Last month in a Boston foreclosure sale, John Hancock Tower Lenders Took, a 65% Haircut In 3 Years . Boston is back in the news today with another foreclosure auction. This time it's condo related, with Chorus Bank in the thick of things.

Please consider 441 Stuart Street: What Happened?

This week, the building at 441 Stuart Street was offered to the public through a foreclosure auction. The property was most recently purchased in 2004 for $37.5MM with the intent of converting the building to condominiums.

Recorded documents show that Corus Bank, a well-known condo conversion lender out of Chicago, placed $42MM in debt on the property in 2004.

The auctioner opened at $30MM and asked if there were any bids. There were not. Next he cut the bid in half and asked for $15MM, and the bids that followed were $15.1MM, $16MM, $16.1MM, and finally $17MM. There was only one 3rd party who bid the $15.1 and $16.1 against the bank. The lender bought the property back at $17MM.

Nevermind the fact that the highest 3rd party bid for the property was less than 40% of the known debt, consider the fact that the number represents only about $100/foot. Remember that this property is in Copley Square. If retail prices for completed condos are $600-900/SF and construction costs run $150-250 per foot then that's a margin of 40% or better - isn't it?

It's interesting that no one wants this building at $100 a square foot with completed condos going for $600 to $900 a square foot.

Corus Bankshares Receives 'Going Concern' Qualification

In Bank Watch (Apr. 12-18): CoStar is reporting Corus Bankshares Receives 'Going Concern' Qualification.

Corus Bankshares Inc. in Chicago announced that its audited financial statements for the year ended 2008 contained a 'going concern' qualification from its independent registered accounting firm Ernst & Young LLP.

Corus, with a portfolio consisting primarily of condominium construction loans, many in the hard hit areas of Arizona, Nevada, south Florida and Southern California, has seen a rapid and precipitous decline in the value of the collateral securing its loan portfolio. Thus, it is experiencing significant loan quality issues.

The net loss of $456.5 million it recorded in 2008 was primarily the result of significant increases in the provision for credit losses.

The company said its board of directors has formed a strategic planning committee to seek all strategic alternatives, including a capital investment, a sale, a strategic merger or some form of restructuring.

The company also reported that there are additional concerns that regulators may take other actions, including placing the bank into conservatorship or receivership.

Here are a few snips of other Banks in the CoStar Article.

Community Bancorp Feeling Heat of Declining Desert Area Real Estate

Community Bancorp, the Las Vegas-based holding company for Community Bank of Nevada and Community Bank of Arizona, is late filing its annual report for 2008 with the U.S. Securities & Exchange Commission.

Community Bancorp said it expects that it will report a loss for the year compared to net income of $20.4 million for a year earlier.

As a result of these losses, the company expects that federal and state regulators will require a formal agreement with respect to, among other things, asset quality, capital and earnings.

Preferred Bank Hit By Declining San Diego Property Values

Preferred Bank, an independent Los Angeles-based commercial bank focusing on the Chinese-American and diversified Southern California market, reported an additional revision to results for the quarter and year ended Dec. 31, 2008, due to the receipt of an appraisal on an impaired construction loan.

The March "appraisal indicates a value deterioration far beyond our estimation for that area and far in excess of published market statistics for that market area," said Li Yu, chairman and president of Preferred Bank.

Union Center National Bank Takes Back Warehouse Project

Union Center National Bank in Union, NJ, announced that for the first quarter of 2009, it intends to establish a loan loss provision of $1.4 million, which covers a charge-off of approximately $900,000 in connection with a $4.9 million commercial real estate construction project of industrial warehouses. It had recently downgraded the loan to non-accrual status and increased its level for loan loss allowance by $521,000.

"At March 31, 2009, the corporation expects non-performing assets to amount to $9.1 million -- up from $4.7 million at Dec. 31, 2008," said Anthony Weagley, president and CEO of the bank's holding company, Center Bancorp Inc.

The bank's other real estate owned will increase to $4.4 million, with the other asset being a residential condominium project that was taken back in the fourth quarter of 2008. The bank holding company is near completion of that project and has elected to begin to rent the units.

Expect to see more banks completing projects and electing to rent units as the recession wears on. Ironically, you can also expect to see the opposite extreme whereby banks acquiring real estate in foreclosure processes and tear it down because they do not want to become rental agents. For an interesting video of teardowns of brand new homes please see Extreme Home Makeover Depression Edition II.

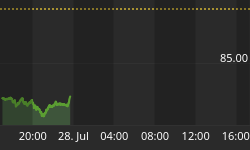

Meanwhile, it's just a matter of time for Chorus Bank (CORS) heads into receivership. It was trading at $28 in April of 2006 and you can be a proud owner today at 31 cents.