Financial Times: Bernanke explains Fed's new openness

"Ben Bernanke has explained his decision to turn the normally secretive US Federal Reserve into something of an open house, saying his unusually large number of recent public appearances are the result of the 'extraordinary' times the country faces.

"The Fed chairman has turned up at everything from a 60 Minutes television interview to a Kansas City town hall session over the past few weeks, prompting some to wonder if he is trying to ensure he is re-appointed when his four-year term ends in January.

"However, Mr Bernanke said he was answering a clear public need. 'Normally Fed chairmen don't do this kind of thing because we want to avoid causing near-term market volatility as people try to anticipate our next FOMC (Federal Open Markets Committee) meeting, he told the Financial Times this week.

"'But this is an extraordinary period. We want to answer the questions we know people have about what hit them in this economic crisis, what the Fed is doing about it and how we expect economic developments to play out.'

"The Fed's new openness is well timed. This week, as the debate continues over the bank's role in the financial crisis and proposed prudential powers, Gallup showed it is held in lower esteem than the Internal Revenue Service.

"More seriously, there is a populist headwind in Congress among some lawmakers who want to remove the Fed's monetary independence.

"Cynics believe Mr Bernanke is using this public relations outreach to ensure he is reappointed next January. But Mr Bernanke says the goal is to educate the public about what the Fed does at a time when it keeps getting caught in the crossfire over its role in the crisis and its future prudential powers.

"The chairman's personal standing remains high. 'I would be astonished if Ben isn't re-appointed,' says Alice Rivlin, a former vice-chairman of the Fed. 'He has become very good at interacting with people beyond the usual circles and he is good at avoiding traditional Fed-speak.'

Source: Edward Luce, Financial Times, July 30, 2009.

Nouriel Roubini (The New York Times): The Great Preventer

"Last week Ben Bernanke appeared before Congress, setting off a discussion over whether the president should reappoint him as chairman of the Federal Reserve when his term ends next January. Mr. Bernanke deserves to be reappointed. Both the conventional and unconventional decisions made by this scholar of the Great Depression prevented the Great Recession of 2008-2009 from turning into the Great Depression 2.0.

"Mr. Bernanke understands that in the Great Depression, the collapse of the money supply and the lack of monetary stimulus during contractions worsened the country's economic free fall. This lesson has paid off. Mr. Bernanke's decision to keep interest rates low and encourage lending has, for now, averted the L-shaped near depression that seemed highly likely after the financial collapse last fall.

"To be sure, an endorsement of Mr. Bernanke's reappointment comes with many caveats. Mr. Bernanke, a Fed governor in the early part of this decade, supported flawed policies when Alan Greenspan pushed the federal funds rate (the policy rate set by the Fed as its main tool of monetary policy) too low for too long and failed to monitor mortgage lending properly, thus creating the housing and credit and mortgage bubbles.

"He and the Fed made three major mistakes when the subprime mortgage crisis began. First, he kept arguing that the housing recession would bottom out soon (it has not bottomed out even three years later). Second, he argued that the subprime problem was a contained problem when in reality it was a symptom of the biggest leverage and credit bubble in American history. Third, he argued that the collapse in the housing market would not lead to a recession, even though about one-third of jobs created in the latest economic recovery were directly or indirectly related to housing.

"Mr. Bernanke's analysis was mistaken in several other important ways. He argued that monetary policy should not be used to control asset bubbles. He attributed the large United States current account deficits to a savings glut in China and emerging markets, understating the role that excessive fiscal deficits and debt accumulation by American households and the financial system played.

"Still, when a liquidity and credit crunch emerged in the summer of 2007, Mr. Bernanke engineered a U-turn in Fed policy that prevented the crisis from turning into a near depression. He did this largely with actions and programs that were not in the traditional toolbox of monetary policy.

Click here for the full article.

Source: Nouriel Roubini, The New York Times, July 25, 2009.

Clusterstock: Thank goodness for government spending

"Today's better-than-expected -1% GDP was tempered, somewhat, by the staggering 11% spike in Federal Government spending (hello stimulus!). Today's chart looks back at the Y/Y GDP change with the same number sans government spending. As you can see from the divergence, the government boost provides a big help.

