The Anatomy of an International

Monetary Regime (Oxford

University Press, 1995).

Every now and then a viewpoint so convincing and inherently logical captures the crowd, it becomes near impossible -- psychologically, at least -- to counter its premise. At such times, a seeming arrogance born of a zombie-like consensus assumes its position to be beyond reproach ... in fact, beyond truth itself. When that happens, the analytical brain-cells can be cowed into self-doubt.

What we are talking about here is the fate of the U.S. dollar and gold bullion. The "gold fever" hype is hitting the mainstream ... i.e. "Dump the dollar! Buy gold," a headline from Fortune Magazine recently blazes. Would it be foolish to consider countering the consensus on these topics right now? "Fools rush in where angels dare tread."

However, isn't it true that absolutely everyone knows that gold bullion must soar in price because central banks around the world are reflating as never before? Everyone also seems sure that the U.S. dollar is likely to collapse in the very near future. We are to believe, then, that these two outcomes are absolutely ineluctable ... born of unassailable logic ... as good as already happened.

Some readers may be tempted to think that only fools can't see that gold is heading to $2500 per ounce and that the U.S. dollar is finished. Fools we may be.

Perhaps not so foolishly, we have been "structural" dollar-bears for a long, long time and, frankly, still have no sufficient reasons to change our long-term perspective here. Also, we have held significant "above-weight" exposures to gold and gold equities for a number of years ... and, by and large, have held them to this point. Alone the low correlation of this asset class has had a lustrous effect upon portfolio performance at times. We surely are not about to recant our beliefs that central banks in a clinch will always inflate. Fiat money will continue to be the servant of corrupt governments and political demagoguery.

However, all that said, we want to turn our attention to gold. The facts simply do not add up to support a hyperinflationary phase ... at least not for some time. Therefore, before we risk getting swept up into a possible "manic phase" for gold, it would be wise to test the apparently "self-evident" rationale of the current "gold consensus." Are the reasons luster or bluster?

From Market Lore to Gold Ore

All we are wanting to accomplish here is to remind of several recurring lessons of free markets; the actions of human crowds; and to identify what is different today from previous periods of dollar weakness and surging gold prices.

To start, let's take the following points as a given:

1. When absolutely everyone holds the same view, it is usually pretty much too late to jump on the bandwagon. The momentum of new converts to the bullish view dies out.

2. When it comes to financial matters, the future is never perfectly predictable no matter how certain the consensus view.

3. Gold's ascent may be inversely related to the fall of the U.S. dollar of late, however, all currencies are fiat, not just the buck.

4. In the case of currencies, relativity matters more than absolutes ... especially at this late stage of global capital mobility. As colleague, Director of Research, Tyler Mordy has written, currency analysis these days is really a matter of conducting an ugly contest.

5. Gold is not sacred money nor imbued with special powers of monetary truth. Last we checked, it was still a metal found on planet earth, the value of which can also be manipulated by both crowds and governments. (See quote on the front page.)

6. Inflation is a chameleon. Its different guises are not always well recognized nor necessarily manifested in the fashion expected. There is not observed a tight correlation between the gold price and consumer price inflation nor any other inflation symptom.

7. Fools do rush in for lack of better sense. This is one of the reasons why illogical, manias (also involving gold) can continue much longer than any rational person may think.

The above points call for some aloofness from the current gold rush. Yet, the arguments fanning interest in gold are seemingly convincing. After all, there has been much negative press on the inflationary monetary actions of central banks around the world, particularly so the U.S. Federal Reserve Bank.

Also, the gold price has been rising fastest in U.S. dollar terms because the U.S. currency has again entered a weakening phase against virtually every currency in the world in recent months (with the notable exception of the Chinese yuan. That said, the U.S. Dollar Index has yet to fall below the lows of early 2008.)

Isn't it a fact that central banks are creating a lot of money out of thin air these days? Yes, very definitely. Initially, that did alarm us, too. But such actions are only part of the picture. There are additional factors to consider. Advisors that are recommending that investors "jump into" gold, presume that world conditions today are exactly the same as other periods when gold prices rose rapidly. As we will show, this is not really the case.

Indeed, it is possible that gold bullion prices can continue to rise higher -- that there really is no telling just how high it may rise if a hyped-up mania takes hold. Yet, there very definitely are new factors playing out today that should not be overlooked. We count at least 4 that we believe do not support the "bluster."

Therefore, let us rush in.

Four Against The Ore

For one, the world is today experiencing conditions that are remarkably different ... frankly, different from ever before. The times are unprecedented; the waters uncharted. Consider that a large part of the world economy -- a problem concentrated in the advanced nations -- are experiencing a retirement crisis; also an "income crisis." Given "cupboard-bare" interest rate levels (virtually zero on most short-term deposits), pension funds today are starving for higher levels of income and so are most retirees. Investors today are more anxious about earning income that they were the last time gold soared in price. We call it "Zero Intolerance."

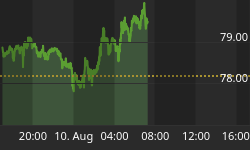

Comex Gold, Continuous Near Month Contract, USD

Source: www.sharelynx.com

Frequently cited is the previous "gold rush" that occurred between 1980 and 1982. The price of an ounce of gold then soared above $800 from a level of less than $100. I well remember the long line-ups of people jostling to buy gold wafers at the time. To the pained chagrin of many of those people, the price of gold eventually fell all the way back below $260. Please view the gold price (futures) chart on the opposite page. You will note that following the emotional gold price spike upwards, in the early 1980s, (a pattern evincing a similar frenzy as we are starting to again see today) prices fell markedly. Today, advisors reason that since governments are pursuing similar inflationary policies as prior to that earlier time, that therefore the same outcome for gold can be expected today. This is not necessarily a logical deduction. Why?

