Bespoke: British pound crumbles

"The US dollar is clearly back in rally mode after suffering a setback in December. As shown in the first chart below, the Dollar Index has now broken well above its 50-day moving average and appears to be heading back to its November highs. Unfortunately, rallies in the dollar have recently coincided with declines in riskier assets like equities.

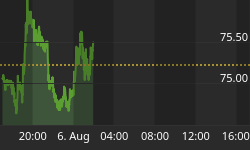

"But the bigger news in currencies is the dramatic fall that the British pound has recently experienced. Today the pound is suffering another big drop, and as shown in the first chart below, the currency broke below recent support levels as well as the $1.40 mark. And the bottom chart shows just how much the pound has fallen in such a short period of time. In late 2007, the pound was trading at record highs versus the US dollar. Now it is trading very close to its lowest level since 1991. Anyone in the US that has the money to go to England can stay there on the cheapest tab in decades."

Source: Bespoke, January 20, 2009.

Eoin Treacy (Fullermoney): Testing times for euro

"All countries in the Eurozone are now seeing their government bond spreads widen relative to German yields. This is an indication that all countries took part in the access to abundant credit made possible by the launch of the Euro and are now suffering the consequences.

"Some are being more affected than others. Spreads for Spain, Greece, Italy and Ireland have expanded most. These were some of the countries where borrowing costs had fallen most in order to join the Euro and where most use was made of the ability to access cheap credit. Without the single currency they would never have been able to borrow at such low rates, but they are now constricted by being unable to devalue their currencies in order to help them through the crisis.

"This is the first real test for the single currency. If it can survive the credit / solvency crisis without seeing some countries dropping out or its efficacy being called into question; then it stands a good chance of surviving for the longer-term as a viable entity. This may well depend on how long the crisis drags on.

"Spreads of more than 250 basis points over Bunds, for Greek government bonds are not encouraging for its long-term participation. Investors will no doubt remember there were significant questions about the Greek government's financial probity in the figures submitted to the European Commission prior to its entry into the single currency. Time will tell, but it will be a worthwhile exercise to monitor these spreads going forward.

"It is also interesting to see that in the UK, where control of interest rates is maintained by the BOE, that the brunt of the country's risk reassessment has been borne by the pound rather than government bonds. The spread over Bunds has been in a volatile downtrend since late 2005 and tested parity recently. The government bond spread has been contracting in line with the pound's decline against the Euro; both appear to have turned around the same time."

Source: Eoin Treacy, Fullermoney, January 19, 2009.

CEP News: Treasury Secretary Geithner takes hardline stance on China

"In tune with the 'change' mantra heard throughout the US Presidential campaign, the Obama administration signalled a new stance on China. But given the economic climate, analysts question the strategy of adopting a hardline position with the biggest purchaser of US debt.

"In comments to the Senate Finance Committee released Thursday, newly-confirmed Treasury Secretary Timothy Geithner said, 'President Obama - backed by the conclusions of a broad range of economists - believes that China is manipulating its currency.' He added later that Obama will aggressively push the Asian country to change its policies on foreign exchange.

"'The comments from the new administration suggest a more robust position on China than the former administration,' said Shaun Osborne, chief currency strategist at TD Securities. 'It remains to be seen what China's response will be, but the US is in a very delicate position at the moment.'

"In September, China overtook Japan as the largest foreign holder of US debt, but that appetite may shrink as China's growth has slowed dramatically in the global recession."

Source: Patrick McGee, CEP News, January 22, 2009.

John Authers (Financial Times): Currency interventions looming

"Unprecendented shifts in forex markets last year is fueling rumors of currency interventions in the coming weeks."

Click here for the article.

Source: John Authers, Financial Times, January 22, 2009.

US Global Investors: Rosenberg - the case for gold

"Gold was, of course, one of the investment world's few bright spots in 2008, and after a slow start in 2009, it began a rally that climbed above $900 an ounce on Friday. This is gold's highest price since early October.

"David Rosenberg at Merrill Lynch sent out a short but useful research note Friday titled 'The Case for Gold' that explains that gold's value is enhanced by declining bullion supply and increasing money supply.