Source: Joe Weisenthal and Kamelia Angelova, Clusterstock - The Business Insider, July 31, 2009.

BCA Research: US GDP - major benchmark revision to growth

"US output net of inventories stabilized in the second quarter, which could foreshadow positive growth in the second half as inventory levels are rebuilt.

"Although the advanced GDP report for the second quarter beat expectations, it also indicated that the 2008 downturn in growth and consumer spending was considerably weaker than previously thought. Gross domestic product contracted by 6.4% (at annual rates) in the first quarter, a much weaker result than the previous estimate of 5.5%. Consumer spending was also revised markedly lower. Interestingly however, real final sales of domestic product - i.e. GDP net of the change in inventory - has stabilized, a fairly positive sign that growth can turn positive in the second half of the year as inventories are rebuilt.

"Bottom line: We expect a gradual recovery in the US economy in the months ahead, but the Fed will need to keep the policy setting extremely aggressive to achieve a self-reinforcing upturn in consumer confidence and spending.

Source: BCA Research, July 31, 2009.

Asha Bangalore (Northern Trust): Jobless claims report makes a case that the labor market is improving

"Initial jobless claims rose 25,000 to 584,000 during the week ended July 25. There were seasonal distortions in the early part of July which have been more or less corrected now. Typically, layoffs at auto companies increase in July for retooling. This year the layoffs occurred in May and June and were related to the GM and Chrysler bankruptcy issues. This shift in layoffs led to lower seasonally adjusted jobless claims in July and the readings we see now are gains after the artificial decline. Despite the increase in initial jobless claims in the past two weeks, the peak in initial jobless claims has occurred in March 2009 (674,000).

"Continuing claims, which lag initial jobless by one week, fell 54,000 to 6.197 million. Continuing claims have declined in four out of the last five weeks.

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, July 30, 2009.

The Wall Street Journal: Consumer-debt picture shows one sign of improvement

"Fewer American households appear to be falling behind on their debt payments, according to a new study, but some economists question whether the data reflect a meaningful easing of consumer-credit problems.

"'I feel very confident we are at a turning point,' said Mark Zandi, chief economist of Moody's Economy.com. 'Household credit conditions are set to improve significantly by this time next year,' he said. Mr. Zandi attributed the turn to tightening lending standards.

"Mr. Zandi's outlook is based largely on his analysis of 7.5 million credit files supplied by Equifax Inc., the credit-reporting titan based in Atlanta. The files analyzed represent 5% of US consumers. The analysis showed that the number of mortgage, credit-card and other consumer loan payments that were 30 and 60 days past due fell by nearly 1.1 million to 13.9 million at the end of June, on a seasonally adjusted basis, from three months earlier. Nearly two-thirds of the decline came from falling credit-card delinquencies.

"The analysis of 'early-stage' delinquencies can be key to spotting changing trends. When such data show a slowing, it could indicate that total delinquencies will come down in the next six to 12 months. But the data don't mean the broader credit problems plaguing banks and other lenders will be eliminated anytime soon.

"In fact, the total number of seriously delinquent borrowers and those in default will keep rising for some time, as borrowers who are 30, 60 and 90 days delinquent move to the next phase of delinquency. Overall, household liabilities in delinquency and default rose to $1.15 trillion in June, 10% of total liabilities, according to Mr. Zandi's analysis of the Equifax data. The delinquency and default rate in June was up from 8.96% in March and 8.01% in December.

"Still, Mr. Zandi said the reduction in newly delinquent borrowers is a positive sign for the economy, especially coming at a time when 'the job market and housing market are still bad and getting worse. Once those markets stabilize, when combined with the tighter underwriting, we will see a dramatic improvement in credit quality.'

"But not all analysts are convinced. Some believe that improvements in the data represent little more than temporary blips that will reverse as a new wave of credit problems emerge.

Source: Ruthe Simon and Constance Mitchell Ford, The Wall Street Journal, July 25, 2009.

Asha Bangalore (Northern Trust): Durable goods orders - decline in airline and defense masks improvement

"Orders of durable goods fell 2.5% in June after a 1.3% increase in May. The 38.5% drop in orders of aircraft and a 28.3% decline in bookings of defense equipment resulted in the overall plunge in orders of durable goods. Orders of non-defense capital goods excluding aircraft increased 1.4% following a 4.3% gain in the prior month.

