One of the most important questions investors have about gold stocks is "which is the best stock to buy"? You want to invest in the next ten bagger, all investors do. Huge profits that leverage the coming gold price rise are most certainly possible in gold stocks however you are unlikely to achieve this by luck. Choosing without in-depth evaluation is a recipe for disaster.

I will repeat again- I have never been more excited about the prospects of the gold mining sector here in Australia. Soon we will see an awesome buying opportunity for the precious metals (physical or ETF's) and the quality gold mining stocks so I am gearing up in readiness. This is the time to get the homework and preparation done.

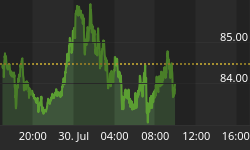

Quick market comment- the XGD still going against the general market most days this week and bounced off a new short-term low. RSI made a new low for this correction indicating it was oversold but also that we may still be on the way down albeit gently. This is not a savage correction in the XGD but we did warn it was going to happen and it is still ongoing. I am watching for the turn around in the charts and see it could potentially come soon due to seasonal factors.

I spoke to one investor last week who was watching a "falling knife" looking at the value- his assumption was that this stock with a plummeting share price is cheap now. My assumption is that this stock is in trouble and that investment is a high risk. If he is right he gets a bargain but this is not a wise method to choose a stock. Different valuation models have to be used, not just price which can be highly dangerous.

Tough Business

Gold mining is tough for the miners and for investors to evaluate. Education on this subject is so important to making profits as an investor. I have just done a study with an in depth evaluation of a gold company so I could provide some answers on this complex subject. It was time consuming and I already had an excellent understanding of the company I chose as the main example.

I spoke to a founding Director, the Information Communications and Technology Manager, the Exploration Manager and the CEO in order to verify facts and research the report. I went through the web site, tangible assets, EV, ground position, Management skill sets, company reports, broker reports and my own investor education files from the GoldOz Gold Members area to calculate, evaluate the company - and also to compare the stock to its piers.

Forward earnings were evaluated in depth as part of the exercise- an essential element in profitable investing. Also touched on were the modern technologies being employed to unearth the balance of the available gold Resource on their ground position.

It is also highly useful to look at comparative advanced operations in terms of resources, cash flow, share price / market capitalization and geology to establish potential should the company you are considering reach that stage of company evolution. Will it succeed; does it have cash flow or other problems / limitations that could stop progress? These are vital questions.

The exercise was highly rewarding as I eventually gained the informed knowledge about the geology, mine progress, corporate strategy and finances required to come to any sort of reliable conclusion. Some non company specific excerpts from the research are offered in this article.

"General comment:

Astute investors value gold stocks via several benchmarks including resources, assets, production and profitability, life of mine, quality of management and ground position. These factors point to sustained future growth in share price = investor profits.

The balance sheet indicates financial health and potential yield- how much return am I going to get if I park my capital into this investment over time? As such we also find debt, hedge book obligations, convertible notes and royalties influence share price too."

And...

"Distortions in share prices based on general market sentiment also create opportunity, eventually under-valuation leads to over-valuation. This will be the time we seek to sell and take profits.

Make no mistake though- the single most important factor that drives any share price is money- purchasing pressure. I am talking about two buyers for every seller (or better), liquidity pouring into a stock in a sustained flow forcing the share price higher.

This can only result from broad investor / broker interest and media attention. In other words share price is driven by positive promotion in its various forms. To achieve this, a stock needs a good story initially followed by a positive information flow and over time it needs a high level of profitability over a sustained period."

Also...

"General comment: The JORC contained assets are not yet mined and production costs in future years are not yet known- however these assets do point to projected profits and LOM (life of mine) which indicates mine sustainability. Commodities fluctuate in value which increases risk in future years if sale prices drop along side an increase in costs. Therefore high margin ore-bodies that can be mined over extended mine life after capital expenditure is returned are more attractive."

When establishing a potential gold endowment of their assets looking forward...

"When you add historic gold production to the current un-mined resource this field has already established an endowment of 4.52M oz in total. I am saying that a total of 7.5 M oz is quite possible with sufficient drilling and use of the right technologies. Archean Greenstone Belts of this scale typically average about 7-10M oz. This is a global average across Russia, Canada, Australia (Kalgoorlie, Leonora, Noresman, St Ives, Paddington etc), Brazil & China."

When looking at various balance sheet questions and financial aspects...

"Assets of approx $230M and short term liabilities of $20M gives a balance of $210M by this valuation model. Forward earnings however suggest a $30M gross profit which gives us a current market capitalization of 2.5 x gross profit. These earnings are current however they are not guaranteed to be on-going short-term due to the mill refurbishment / start up risk."

The whole 13 page report is linked at the end of this article for interested investors and at the top centre home page on my site. It is written in plain English for education purposes because I want to communicate some skills and knowledge- there is no point in being illegible because you don't get the message across.

On this point I feel many mainstream investors run away from investment in the mining sector because they don't understand the jargon. I must admit is can be daunting but understanding the nature of the deposit is essential. Over the years I have found a most useful trick- simply gaining the most important piece of data about the deposit. Of course I have to understand the deposit to a far greater degree but this is an indicator that is important.

This equates directly back to cash cost but learn to look at the reports carefully and workout how much actual cost is being capitalized. Otherwise high development costs can be hidden distorting the real profitability picture. Are the development costs ongoing or just an initial pain in the balance sheet? Some deposit types are just troublesome and so are some sovereign states.

But generally you may see high or low grade ore yielding similar profits and this will give away the end game. It's about profits. We are offering a limited discount subscription for Gold Membership at present- offer runs out on 4th September so consider your timing if you have interest. Here is the link promised above to the offer and free educational report.

Good trading / investing.

Regards,