oil prices to their consumers. That is changing, as Indonesia, Sri Lanka, and Taiwan have announced they are decreasing their subsidies, as the cost is simply too much. Malaysia now spends 25% of its budget on oil subsidies, and must raise prices or cut other services - or watch inflation get worse. India is now contemplating how to cut its subsidies. Even China is likely to start to raise costs after the Olympics. These countries are going to go through their own price shocks. All this will reduce world demand for oil.

And while there are those who are convinced the high price of oil is due to speculators, there are reasons to think the real culprit is still demand. Refiners are paying anywhere from $5-7 more per barrel than futures prices for "light sweet" crude (oil with low sulfur content) and $7 less for heavy sour crude. Much of the oil from the Middle East is of the latter variety, and supplies are increasing. There is not enough refinery capacity for heavy sour crude. That is why you see OPEC representatives say there is enough supply. For the crude they produce, there is. Spot prices are reacting to supply and demand and not speculative futures prices.

Over time, reducing demand should reduce price. I would expect to see oil get back to $120 or lower by the end of the year. But by year-over-year comparisons, inflation will still be ugly for some time. Oil prices have risen approximately 90% in the last 12 months (the actual percentage is highly dependent upon which measure you use). The bulk of that has been in the last four months. For energy inflation to go down on a year-over-year basis, we would need to see oil drop below $100. How likely is that in the next two quarters?

Where Can We Get Help on Inflation?

So, the two main sources of inflation are unlikely to drop in the next two quarters. If we want to get overall inflation down to 2%, we will need to look for help in other areas of the economy. How about medical care? Not likely. Education costs? Get real.

Housing costs make up 42% of the CPI, and thus are the biggest component. That is broken down into several categories: owners' equivalent rent for those who own their homes (32%), actual rent for those who do not (around 6%), utilities, furnishings, etc.

Rents have been up by 3.5% over the last year and owners' equivalent rent by 2.6%. If rent increases were to drop to zero, that would just about get us to 2% overall inflation. But let's think about that. Such a low number would mean an economy on its heels and a lack of buying power on the part of consumers. The only way that happens is with serious unemployment.

You can go to http://www.bls.gov/news.release/cpi.t01.htm and look at the various components of the CPI. Spend some time thinking about what costs are likely to drop. New and used vehicles are now dropping year over year, but only by a little, and that is only 7% of the index. Most items are rising at least a little.

Now, in a second thought exercise, think about what would happen if Bernanke decided to raise rates. A rising Fed funds rate is unlikely to have much effect on oil or food prices, unless he raises them enough to put the US and world economies in a serious recession.

How much would he have to raise rates to really slow the rest of the economy down? If you push up rates by 2% with the economy either in recession or close to it, you risk putting the economy into a much deeper recession.

Look at the yield curve below. This is exactly what the banks and financial services lend. They like to have a nice positive differential between the cost of their deposits and what they can charge for lending.

If you raise rates by 2%, you would more than likely invert the yield curve, making it that much more difficult for financial service companies to be able to recover. Given that they are already in trouble, and therefore less able to lend to businesses and consumers, do you really want to make things worse?

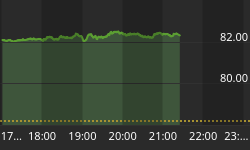

Look at the banking index below. This is an ugly chart. Another inverted yield curve would do serious damage to an industry already reeling. We are going to see more write-offs from banks. This chart will get uglier, but it will collapse without a positively sloped yield curve. (chart courtesy of www.fullermoney.com)

Further, raising rates would make it more difficult for consumers whose mortgage rates are tied to short-term rates. Is that what a housing industry needs right now?

Bottom line, Bernanke is in a very difficult position. Inflation by any standards is too high. But the cause of the inflation is not something in the Fed's control. To bring inflation back to 2%, he would have to savage the economy, perhaps at least as much as Volker did. Do you want to see unemployment go to 8-10%?

Volker was dealing with wage inflation. Everything had cost of living adjustments (COLAs) back in the late '70s and early '80s. Spiraling wages were one of the primary causes of inflation, if not the most important. A higher Fed funds rate could do something about rising wages by increasing the unemployment rate. Tough love, but effective.

Volker had to kill inflation expectations. Today, that is not (so far) Bernanke's problem. If you look at the implied inflation in the TIPS market, which is the difference between a ten-year treasury note and the ten-year TIP rate, it has only risen from a recent low of 226 bps on May 1 to 249 bps on June 10. Look at the following chart from Asha Bangalore of Northern Trust. Note that inflation expectations are not at recent highs.