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, July 29, 2009.

Asha Bangalore (Northern Trust): Sales of new homes surge in June, inventories of unsold homes are sliding down

"Sales of new single-family homes rose 11.0% to an annual rate of 384,000 in June, after gains in both April and May. The bottom of the housing market appears to have occurred in January 2009 (329,000). Sales of new single-family homes have dropped 72% from the peak registered four years ago in July 2005. On a year-to-year basis, sales of new single-family homes fell 20% in June, a noteworthy deceleration following the largest cyclical drop in January 2009 (45.5%).

"The inventory-sales (I-S) ratio of new single-family homes has dropped significantly. This ratio has dropped in four of the five months ended June. The median I-S ratio is roughly a 6-month supply. The I-S ratio of all new homes was an 8.8-month supply in June, down from a 12.4-month supply in January. Unsold and sold homes are reported as three sub-categories - not started, under construction, and completed homes. Within the sub-category of unsold/sold completed homes, the I-S ratio was an 8.0-month supply in June vs. a peak of a 12.8-month supply in January.

"The median number of months to sell a new single-family home continues to advance, and in June it reached a new record high of an 11.8-month supply.

"The median price of a new single-family home was $206,200 in June, down 11.9% from a year ago. The elevated level of inventories continues to influence prices of new single-family homes.

"In sum, the housing market is stabilizing with sales of both new and existing single-family homes having advanced in each of the three months ended June and the I-S ratios of new and existing unsold homes have peaked.

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, July 27, 2009.

Standard & Poor's: Case-Shiller - home price declines continue to abate

"Data through May 2009, released today by Standard & Poor's for its S&P/Case-Shiller Home Price Indices, show that, although still negative, the annual rate of decline of the 10-City and 20-City Composites improved for the fourth consecutive month in 2009.

"The chart above depicts the annual returns of the 10-City and 20-City Composite Home Price Indices. The 10-City and 20-City Composites declined 16.8% and 17.1%, respectively, in May compared to the same month last year. These values are improvements over April's data, which show annual declines of 18.0% and 18.1%, respectively. After 16 consecutive months of record annual declines, beginning in October 2007 and ending in January 2009, the indices have now shown four consecutive months of improvement in annual returns.

"'The pace of descent in home price values appears to be slowing,' says David Blitzer, Chairman of the Index Committee at Standard & Poor's. 'There is a clear inflection point in the year-over-year data, due to four consecutive months of improved rates of return, after the steep decline that began in the fall of 2005. In addition to the 10-City and 20-City Composites, 17 of the 20 metro areas also saw improvement in their annual returns compared to those of April. Looking at the monthly data, 13 of the 20 metro areas reported positive returns; and the 10-City and 20-City Composites reported positive returns for the first time since the summer of 2006. To put it in perspective, these are the first time we have seen broad increases in home prices in 34 months. This could be an indication that home price declines are finally stabilizing.'

Source: Standard & Poor's, July 28, 2009.

Floyd Norris (The New York Times): Politicians accused of meddling in bank rules

"Accounting rules did not cause the financial crisis, and they still allow banks to overstate the value of their assets, an international group composed of current and former regulators and corporate officials said in a report to be released Tuesday.

"The report, from the Financial Crisis Advisory Group, also deplored successful efforts by politicians to force changes in accounting rules and said that accounting standards should be kept separate from regulatory standards, contrary to the desire of large banks.

"'The message to political bodies of 'Don't threaten, Don't coerce' flies in the face of some of what has been coming from the European Commission and from members of Congress,' said Harvey Goldschmid, a co-chairman of the group and a former member of the Securities and Exchange Commission.

"'We have become increasingly concerned about the excessive pressure placed on the two boards to make rapid, piecemeal, uncoordinated and prescribed changes to standards, outside of their normal due process procedures,' the group wrote in its report, which was commissioned by the Financial Accounting Standards Board of the United States and the International Accounting Standards Board.

"'While it is appropriate for public authorities to voice their concerns and give input to standard setters, in doing so they should not seek to prescribe specific standard-setting outcomes,' the report added.

