The lack of fresh economic reports today gave traders no choice but to look at the trend and resume selling pressure on the U.S. Dollar. The U.S. Dollar resumed its downtrend from the opening of the New York trading session after trying to mount a small comeback late last week. Better than expected earnings or projections for better earnings in the future helped drive up equity prices which in turn boosted demand for higher risk assets. Fed Chairman Bernanke said very little today to boost the Dollar but did say that Washington is concerned about its drop in value. He noted that the U.S. faces a "difficult fiscal situation" which is said to be the cause behind the lack of confidence in the U.S. economy and the Dollar.

The EUR USD is slowly working its way toward the psychological 1.50 resistance barrier. Traders are uncertain what will happen if this area is breached. Some feel an acceleration is in order while others feel that buying will dry up slightly above this level. Euro Zone finance ministers are meeting in Luxembourg at this time to discuss the fate of the Euro. Most are expected to voice concerns about the rapid rise in price and its potential detrimental effect on Euro Zone exports. No solution to the problem is expected to be presented, but traders are anticipating some commentary supporting a stronger Dollar.

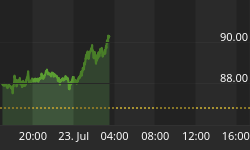

The GBP USD started the day lower after a story leaked over the week-end that the Bank of England was considering expanding its asset-buyback program. Last week speculators drove up the Pound as comments from a BoE official hinted that it would end the program. By midsession, the British Pound had erased all of its loss and near the close was in position to close higher. Today's action demonstrates that positive momentum is still present in the market.

Stronger equity prices helped drive up demand for higher yielding assets. This helped put pressure on the USD JPY as traders continued to treat the U.S. Dollar as a funding currency because of low U.S. interest rates. Traders continue to use the Dollar as a carry currency because of the Fed's decision to keep U.S. rates at the lowest level in the world.

Higher crude oil and equity prices helped boost the Canadian Dollar. Despite tomorrow's Bank of Canada meeting, investors were not reluctant to trade the long side of the market today. Traders expect the BoC to leave interest rates unchanged at this meeting but may issue a statement regarding the time period it expects to begin raising interest rates. Last week's lower than expected CPI figure supports lower rates at this time, but central bank officials will be basing their long-term outlook on the possibility of a recovery in 2010.

Investors will also be looking for any commentary about the value of the Canadian Dollar. Last week, Canadian Prime Minister Harper voiced his concern about the rapid rise in the currency and its possible adverse effect on the ability of the economy to sustain its developing recovery.

Increased demand for higher yields helped to drive up the NZD USD and AUD USD on Monday. Today's strong rallies helped to negate last Friday's dramatic closing price reversal top. Traders are now beginning to speculate that the Reserve Bank of New Zealand and the Reserve Bank of Australia will raise interest rates at their next meetings in November. Some investors are even placing trades in anticipation of the RBA hiking rates as much as 50 basis points. Strong demand for commodity exports is expected to keep upside pressure on both of these currency pairs.