The Patient Died Anyway

An expected inflation rate of 2.5% is well within "contained." It would be irresponsible to put the economy into a serious recession under such a set of circumstances. My Dad had a saying, "The operation was a success, but the patient died anyway." Raising rates in any serious manner would whip inflation but would kill the economy at this point. Rates will need to go back up at some point, but not until the economy shows signs of a rebound. I think the chances of the Fed raising rates by the 75 basis points, by January, that the market has priced in, is quite low.

What will happen is that over time the annual comparisons will begin to be less problematic. The cure for high prices is high prices, as the true cliché goes.

Sadly, we may get some help on the housing inflation component. Foreclosure filings last month were up nearly 50% compared with a year earlier. Nationwide, 261,255 homes received at least one foreclosure-related filing in May, up 48 percent from 176,137 in the same month last year and up 7% from April, foreclosure listing service RealtyTrac Inc. said Friday.

The prices of homes in many areas are going to fall to the level at which they can be rented. As more homes come onto the market for rent, the pressure on rent prices will fall. And the measure of owners' equivalent rent will fall along with it. Mark Zandi, chief economist of Moody's Economy.com (and an adviser to Republican John McCain's campaign), wrote earlier this week that "the Bush administration's efforts to encourage loan modifications and delay foreclosures are being completely overwhelmed."

Separately, a Credit Suisse report from this spring predicted that 6.5 million loans will fall into foreclosure over the next five years, reaching more than 8 percent of all US homes. (AP) That is going to keep pressure on housing prices for several years at the least.

Thus, it is likely that Bernanke and company will continue to talk tough on inflation. But, as noted above, I also doubt that they will raise rates this year, and probably not until well into the next.

The only reason to raise rates would be to protect the dollar from a serious collapse. I think it more likely the Treasury would intervene in the markets to prevent such a collapse. Dennis Gartman, at dinner Wednesday night, suggested that if the administration really wanted to get the market's attention, they could intervene in the currency markets and release oil from the Strategic Petroleum Reserve at the same time. While it would only be a temporary fix, it would make speculators nervous. However, they might consider such an experiment preferable to having the Fed raise rates during the middle of a slowdown/recession.

And the dollar seems to have found at least a temporary bottom, and we could see further strengthening next week, as Ireland voted today to reject the proposed European central government. Since it takes an absolute 100% consensus among all member nations, that kills the deal. Europe now has a very odd shape. They have a commercial union. Some of the members share a currency. Some of them share actual membership in the EU. Some of them are in NATO. They have competing and very different needs for monetary policy.

In fact, it will be hard to get anything done in Europe apart from commercial treaties, etc., as any one country can veto any particular item which is not to their advantage. Over time, this is going to be seen by the world as an issue for the euro. And given the demographic and pension problems of "Old Europe," the currency is going to come under increased pressure from competing needs for funding, taxes, and an easy monetary policy.

Six years ago I talked about the euro rising to $1.50, but I also noted that by the middle of the next decade it is likely to come back to par. We are halfway on that journey, and I still think we will arrive at my predicted point.

I think it is possible that the dollar could rise 10% or more this year against the euro, which would help inflationary pressures. Import prices into the US are up 17.8% year over year. A stronger dollar will help alleviate that.

Inflation in Asia and Europe

Countries throughout Asia would love to have a 4.2% inflation rate. Indonesia is at 10.4%, almost twice what they were a year ago. Vietnam would love to have such mild inflation, as its own level is up over 25%. Inflation in China is 8%. Inflation is up throughout the continent. And oil and food are the culprits.

Korea is particularly strained. Korea has seen its import prices rise by almost 45% in the last 12 months. Read this note from Stratfor:

"South Korea is among the most vulnerable of Asia's top economic players to global price increases due to its heavy reliance on imports for many of life's basic essentials - including oil, wheat, corn and coarse grains. At least 96 percent to 100 percent of its annual consumption in each of these items is imported. With global supplies in these basic necessities set to tighten, South Korea's inflation and the associated social unrest can only rise. (Protests in South Korea can draw hundreds of thousands of marchers.)