Source: Floyd Norris, The New York Times, July 28, 2009.

CFO: Five firms hold 80% of derivatives risk, Fitch report finds

"Members of Congress probing threats to the global financial system - especially the threat of concentration of risk - will have a lot to ponder in newly mandated disclosures highlighted by a Fitch Ratings report issued last week. While derivatives use among US companies is widespread, an 'overwhelming majority of the exposure is concentrated among financial institutions,' according to the rating agency's review of first-quarter financials.

"Concentrated, in fact, among a mere handful of financial-services giants. About 80% of the derivative assets and liabilities carried on the balance sheets of 100 companies reviewed by Fitch were held by five banks: JP Morgan Chase, Bank of America, Goldman Sachs, Citigroup and Morgan Stanley. Those five banks also account for more than 96% of the companies' exposure to credit derivatives.

"About 52% of the companies reviewed disclosed there were credit-risk-related contingent features in their derivative positions. Such features require a company to post collateral or settle outstanding derivative liabilities if there's a downgrade of the company's credit rating.

"The Fitch analysts also found that just 22 companies disclosed the use of equity derivatives. Just six nonfinancial firms - IBM, General Motors, Verizon, Comcast, Textron and PG&E - reported exposure to share-based derivatives.

Source: David Katz, CFO, July 24, 2009.

Bloomberg: Schumer presses SEC for ban on "unfair high-frequency trades

"Charles Schumer, the third-ranking Democrat in the US Senate, asked the Securities and Exchange Commission to ban so-called flash orders for stocks, saying they give high-speed traders an unfair advantage.

"Schumer's letter to SEC Chairman Mary Schapiro yesterday raised the stakes in a debate over the practice offered by Nasdaq OMX Group, Bats Global Markets and Direct Edge Holdings LLC, which handle more than two-thirds of the shares traded in the US. With flash orders, exchanges wait up to half a second before they publish bids and offers on competing platforms, giving their own customers an opportunity to gauge demand before other traders.

"'This kind of unfair access seriously compromises the integrity of our markets and creates a two-tiered system, where a privileged group of insiders receives preferential treatment,' Schumer wrote in the letter.

"Flash orders make up less than 4% of US stock trading, according to Direct Edge and Bats. They have drawn criticism from the Securities Industry and Financial Markets Association, which is Wall Street's main lobbying group, and Getco LLC, one of the biggest firms that uses high-frequency trading strategies to make markets in stocks and options. NYSE Euronext, owner of the world's largest exchange by the value of companies it lists, told the SEC in May that the technique results in investors getting worse prices.

"Schumer, a member of the Senate Banking Committee, said he will introduce legislation to ban flash orders if the SEC doesn't act on his request.

Source: Edgar Ortega and Eric Martin, Bloomberg, July 25, 2009.

Financial Times: Emerging markets rush to issue debt

"Emerging market bond issuance has risen to record levels as investors hungry for greater risk switch to the securities because of attractive yields.

"The surge in issuance this year, to its highest since records began in 1962, is an encouraging sign for the world economy as activity in emerging market bonds had seized up until a few months ago.

"The bond market freeze had made it difficult for governments and companies, especially those in eastern Europe hit by the credit crunch and needing to refinance debt.

"Bond volumes in emerging markets have risen to $352 billion so far this year, according to Thomson Reuters, up 45% on the same period in 2007 before the financial crisis.

"July, typically a slower month as investors wind down for the summer holidays, has been the second highest for new volumes, with issuance rising to $60 billion.

"China has been the biggest issuer this month, but countries such as Poland and Hungary have been able to tap markets.

"Hungary, which was forced to turn to the International Monetary Fund for financial support, this month launched its first international bond since June 2008.

"Bankers said the pick-up in bond yields had been a big factor in attracting investors.

"Yields on emerging market sovereign bonds, measured by JPMorgan's Embi Index, are nearly 2 percentage points higher than those on single A rated US corporate bonds.

"Bryan Pascoe, global head of debt syndicate at HSBC, said: 'Although emerging market bond spreads have narrowed, they still offer a lot of value compared with developed market corporate spreads, with better credit fundamentals in many cases.'

