"Whenever, therefore, people are deceived and form opinions wide of the truth, it is clear that the error has slid into their minds through the medium of certain resemblances to that truth." ~ Socrates BC 469-399, Greek Philosopher of Athens

http://www.shadowstats.com/alternate_data/money-supply

Inflation is defined as an increase in the money supply and not as many economists falsely refer to it as an increase in the cost of goods. The price increase is a direct result of inflation, but it is not the definition but just a symptom of inflation. If one looks at the above two charts one immediately spots how dramatically the money supply has risen in the last 12 months. In less than 12 months the money supply has risen to a level that is double that of 2003. M1 is increasing at levels not seen for over 40 years; take a moment to digest this fact, when the economy is broken, when savings are low, when companies are scaling back, we have drug addicts driving the printing press to the breaking point. 1+ 1 always equal two and pushing the printing press into over drive must equate to some form of very strong inflation and most likely hyperinflation.

History clearly indicates that when the money supply increases, inflationary forces increase and the more dramatic the increase the more profound the inflationary effects are. It goes without saying that the current rate of expansion is basically illustrating that hyperinflation is moving closer to a reality with the passage of each day.

Note that the current administration has many ambitious plans, improve funding for Medicare, improve social security, provide universal health coverage, improve the infra structure, increase troop levels in Afghanistan, the future money this administration will be forced to lend banks once the commercial mortgage sector starts to crumble, etc. All these programs need extra money, money this country does not have and the only way to create this extra money is to print it as no nation is going to lend this country the trillions of dollars it will need to fund all these ventures. It, therefore, goes without saying that, unless this administration dramatically cuts down on spending or increases taxes by a back breaking amount, inflation and then hyperinflation are going to hit this economy soon.

Now in the not so distant past, the world at large was busy proclaiming that the US economy no longer had as much as an impact on the rest of the world's economies as it once used to. Well, that myth has come to an end; when the US housing market tanked and the credit markets froze, the rest of world crumbled also. Thus the old saying still applies, when the US sneezes the rest of the world catches a flu and in some cases bronchitis or Pneumonia. Thus whatever happens here will have a global effect and other nations are not going to be able to come out and say that it's different this time, for the reality is that it's not.

For a long time individuals in the Euro zone assumed that they were better off, the reality is that the situation is a lot more troubling in the Euro zone than it is in the US. Several of the countries that make up this zone are in deep trouble so the long term prospects for this zone are not very bright at least not for the next few years. The question now comes down to which location is less ugly for most nations are in deep trouble. It is for this reason we are strongly advocating commodities based investments for regardless of the currency they trade in, we expect them to trade significantly higher in the years to come. If we had to choose between the EURO and the Dollar, we would not, but instead deploy our money into the following currencies, the Canadian Dollar, the Hong Kong Dollar, the Chinese Yuan (probably the main one) and maybe the Australian Dollar. Those looking to invest in currencies should spread their money in at least 2-3 of the above currencies. Note we are strictly speaking in terms of investing in currencies directly or via currency ETF's and not the futures market. Believe it or not inflation and hyperinflation provide incredible opportunities to make even more money in the stock and Futures markets provided one holds the right investments and usually a good advisory service is required to help with timing of such transactions. Assets always over inflate to compensate for inflationary pressures, so if the dollar were to lose say 20%, certain based commodities assets could increase in value anywhere from 60%-100% if not higher.

As we have stated before, the next 6-9 years are going to produce profound changes, these changes will be so extreme and deep that it will literally stun the unprepared, for the majority have not and will most likely never again be exposed to such dramatic forces again in their life times. Hyperinflation means that you go out today to buy a loaf for 3 dollars and when you come back tomorrow the cost has risen to 4 or 5 dollars. We had a brief taste of this last year when petrol prices kept increasing on a weekly basis.

We would therefore, once again strongly advise all our subscribers to eliminate all debt, live 1-2 standard below your means and use a large percentage of this money saved to purchase bullion and commodities based stocks; buy during strong pull backs and or corrections. The time to prepare is when the sun is shinning, for once it starts to rain it's usually too late.

Not all the currencies we mentioned have ETF'S and so one could invest directly in them by opening a bank account (a offshore account that allows you to invest in a basket of currencies) or one could choose from the following ETF'S

Canadian Dollar= FXC | Australian dollar= FXA |

A wild speculative play would be the Russian Ruble

Russian Ruble= XRU

Other means to hedge oneself against the side effects of inflation is to deploy money into commodities and the following commodity based ETF's would and should perform well in an inflationary and hyper inflationary environment.

Oil= USO | Gold= GDX | Silver= SLV | ||

Natural gas= UNG | Gold miners= GDX | |||

Dollar

The Chinese by nature are very respectful when addressed by leaders and therefore, what occurred a few weeks ago when Treasury secretary Geithner addressed the students at the prestigious Peking university is very telling.