"Interest rate hikes are one of the most readily available tools for fighting inflation and for propping up a weak currency. In theory, raising rates would help attract foreign money into South Korea by raising the rate of return on investments in the country, thus helping to increase the value of the local currency and to contain rising energy import costs and inflation. But just June 12, South Korea's central bank decided to keep interest rates frozen at 5 percent. This was because the potential economic slow-down an interest rate increase could trigger is too politically risky for the government, and because there are less controversial means to bolster the won.

"If interest rates were raised to tackle the problem of increasingly expensive imports, the access of Korean businesses and households to credit to fund their operating costs or mortgage payments would shrink. This would make the government of President Lee Myung Bak even less popular."

What to do? Each country will try its own particular witch's brew. China is raising interest rates, increasing bank reserves, and allowing its currency to continue to rise. But make no mistake, there are no easy answers. Each choice has its own unintended consequences.

But a large part of the problem in Asia is food and energy. And monetary policy alone cannot address world supply imbalances. To a greater or lesser degree, every country is faced with the same conundrum. Do you risk higher unemployment and your economy to fight inflation that is not strictly speaking a monetary problem? If food is rising 40% in Vietnam, its workers will have to make more in order to eat? Will such a price increase force higher wages and perhaps a wage increase spiral like the US saw in the '70s? If you increase the value of your currency too fast, you risk losing your competitive price advantage and thus losing business and jobs.

There Are No Good Solutions

Over in Europe, I noted last week that one Jean Claude Trichet, the president of the European Central Bank, virtually promised the markets a series of rate hikes. This sent the dollar into the tank and the euro back to new highs. Gold loved it.

But this week has seen a very unusual set of speeches by fellow ECB members disavowing Trichet's promise, and even Trichet had to try and "explain" away what he had said. "We aren't talking about a series of rate hikes. Maybe, just possibly, we would raise in the event of more inflation." Confusion reigns. There is clearly not consensus at the ECB.

You can bet Trichet heard from various finance ministers in the countries whose economies are weakening. They are not interested in a stronger euro or higher rates. What one person called the PIGS countries are surely objecting (Portugal, Italy, Greece and Spain, whose economies are not exactly robust).

And their objections are the same ones that would be made here. What good would a rate hike do? How much more oil or corn would be produced? Why increase our pain when there could be no positive result?

The central banks of the world got by for years with easy monetary policies (think Greenspan) because of rising productivity, cheap energy, increased international trade, a disinflationary environment because of cheap Asian labor and imports, etc. Now that economic regime has come to an end. Stability had bred instability in a very uncomfortable Minsky Moment.

There are no good solutions. There will only be a choice of how much and what type of pain. The US, Europe, and Japan are entering Muddle Through World. The rest of the world is faced with increased volatility. This is a tough environment in which to be a central banker.

New York, "Chicago," and Wedding Showers

It looks like I am going to have to go to New York and Philadelphia the first week of July for a day of meetings with partners. Larry Kudlow has asked me to come on his show July 1, and that sounds like fun. And then I am looking forward to the annual Maine fishing trip hosted by David Kotok of Cumberland Partners. A lot of good friends will be there. And I get to go with my youngest son Trey, who always catches more fish than I do. Maybe this year I can manage to at least stay competitive.

Tomorrow is Tiffani's wedding shower, and it looks like there will be a lot of friends at my home. Her wedding is August 8, and it gets closer every day. There is so much that has to be done. While I am not doing any of the heavy lifting, I am amazed at how much the coordination resembles the Normandy invasion.

I will be speaking at the National Association of Business Economists at the Dallas Fed this next Wednesday, on the assigned topic of how I use earnings forecasts in my economic analysis. That portends to be a very contrarian speech, as long-time readers know my view of the value of stock analysts and the reliability of their forecasts.

On a very sad note, I am distressed to learn that Tim Russert passed away. I have thoroughly enjoyed his analysis and interviews over the years. He has been like an old friend coming into my home each week, and I will miss him. Rest in Peace.

On a lighter note, this Sunday evening The Doobie Brothers and Chicago are in town for a concert, and I am going to go for a little nostalgic evening. Can you believe it has been almost 40 years? Where has the time gone?

Let me say thanks to Pierre and Guy Casgraine, who hosted your humble analyst, Martin Barnes and Dennis Gartman, and a few friends in Montreal on Wednesday. It was an exceptionally fine evening. I so enjoy good food and wine and great friends and conversation. It is one of the true pleasures of life.

Enjoy your week, as I know I will. And look for a major announcement from me this Tuesday, as Tiffani and I need your help on a new project. (No, not the wedding!)

Your getting ready to be an old rocker for a weekend analyst,