Source: David Oakley, Financial Times, July 26, 2009.

Bespoke: Financial default risk at lowest level since June 2008

"Our Bank and Broker CDS Index measures credit default swap (CDS) prices for global financial firms on a cap weighted basis. Below is a chart of our index that shows the huge spike in default risk that occurred during the peak of the financial crisis in late 2008 and early 2009. As things have settled down, default risk has now moved well below the levels it was at just before the Lehman bankruptcy. Our CDS index is currently at its lowest level since June 23, 2008, and it's down a whopping 67% from its all-time high.

Source: Bespoke, July 29, 2009.

Bespoke: Country returns

"The S&P 500 is up 11.24% since July 10, which is a significant move in such a short period of time. The recent gains also put the index up nicely at 8.28% year to date. As shown below, the US has performed well relative to the rest of the world. Since July 10, it ranks 22nd out of 82 countries. Russia is up the most with a gain of 24.23%, followed by Hungary, Poland, Norway, Romania, and Germany. Middle and Eastern European countries have seen some of the biggest gains in recent weeks.

"While China has been the second best performing country (behind Peru) year to date, it is only up 10.32% since July 10. This is better than most countries, but it hasn't been the worldwide leader that it was earlier in the year. Five of the G-7 countries have outperformed China, and all seven G-7 countries are in the top 50% in terms of performance. This is a sign that developed markets have been holding their own against emerging markets in recent weeks. Only ten out of 82 countries are down since July 10, with Slovakia leading the way at -5.67%.

Source: Bespoke, July 27, 2009.

Bespoke: Newsletter writers turning a little more bullish

"This week's release of the Investors Intelligence survey of newsletter writers showed a moderate increase in bullish sentiment. As shown, the bulls rose back above 40%, although they're still below levels from early July. Bearish sentiment also declined, but it too is still above 30% and higher than it was a few weeks ago. The market's rally over the last two weeks has certainly improved spirits, but given the gains, one would expect a larger increase in positive sentiment.

Source: Bespoke, July 29, 2009.

Bespoke: Are institutions participating in the rally?

"We recently broke the S&P 500 into 10 deciles (10 groups of 50 stocks) based on the amount of a stock's shares that are held by institutions. We then calculated the average performance of the stocks in each decile since the rally ramped up again on July 10. As shown below, the two deciles of stocks with the most institutional ownership are up the most, while the decile of stocks with the lowest institutional ownership is up the least. Based on this analysis, institutional investors do believe in the rally, and maybe even more than individuals.

Source: Bespoke, July 27, 2009.

Clusterstock: Shades of 1929

"We've put together an amazing, fool-making rally since the market hit its lows in early March. Of course, before you break out the champagne, remember that a strong bull run can happen during a long-term decline.

"We have eclipsed most such precedents. But we did have one big bull run of nearly the exact same length and magnitude between November 1929 and April 1930. And you know what happened after that.

Source: Joe Weisenthal and Kamelia Angelova, Clusterstock - The Business Insider, July 30, 2009.

Bespoke: Dividend stocks outperform during the rally

"Prior to the 2008 financial crisis, investors typically flocked to stocks with high dividends as safety plays when the overall market was in correction mode. However, since so many financial stocks had nice yields, dividend stock indices and ETFs actually underperformed the S&P 500 throughout the last bear market. The ability for companies to actually pay their dividends eventually came into question, and that added even more fear to owning high yield stocks.

"Below we highlight the performance of the Dow Jones Dividend Select Index versus the S&P 500 during the bear market that ran from 10/9/07 to 3/9/08. As shown, the dividend index was down 60.3% versus the S&P 500's decline of 56.7%. Since the March 9 bottom, however, dividend indices have outperformed. As shown in the bottom chart, the same dividend index is up 51.16% while the S&P 500 is up 45.18%.

Source: Bespoke, July 28, 2009.

Bespoke: Q2 earnings growth versus estimates

"At the start of the second quarter, the consensus estimate was that S&P 500 earnings versus Q2 '07 would be down 31.3%. As shown below, this estimate trended downward to a low of -35.1% on May 15, picked back up again through the end of May, and then dropped to -35.2% on July 10 just when earnings season was beginning.

