The good news is:

• All of the major indices closed at multi month highs last week.

Short Term

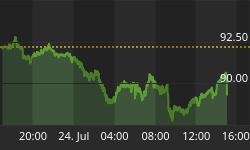

The market action that I interpreted as a blow off a week ago continued last week.

Prior to the early 1990's companies incubated on the NASDAQ and, when they were large enough, moved to the NYSE. Prior to the early 1990's the NASDAQ composite (OTC) was a small cap index similar to the Russell 2000 (R2K). In the early 1990's several large tech companies elected to remain with the NASDAQ. Since the OTC is a capitalization weighted index it became a large cap tech index.

The OTC finished a run of 12 consecutive up days last Thursday, an accomplishment seen only one other time since 1990.

The previous string of 12 or more consecutive up days for the OTC occurred in January 1992 and is shown in the chart below.

The chart shows 100 trading days with the OTC in blue and an indicator showing the percentage of the previous 12 trading days that were up in black. Dashed vertical lines have been drawn on the 1st trading day of each month.

The market peaked about a month later.

A single previous example is not something we can draw conclusions from, we are in uncharted territory.

Intermediate term

Usually volume increases as prices rise.

Volume picked up on the NASDAQ last week, but not on the NYSE.

All of the charts below cover the last 100 trading days which takes them back to the March lows.

The 1st chart shows the OTC in blue and a 5% trend (39 day EMA) of NASDAQ volume of advancing issues in green.

This chart is pretty close to what you would expect.

The next chart shows the OTC in blue and a 5% trend on NASDQ total volume in orange. Volume recovered last week after hitting its lowest level for the period.

The charts for the NYSE are not as pretty as those for the NASDQ.

The next chart shows the S&P 500 (SPX) in red and a 5% trend of NYSE volume of advancing issues (NY UV) in green.

There was a very modest increase in NY UV last week.

The last chart shows the SPX in red and a 5% trend of NYSE total volume in black. There has been no appreciable increase in NYSE volume in the past 2 weeks.

You would expect a run up like we have seen in the past 2 weeks to be caused by an avalanche of buyers, increasing volume. That has not been the case.

Seasonality

Next week includes the last 5 trading days of July during the 1st year of the Presidential Cycle.

The tables show the daily return on a percentage basis for the last 5 trading days of July during the 1st year of the Presidential Cycle. OTC data covers the period from 1963 - 2008 and SPX data from 1928 - 2008. There are summaries for both the 1st year of the Presidential Cycle and all years combined.

By all measures the coming week has been modestly positive.

The average return for the OTC over all years is slightly negative, brought down by huge losses in 1969, 1974 and 2000.

Last 5 days of July.

The number following the year represents its position in the presidential cycle.

The number following the daily return represents the day of the week;

1 = Monday, 2 = Tuesday etc.