"Chinese assets are very safe," Geithner said in response to a question after a speech at Peking University, where he studied Chinese as a student in the 1980s.

His answer drew loud laughter from his student audience, reflecting scepticism in China about the wisdom of a developing country accumulating a vast stockpile of foreign reserves instead of spending the money to raise living standards at home. Full story

The fact that these students laughed loudly clearly indicates that the Chinese have no faith that the US government is concerned with preserving the value of the dollar. As of March China had 786 billion dollars invested in treasuries. As we have repeatedly stated in the past Chinese are very advanced chess players and what makes them even more formidable is their capacity to be extremely patient. China basically controls the US now, those that control the strings of the purse control the nation. If china threatens to sell its treasury holdings it would literally break the bond market and drive interest rates to record levels in a matter of days.

While the above story is a good measure of the dollars' long term demise, it is not accurate in terms of its short to intermediate term direction. There is a very good chance that the dollar could actually go on to test its 2008 Oct-Nov highs, and possibly even put in a new high. The testing of its old highs will mark the beginning of the end for the dollar; from there it could lose up to 60% of its value before it stabilises, which means commodity prices will literally explode across the board.

However, for this short term scenario to remain valid the dollar cannot trade below 78 for more than 3-4 days in a row; if it does then the chances of it rallying to new highs will have diminished significantly. The dollar traded as low as 78.35 and then immediately rallied from these levels; this is a good initial sign for it shows that the 78 price point level is a zone of strong support. The rally we are expecting in the dollar coincides very nicely with the rally that is set to occur in the bond markets; when individuals purchase bonds, they are indirectly opening up long positions in the dollar (in other words, other words they are buying the dollar). As with the bond market we are expecting the dollar to put in its final high in the next 6-12 months and then embark on a long down trend that could result in a total loss of up to 60% of its former value.

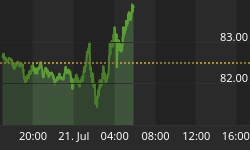

As long as the Dollar does not close below 78 for more than 3 days in a row the outlook will remain bullish; ideally, it should not trade below its June lows of 78.35. It initially mounted a rally but then shed most of those gains and is now attempting to rally again. It needs to trade past 82.50 for roughly 3 days in a row and penetrate down trend line in the 1 year chart; a break past this level for 3 days in a row should be enough to propel the dollar all the way to the 85.50-86.00 ranges. If the dollar breaks below 78.00 the next target becomes 74, and it will also suggest that the downward slide in the dollar is occurring at a faster rate than was initially projected. The current pattern calls for a rally that should lead to a test of its recent highs or potentially to new 52 week high before it embarks on a long downward journey.

The 2 year chart confirms the outlook of the 1 year chart. To move higher the dollar needs to trade past its main down trend line, which falls roughly in the 82.50-83.00 ranges, and a break below 78 would take it at the very least down to the 74 ranges. In the 2 year chart, we notice how important the 78 price point level is; it's a zone of support that stretches back almost 2 years and thus a break below this level would be a very decisive move.

The dollar still has time to move higher and the action in the bond markets is suggesting that it should move higher as the bond markets appear to have put in an intermediate bottom that could result in them rallying for up to 9 months and thus a rally in the bond markets should drive the dollar higher.

We are not expecting the dollar to mount another long term rally; this rally will be the last strong rally for sometime to come. Once this rally is over (current targets are now in the 88-90 ranges, but it could rally as high as 92), we expect the dollar to resume its long term down trend and shed up to 60% of its value. As long as the dollar can remain above 78 the picture will remain somewhat bullish, a close above 82.50 for 3 days in a row or a weekly close above 83 will turn the hourly, daily, and maybe even the weekly trends bullish.

One rather strong bullish factor for the dollar is the fact that when it traded to new 6 moth lows, gold did not respond by trading to new highs; this is a rather strong intra market negative divergence signal and usually such signals indicate that the weaker market (in this instance the weaker market is the dollar) is going to mount a rally.

Risk takers could deploy funds into the dollar now with the intention of closing these positions out the moment the dollar tests its old highs and then redeploying this money back into their original currencies. There are many ways to take advantage of this situation, the riskier ones will yield significantly higher returns but the simplest strategy would be to purchase shares in the ETF UUP.

The current pattern indicates that the Dollar could trade to the 90-92 ranges; this represents roughly a 15% gain from current levels; in currency markets such moves are considered massive.

"'Tis but an hour ago since it was nine, and after one hour more twill be eleven. And so from hour to hour we ripe and ripe, and then from hour to hour we rot and rot. and thereby hangs a tale." ~ William Shakespeare 1564-1616, British Poet, Playwright, Actor