"One of the reasons the market has done so well this earnings season is because actual earnings growth has come in better than expected. Fifty percent of the S&P 500 has reported second quarter numbers, and the collective change in earnings from Q2 '07 to Q2 '08 has been -24.8%. This is a negative number, but compared to the estimates, it's a positive.

Source: Bespoke, July 29, 2009.

Clusterstock: China's incredible run

"Chinese shares crashed 5% on Wednesday, setting off a mild panic about Asian stocks and currencies. Chinese stocks have had a massive rally this year, by far outpacing the S&P's meteoric rise since March. So perhaps a pull back shouldn't be that much of a surprise.

Source: Joe Weisenthal and Kamelia Angelova, Clusterstock - The Business Insider, July 29, 2009.

Bloomberg: China stocks plunge on tightening concern

"China's stocks plunged, driving the Shanghai Composite Index down the most in eight months, on speculation the government will curb inflows into a market that had doubled from last year's low.

"The benchmark gauge lost 5%, snapping a five-day, 7% advance that pushed valuations to their highest since January 2008. The gauge has gained 79% this year as government stimulus spending, record bank lending and an economic rebound spurred demand for equities.

"'Speculation the central bank may take steps to rein in liquidity worried the market,' said Gabriel Gondard, deputy chief investment officer at Fortune SGAM Fund Management Co., which oversees about $7.2 billion in assets. 'A lot of people were looking to take profit' after the market gains.

"'Expensive valuations and jitters among investors about fast share-price gains are enough to trigger panic selling like today,' said Larry Wan, Shanghai-based deputy chief investment officer at KBC-Goldstate Fund Management Co., which oversees about $583 million in assets.

"Stocks plunged amid speculation the central bank is poised to order lenders to set aside larger reserves, Beijing-based Caijing magazine reported today on its website. Market News International said Chinese equities fell on speculation regulators will increase a tax on stock trading.

Source: Bloomberg, July 29, 2009.

MoneyNews: China says loose monetary policy to stay

"China's central bank pledged to maintain loose monetary policy to support the economy and said it would ensure sustainable credit growth without resorting to heavy-handed quotas to rein in a lending spree.

"In a statement that analysts said was intended to calm skittish markets, the People's Bank of China Vice Governor Su Ning said the central bank 'will unswervingly continue to apply appropriately loose monetary policy and consolidate the economic recovery momentum.'

"The statement was posted on the bank's website after Wednesday's 5% fall in the Chinese stock market, its biggest daily drop in eight months, which had been sparked in part by worries that Beijing would restrict bank lending.

"But there was also a hint of a gradual shift in policy footing when an unnamed official was quoted by state-run Xinhua news agency as saying that the central bank would 'fine tune' its loose monetary stance and keep prices 'within a reasonable and controllable range'.

"Officials have expressed concern about the risk of stock and property bubbles inflating because of an unprecedented surge in bank lending, and the central bank said this week that consumer prices, now in mild deflationary territory, could start rebounding after the third quarter.

"China has in the past used a quota system to control lending, telling banks not to exceed specific ceilings. This credit management was a key prong of China's monetary tightening in 2008 and it was subsequently blamed for contributing to the economy's sharp slowdown in the fourth quarter.

"Su's comments appeared to rule out an imminent return to a strict, central bank-directed quota system.

"'They are responding to an incorrect interpretation by the market,' said Ting Lu, economist with Merrill Lynch in Hong Kong.

"Beijing has tamped down a little on the tide of money washing through the economy, but it is seen as unwilling to shift to more substantial tightening until a full-fledged recovery is assured.

Source: MoneyNews, July 30, 2009.

Bespoke: IBD 100 China edition?

"Investors Business Daily has its IBD-100 list that highlights the most attractive stocks from an earnings, growth, and relative strength perspective. When the market is rallying, the IBD-100 has historically outperformed, and when it corrects, these stocks usually underperform.

"This weekend, however, we wondered whether we were reading an alternate edition of the newspaper. When looking through the top stocks in the IBD-100, seven of the top eight and ten of the top twenty were Chinese stocks listed in the US. We're all well aware of how China has recently been the leading force of economic growth, but given the strength in these names, one has to at least wonder how much of this growth has already been priced in.