"'It's the only currency not going up in supply. Pretty simple. South African gold output declined 14% last year in the steepest decline since 1901. US production was down 2%. The leading producer in terms of growth last year was China at +3% (and global central bank selling activity dropped 42% in 2008 to 279+ tons, the lowest since 1996).

"'Meanwhile, money supply is up more than 10% YoY in the USA (M2); +16% in Australia (M3); almost 11% in Germany (M2); 18% in the UK (M2); almost 9% in Italy (M2); 13% in Canada (M2); 14% in Korea (M2); 18% in India (M2); 12% in Singapore; and 18% in China (M2).

"'Outside of gold, the only country where money is not being poured into the financial system as if it was water from the tap is Japan, where trends in the monetary aggregates are flat-to-negative. Be that as it may, and in view of all the problems in the US banking sector, we think the dollar is unlikely to lose its reserve currency status any time soon ... Confidence in the ability of European governments to service their sovereign debt is being called into question in the debt markets ('in the land of the blind ...' ).'"

Source: US Global Investors - Weekly Investor Alert, January 23, 2009.

Richard Russell (Dow Theory Letters): Gold - very bullish action

"During the great gold bull markets of the 1970s to 1980, gold topped out at a price of 850 per ounce. For months now, gold has been 'testing' the 850 level, first rallying above 850 and then sliding below 850. Currently, February gold is trading at 891. I consider this to be very bullish action. The current gold action is taking place in the second phase of the new gold bull market. The second phase has seen many hedge funds and a small segments of the public become interested in gold.

"I believe the third speculative phase of the current gold bull market lies ahead. This is the phase where the public jumps wholesale into the market. It's the phase where I expect to see a much higher, even frenzied, gold price. This final phase of the gold bull market will be accompanied by international doubt regarding the value and viability of fiat currency.

"Fiat money is being created in great quantities by almost every central bank in the world. Imagine, the foolishness of trying to ward off insolvency by creating ever-larger quantities of paper money. The worse off the economies of the world, the more fiat currency will be created."

Source: Richard Russell, Dow Theory Letters, January 23, 2009.

Financial Times: UK move to boost cash supply

"Britain paved the way towards unconventional monetary policy in Europe on Monday when the government gave the Bank of England authority to create money and buy a variety of private sector assets.

"Although there is no sign the Bank's monetary policy committee wants to introduce US-style quantitative easing immediately, it now has the power to buy assets ranging from corporate bonds to asset-backed securities with newly created money.

"The policy, if introduced, seeks to ease the flow of finance to companies, driving down company borrowing costs and boosting the supply of cash in the economy. The Federal Reserve prefers the term 'credit easing' to describe similar moves.

"The decision comes as part of a package designed to ease pressure on lending in the UK economy and put a brake on deepening recession. On Monday, the European Commission said Britain had one of the most exposed economies in the world to the global recession, predicting its economy would contract by 2.8% this year with stagnation continuing in 2010.

"Other elements of the package were heavily trailed. An insurance scheme stands at its heart, designed to restore some certainty to banks' finances by providing cover against catastrophic losses. This will be implemented from February on a case-by-case basis.

"From April, the government will provide guarantees to wrap around simple asset-backed securities issued by banks containing high-quality mortgage and corporate assets. Subject to state aid approval from the European Commission, it is also planning to extend its current guarantee of short-term funding for banks to the end of the year.

"For the first time since the crisis began, the Bank of England will also explicitly accept corporate credit risk when it begins a $74 billion programme of asset purchases from the private sector in return for government paper in February."

Source: Chris Giles, Financial Times, January 19, 2009.

Financial Times: UK tries to break recessionary dynamic

"The government on Monday launched its second bank rescue package, injecting billions of pounds more of the taxpayer's money into saving Britain's banks. Chris Giles, FT's economics editor, tells Daniel Garrahan that the new bank rescue package is designed to rescue the economy as well as the banks."

Source: Financial Times, January 19, 2009.

BCA Research: Last chance for UK banks

"Measures by UK authorities to shore up the banking system brings the prospect of full scale nationalization one step closer if they fail to re-ignite lending.