| OTC Presidential Year 1 | ||||||

| Day5 | Day4 | Day3 | Day2 | Day1 | Totals | |

| 1965-1 | 0.66% 1 | 0.08% 2 | -0.17% 3 | 0.13% 4 | 0.74% 5 | 1.43% |

| 1969-1 | -0.13% 5 | -1.39% 1 | -1.63% 2 | -1.33% 3 | -0.58% 4 | -5.06% |

| 1973-1 | 0.83% 3 | -0.02% 4 | 0.17% 5 | -0.44% 1 | -0.22% 2 | 0.33% |

| 1977-1 | -0.10% 1 | -0.59% 2 | -1.12% 3 | -0.56% 4 | -0.03% 5 | -2.40% |

| 1981-1 | 0.68% 1 | -0.24% 2 | 0.02% 3 | 0.52% 4 | 0.76% 5 | 1.74% |

| 1985-1 | 0.24% 4 | 0.06% 5 | -1.21% 1 | -0.12% 2 | 0.23% 3 | -0.79% |

| Avg | 0.30% | -0.44% | -0.75% | -0.39% | 0.03% | -1.24% |

| 1989-1 | 0.11% 2 | 0.59% 3 | 0.75% 4 | 0.08% 5 | 0.23% 1 | 1.75% |

| 1993-1 | 0.61% 1 | -0.50% 2 | 0.65% 3 | 0.23% 4 | -0.36% 5 | 0.64% |

| 1997-1 | 0.03% 5 | -0.39% 1 | 0.56% 2 | 1.00% 3 | 0.36% 4 | 1.57% |

| 2001-1 | 1.28% 3 | 1.95% 4 | 0.30% 5 | -0.55% 1 | 0.46% 2 | 3.44% |

| 2005-1 | -0.60% 1 | 0.43% 2 | 0.47% 3 | 0.56% 4 | -0.62% 5 | 0.24% |

| Avg | 0.29% | 0.42% | 0.55% | 0.26% | 0.01% | 1.53% |

| OTC summary for Presidential Year 1 1965 - 2005 | ||||||

| Averages | 0.33% | 0.00% | -0.11% | -0.04% | 0.09% | 0.26% |

| % Winners | 73% | 45% | 64% | 55% | 55% | 73% |

| MDD 7/31/1969 4.97% -- 7/29/1977 2.39% -- 7/30/1985 1.32% | ||||||

| OTC summary for all years 1963 - 2008 | ||||||

| Averages | 0.02% | -0.01% | -0.08% | -0.02% | 0.00% | -0.09% |

| % Winners | 54% | 46% | 48% | 61% | 52% | 59% |

| MDD 7/28/2000 9.10% -- 7/31/1974 6.22% -- 7/31/1969 4.97% | ||||||

| SPX Presidential Year 1 | ||||||

| Day5 | Day4 | Day3 | Day2 | Day1 | Totals | |

| 1929-1 | -0.38% 5 | -0.38% 6 | -1.30% 1 | 1.14% 2 | 1.33% 3 | 0.41% |

| 1933-1 | -1.71% 2 | 2.62% 3 | 0.85% 4 | -2.34% 5 | -4.60% 1 | -5.19% |

| 1937-1 | -0.12% 2 | -1.53% 3 | -0.36% 4 | 0.30% 5 | 1.25% 6 | -0.45% |

| 1941-1 | 0.48% 6 | 0.77% 1 | -0.19% 2 | -0.48% 3 | -0.10% 4 | 0.49% |

| 1945-1 | 0.96% 3 | -2.04% 4 | 0.49% 5 | 1.04% 1 | 0.41% 2 | 0.86% |

| Avg | -0.15% | -0.11% | -0.10% | -0.07% | -0.34% | -0.78% |

| 1949-1 | 0.34% 1 | 0.80% 2 | 0.00% 3 | -0.13% 4 | 0.00% 5 | 1.01% |

| 1953-1 | -0.66% 1 | 0.17% 2 | 0.62% 3 | 0.95% 4 | 1.06% 5 | 2.14% |

| 1957-1 | 0.00% 4 | -0.33% 5 | -1.09% 1 | 0.00% 2 | -0.02% 3 | -1.44% |

| 1961-1 | 0.55% 2 | 0.94% 3 | 1.17% 4 | 0.15% 5 | 0.07% 1 | 2.88% |

| 1965-1 | -0.02% 1 | -0.21% 2 | 0.19% 3 | 0.77% 4 | 0.67% 5 | 1.40% |

| Avg | 0.04% | 0.27% | 0.18% | 0.35% | 0.36% | 1.20% |

| 1969-1 | -0.91% 5 | -1.90% 1 | -0.81% 2 | 0.50% 3 | 2.11% 4 | -1.00% |

| 1973-1 | 1.39% 3 | 0.19% 4 | -0.24% 5 | -0.31% 1 | -0.94% 2 | 0.09% |

| 1977-1 | -0.81% 1 | -0.58% 2 | -1.63% 3 | 0.15% 4 | 0.06% 5 | -2.79% |

| 1981-1 | 1.12% 1 | -0.59% 2 | 0.02% 3 | 0.66% 4 | 0.70% 5 | 1.91% |

| 1985-1 | 0.25% 4 | 0.18% 5 | -1.46% 1 | 0.17% 2 | 0.52% 3 | -0.33% |

| Avg | 0.21% | -0.54% | -0.82% | 0.24% | 0.49% | -0.43% |

| 1989-1 | 0.06% 2 | 1.25% 3 | 1.17% 4 | 0.05% 5 | 1.15% 1 | 3.67% |

| 1993-1 | 0.45% 1 | -0.19% 2 | -0.23% 3 | 0.68% 4 | -0.47% 5 | 0.23% |

| 1997-1 | -0.16% 5 | -0.25% 1 | 0.62% 2 | 1.06% 3 | 0.21% 4 | 1.49% |

| 2001-1 | 1.61% 3 | 1.04% 4 | 0.24% 5 | -0.11% 1 | 0.56% 2 | 3.34% |

| 2005-1 | -0.38% 1 | 0.17% 2 | 0.46% 3 | 0.56% 4 | -0.77% 5 | 0.05% |

| Avg | 0.32% | 0.41% | 0.45% | 0.45% | 0.14% | 1.76% |

| SPX summary for Presidential Year 1 1929 - 2005 | ||||||

| Averages | 0.10% | 0.01% | -0.07% | 0.24% | 0.16% | 0.44% |

| % Winners | 50% | 50% | 50% | 70% | 65% | 70% |

| MDD 7/31/1933 6.84% -- 7/29/1969 3.58% -- 7/27/1977 2.98% | ||||||

| SPX summary for all years 1928 - 2008 | ||||||

| Averages | -0.05% | 0.01% | 0.11% | 0.15% | 0.09% | 0.31% |

| % Winners | 56% | 58% | 54% | 63% | 63% | 58% |

| MDD 7/26/1934 7.83% -- 7/31/1933 6.84% -- 7/31/1974 6.68% | ||||||

Money supply (M2)

The money supply chart was provided by Gordon Harms. Money supply growth continued to deteriorate last week.

Conclusion

Last week confirmed the old adage "Don't short a dull market". As an initiation of a new leg up the past two weeks have left something to be desired, volume. I think it is likely to continue higher because, right now, no one wants to sell it.

I expect the major indices to be higher on Friday July 31 than they were on Friday July 24.

This report is free to anyone who wants it, so please tell your friends. They can sign up at: http://alphaim.net/signup.html. If it is not for you, reply with REMOVE in the subject line.

Last weeks positive forecast was a miss.

Thank you,