Source: Bespoke, July 28, 2009.

MoneyNews: Gross: Wall Street to blame for high fees

"Bill Gross, the influential manager who runs top bond fund PIMCO, on Wednesday lambasted his industry for charging investors hefty fees for subpar performance amidst the worst economic crisis since the Great Depression.

"In his latest investment letter to clients, Gross, co-chief investment offer of Pacific Investment Management Co., said roughly 90% of the $1.5 trillion in 401K and other defined contribution assets in mutual funds are 'actively managed'. And yet many of those portfolio managers posted unspectacular performance for exorbitant fees, close to 1%, he asserted.

"He likened the situation to the infamous Madame Rue selling Potion #9.

"'I've never known any gold-capped tooth money managers, but without squinting very hard there is undoubtedly a strong resemblance between all of us 'managers' and the infamous Madame Rue selling Potion #9,' Gross said. 'Instead of love, though, we sell 'hope', but very few are able to seal the deal with performance anywhere close to compensating for the generous fees we command.'

"Gross said investors paying for those potions during an era of asset appreciation with double-digit returns may have been 'tolerable', but if investment returns gravitate close to 6% as his firm envisions, 'then 15% of your income will be extracted based on the beguiling promise of Madame Rue'.

"He highlighted a recent Barron's article that pointed out that stock funds extract an average 99 basis points or virtually 1% a year in fees from an investor's portfolio, while bond managers at 75 basis points. Many money market funds manage to charge 38 basis points.

"'Since money market funds barely earn 38 basis points these days, much of the return winds up in the hands of investment managers,' Gross said. 'A mighty expensive potion indeed.'

"For his part, Gross' PIMCO Total Return Fund, whose assets under management of $164 billion makes it the world's largest mutual fund, ranks as a strong performer. The Fund charges 46 basis points to investors.

"Gross reiterated that economic growth for the United States will fall short of recent years, expanding around 3% a year once it emerges from recession. The US economy was growing at 5-7% a year for 15 years before it plunged into the worst recession in decades.

"Slower growth means lower profit growth, permanently higher joblessness, constrained consumer spending and increased government involvement, Gross added.

"'The 'new normal' nominal GDP, the future return on our stock of labor and capital investment, will likely be centered closer to 3%, for at least a few years once a recovery is in place beginning in this year's second half,' Gross said. 'Diminished capitalistic risk taking and constrained policymaker releveraging will lead to that likely conclusion.'

Source: MoneyNews, July 29, 2009.

Steve Barrow (Standard Bank): SNB battles stubborn franc

"Signs are finally emerging that the Swiss National Bank (SNB) may succeed in its aim of driving down the franc, believes Steve Barrow, currency strategist at Standard Bank.

"He notes that it is highly unusual for a central bank to promise to keep a currency from rising. 'It is more common for them to aim to avoid currency weakness. This is a very important difference.'

"Usually, he says, central banks looking to defend their currency face the problem that they could run out of reserves. Any hint of this happening can lead to intense pressure on the currency. But for the SNB, no such constraint exists - it can intervene with a potentially limitless supply of newly-printed francs, which should leave the market running scared.

"So why has the franc stubbornly refused to fall?

"'All theories concerning the effectiveness of intervention stress the importance of falling interest rates,' Mr Barrow says. 'The problem for the SNB has been that rates are about as low as they can go with a three-month Libor target of 0.25%. But there are signs of a bit more rate divergence now, especially further down the curve. For instance, quite a gap has opened up in 10-year bond spreads between Germany and Switzerland.

"'With similar, if smaller, divergences creeping in at the front end, the euro could be on its way back to the SFr1.5450 level seen in the wake of the original decision to target franc weakness in March.'

Source: Steve Barrow, Standard Bank (via Financial Times), July 29, 2009.

TheStreet.com: Frank Holmes - gold will hit $1,300

"Frank Holmes, CEO and Chief Investment Officer of US Global Investors, argues that deflation and the dollar are the main factors moving gold futures and he outlines his number one trading strategy for the rest of the summer.

Source: TheStreet.com via (via YouTube), July 30, 2009.