"The BoE's ability to purchase assets outright will effectively help in recapitalizing the banking system and should also provide a valuable fillip to the corporate debt market. For now, the Treasury has stopped short of setting up a 'bad bank' to coral all the poor quality assets, probably for fear of what this might mean for the UK's beleaguered public finances in the event of default. Based on current government estimates the deficit will stay above 3% of GDP until the middle of the next decade.

"Bottom line: At this stage, policymakers are limiting their actions to 'quality assets'. However, it is probable that the next step is a 'bad bank' and full scale nationalization, given that output is forecast to fall this year at the fastest pace since 1946 and lending is likely to stay weak for a prolonged period."

Source: BCA Research, January 21, 2009.

James Pressler (Northern Trust): Japan - no sale!

"Two items of significance regarding the Japanese market hit the wire this morning - the end-year trade balance and the Bank of Japan (BoJ) policy meeting announcement. With the overnight call rate already down to 0.10%, another rate cut would hardly be a news-maker, but the state of Japan's exports usually makes the front page. And unfortunately, the news was not good.

"Nobody expected the export market to make a miraculous turnaround, but some hope existed for less erosion in overseas sales or fewer imports, thereby supporting net exports. Neither occurred. December imports contracted by 21.5% on the year and were up by 7.9% for 2008 as a whole, but exports fared much worse, posting respective changes of -35.0% and -3.4%. This dragged the annual trade balance down to $20.4 billion, a level not seen since 1983 and a far cry from the 2007 tally of $92.1 billion.

"We have said it before and we will say it again - our official forecast for Q4 GDP in Japan is 'abysmal'."

Source: James Pressler, Northern Trust - Daily Global Commentary, January 22, 2009.

Societe Generale: Japanese exports fall 35%

"Strikingly, Japanese exports to the US were down some 37% yoy. But we cannot highlight strongly enough how truly mindboggling Japan's collapse in exports to China are. Last July they were expanding at a 16% yoy pace. Now they are contracting at a 35% yoy rate! This is a phenomenon throughout the region. Hence despite the notoriously manipulated Chinese GDP data showing a shocking slowdown in GDP growth to 6.8% yoy. I would eat my hat if the Chinese economy was doing anything other than contracting right now."

Source: Societe Generale, January 2009.

Nouriel Roubini (RGE Monitor): China - why 0% growth is the new size 6.8%

"The Chinese came out today with their 6.8% estimate of Q4 2008 growth. China publishes its quarterly GDP figure on a year over year basis, differently from the US and most other countries that publish their GDP growth figure on a quarter on quarter annualized seasonally adjusted (SAAR) basis.

"When growth is slowing down sharply the Chinese way to measure GDP is highly misleading as quarter on quarter growth may be negative while the year over year figure is positive and high because of the momentum of the previous quarters' positive growth.

"Indeed if one were to convert the 6.8% y-o-y figure in the more standard quarter over quarter annualized figure Chinese growth in Q4 would be close to zero if not negative.

"Other data confirm that China was in a borderline recession in Q4 and that it may be in an outright recession in Q1: production of electricity plunged 7.9% in y-o-y basis; the Chinese PMI has been below 50 and close to 40 for five months now.

"And with manufacturing being about 40% of GDP , manufacturing is certainly in a sharp recession (negative growth) and the overall economy may be close to a recession

"So the 6.8% growth was actually a 0% growth - or possibly negative growth - in Q4; and the Q1 figures look even worse. So China is in a recession regardless of what the highly massaged official numbers claim."

Source: Nouriel Roubini, RGE Monitor, January 22, 2009.

Bryan Crowe (Northern Trust): Brazil - 100 is the new 75

"In a surprise to the majority of forecasters, Brazil's central bank lowered its benchmark rate by a larger-than-expected 100bps on Wednesday after an official vote of 5-3 (the three voted for a 75 bp cut), bringing the overnight Selic rate down to 12.75%. This move was justified after a subdued inflation reading for December, but the committee's main reason for the move was a significant deterioration in domestic conditions."

Source: Bryan Crowe, Northern Trust - Daily Global Commentary, January 22, 2009.

Did you enjoy this post? If so, click here to subscribe to updates to Investment Postcards from Cape Town by e-mail.