Don't forget that gold bullion does not yield income (for the average investor, in any case). Technically, you can't live on income from gold and neither would that be possible for the entire world. Gold ownership may be a claim on wealth, but it does not itself facilitate flows of income or profits from production. You must sell it to generate the cash to live on. While this point certainly did not limit tulip bulb prices from soaring in 16th century Holland, all the same, we would take a good quality bond (with a decent yield and denominated in a reasonably solid currency) over gold any day. Of course, the operative differentiators are "quality" and "solid."

Investments that yield income (i.e. interest or dividend payments) are likely to be just as eagerly sought during these threadbare times of income. In fact, to date in 2009, some high-yield bond categories have outperformed gold.

Moreover, we observe that lately bonds have been rising along with the price of gold. This fact alone should caution the rampant gold bulls.

How is it that gold bullion and bonds are rising simultaneously? This isn't following the script of the inflationist "gold bugs." Actually, this pattern is more diagnostic of deflationary than inflationary pressures.

But surely aren't the U.S. and other nations fated for a hyper-inflationary spiral? While central banks are indeed trying to re-inflate the world with their fiat money creation, this is not the sole determinant of an inflationary outcome.

Our second point is that other factors also play a role. For example, the capital destruction caused by an imploding debt situation, can cause deflation no matter how much central banks may want to intervene with cheap money. Deep black holes on bank balance sheets are "monetary destruction." Filling these holes with "created money" definitely causes distortions in the pricing of risk, however, it is only replacing money ... not necessarily creating net new money. This has indeed happened by way of the deflating collateral value of real estate in recent times. Plunging collateral values have destroyed a lot of money as mortgages are becoming impaired and requiring write-offs (with another wave expected ahead). There are other factors that are not well appreciated especially during times where private debt is contracting as is now the case.

Thirdly, before jumping onto the gold bandwagon now, it should be recognized that the workings of monetary inflation once intermediated through global capital flow channels can be inverse to expectations. Today, "falling prices" can actually be caused by inflationary policies. That indeed has been the case for some time. It happens to be a peverse side-effect of a globalized, interconnected world of trade and money flows. How so?

Suffice it to provide a brief example. Consider that the inflationary policies of some countries actually have the consequence of overinvestment ... meaning here, the overbuilding of productive capacity in the form of factories and public infrastructure. Rather than giving rise to a condition of overconsumption (as tends to occur in North America) which may cause consumer prices to rise, in this case the opposite occurs.

Huge credit-inflated, over-expansion in manufacturing capacity causes a surplus of export goods, which in turn causes downward pressures on consumers prices. Anyone benefiting from the yellow "happy face" proclaiming low prices at Wal-Mart stores will understand the impact of expanding Chinese production.

So we see that in the globalized world of today, the inflationary policies of one country can work through international channels by facilitating the over-stimulation productive capacity abroad, to perversely return domestically in the form of falling goods prices. That effect was evident in the case of Japan's "bubble" of the late 1980s. Now, it is happening on a grand scale through the hyper-expansions of the China-centric manufacturing hub.

Don't overlook the fact that China's boom of today is also, in part, the product of an unsustainable inflationary bubble. Its massive increases in industrial capacity are far out-running demand. Now that the American consumer is deleveraging and cutting back spending, China faces significant challenges in re-establishing its former pace of export growth. Consumer prices will therefore remain under pressure. Moreover, China will most certainly face its own crises in future years.

Another difference to realize (especially for those who are expecting another Weimar era of hyperinflation as occurred in 1920s Germany) is that today there exist well developed bond markets. This factor, along with an aging population in much of the Western nations, suggests that bond markets will be highly vigilant against inflation. While it is true that bond markets are also prone to financial bubbles, over time they nonetheless are adverse to rising inflation. Interest rates tend to rise when threatened by rising consumer price inflation. Rising interest rates in turn act as a depressant on inflation ... a type of regulator.

Conclusion: A Dangerous Confluence for Gold

To sum up, just why should gold be such an attractive investment right now ... at currently elevated prices? Most people, of course, would answer this question quite simply: Because it is going up in price! Well, yes, that has been obviously the case looking in the rear view mirror.

Gold may indeed get caught in a psychological updraft for no other reason than the hyped and emotional fears of the masses for a time. However, as we have pointed out, it is not a one-way bet as may be popularly presented. Even as gold prices have risen, the very seeds of its future collapse can already be discerned.

Financial trends rarely reward the frenzied opinions of the crowd. Were the basic premise for soaring gold prices correct, then the bond market would soon crash and interest-rate yields would soar. That in turn would undermine a gold rally.

We make one final point. Just what "hard asset" would be most ideal to ride during an inflationary period? The graph on the front page leads to an answer. Despite the fact that corporate earnings and dividends have fallen, dividends remain high relative to the norms of the last 40 years versus National Income.

The bottom line? Don't get carried away by the pitchmen and cheerleaders for gold who want you to take out a mortgage on your house and to load up on gold-related investments. Some gold and other assets in the context of a diversified investment portfolio makes sense.

But, a continuing gold frenzy? Hyperinflation or yet a final debt-induced deflation? The jury is still out. But frankly, as of this point, the continuing high dividend pay-out in the corporate sector (still high in relation to National Income) and falling interest rates, argues that assets prices are more anticipating the future effects of deflation rather than hyperinflation. Gold, too, can be expected to perform well in this scenario. But, only in the earlier stages of a deflationary period.

Ounce for ounce, facts and trends to date suggest that some lightening up on gold position during the current upward surge will make some sense. Rather than raising weightings, our inclination is take opportunities to lower our gold exposure.