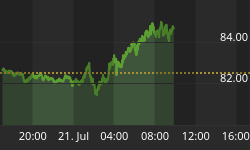

Bloomberg: Goldman - crude oil to rise to $85 by year-end

"Goldman Sachs Group Inc. said it is maintaining its forecast that West Texas Intermediate crude oil will reach $85 a barrel by year end as the recent weakness in market fundamentals will be temporary.

"Oil demand will be supported by stabilization in US industrial activity and a positive outlook for China's economic growth, the bank said in a report today.

"'Concerns over economic growth and weak oil statistics led a commodity sell-off yesterday,' said Goldman analysts, led by London-based Jeffrey Currie. 'However, we believe most of these drivers are less negative than they first appear.'

"'We maintain that demand stabilization will be critical to a sustainable rise in oil prices that we expect later this year,' the analysts said. 'Stabilization in industrial activity and a nascent slowing in industrial destocking give us confidence in this view.'

"Goldman closed its recommendation to buy crude futures for December 2011 delivery in a July 27 report after long-dated oil prices approached the bank's target of $85 a barrel.

Source: Bloomberg, July 30, 2009.

CNBC: Speculators hiked oil prices - Chilton

"New data shows speculators played an important role in last year's hike in oil prices, Bart Chilton, one of four CFTC commissioners, told CNBC Tuesday.

Source: CNBC, July 28, 2009.

Nationwide: UK house prices up for third month in a row

"The price of a typical house rose for the third consecutive month in July, increasing by 1.3% on a seasonally adjusted basis. The 3 month on 3 month rate of change - generally a smoother indicator of the near term trend - rose from 1.0% in June to 2.6% in July, the highest level since February 2007. House prices are still 6.2% lower than 12 months ago, but this represents another sharp improvement from the 9.3% year-on-year decline in June.

"Even if prices were to remain unchanged for the rest of 2009, the year-on-year rate would continue to improve since prices were falling very sharply in the second half of last year. For the first seven months of 2009 as a whole, prices have risen by a cumulative 1.3%, suggesting there is now a reasonable chance that prices could end the year slightly higher than where they started. Only a few months ago, such an outcome would have appeared unthinkable.

Source: Nationwide, July 30, 2009.

The Wall Street Journal: UBS, Swiss reach pact on US tax probe

"UBS AG and the Swiss government, rocked by months of embarrassing details about bank secrecy and guilty pleas for UBS clients, agreed to settle a tax-evasion probe with US authorities.

"The agreement appears to signal that thousands of US client accounts, hidden in offshore shadows, will be turned over to US revenue agents.

"The settlement, announced during a teleconference with a federal court judge Friday ahead of a scheduled hearing in Miami on Monday, closes one chapter in the long-running case that centered on the Internal Revenue Service's demand that UBS turn over the identities of 52,000 UBS accounts that belong to UScitizens.

"Details of the settlement weren't provided during the call, with the Justice Department simply reporting that the parties had reached an agreement in principle and would work to resolve remaining issues in the coming week. Another conference that could shed more light on the deal is set for Friday.

"But lawyers involved in the case said one likely scenario is that UBS will turn over the identities of some, but not all, of the 52,000 accounts.

"'I think it's possibly going to push north of 10,000,' said William Sharp, a Tampa, Fla., lawyer who is representing UBS clients and was working on the case in Zurich in the past week.

"'We have never before seen so many US citizens and residents potentially subject to criminal tax prosecution on the same basic issue,' said Bryan Skarlatos, a partner at New York law firm Kostelanetz & Fink LLP who is representing UBS clients.

"UBS and the Swiss government argued in the tax-evasion case that Swiss bank-privacy law meant the bank couldn't hand over the account identities. It now appears that UBS and the Swiss government have combed through the files and identified enough potential fraud to make them willing to hand over information about certain accounts.

"Swiss laws don't provide confidentiality if people engage in fraudulent activities such as setting up accounts with shell companies that lack any real business substance.

Source: Carrick Mollenkamp, Stephen Fidler and Laura Saunders, The Wall Street Journal, August 1, 2009.

Did you enjoy this post? If so, click here to subscribe to updates to Investment Postcards from Cape Town by e-mail.