The calendar date is now sufficiently far enough in the future from the injection of massive amounts of liquidity by the world's central banks in 2008 that if inflation was to be a consequence of that action, it would be readily evident. However, as we look around the world, inflation exists only in isolated cases. Certainly in the U.S., inflation is non existent. At the same time, rather than collapsing into oblivion, the U.S. dollar has been in a rally.

Pockets of inflation have appeared. Argentina, India, and China are experiencing rising prices. In the first two cases that experience may be more due to production shortfalls rather than money creation. Prices in China may be rising due to excessive credit creation. However, that development may also be a means of lowering that nation's export surplus without altering the Yuan's relationship to the dollar. But, again, to date, U.S. inflation remains moderate or near nonexistent.

Our first chart this week, above, helps to explain why, one, U.S. inflation is moderate, and, two, why the U.S. dollar has not collapsed into oblivion. In that chart are plotted two measures of the growth rate for the U.S. money supply, M-2 NSA. The blue line is the two-year growth rate, annualized. It might be considered the slow-moving average. Red line is the one year rate of change, or the fast-moving average.

In the fall of 2008, the Federal Reserve, along with most of the world's central banks, began a massive injection of liquidity in response to the collapse of the mortgage bubble. As we can see in the chart, both measures of money supply growth moved upward. That experience caused widespread expectation of higher U.S. inflation. The same expectation existed in other countries where these liquidity injections occurred.

However, since then money supply growth in the U.S. has slowed dramatically. As shown in the chart, the one year rate of growth for the U.S. money supply is approaching zero. Expectations of U.S. inflation rising when the money supply is not growing are unlikely to be fulfilled. Current growth rate of U.S. money supply is non inflationary.

A further consequence of this meager growth rate for the quantity of U.S. dollars is that they are becoming relatively rarer. As the rate of dollar creation slows, the relative value of the dollar should rise. Expectations of the value of the U.S. dollar falling dramatically, ceteris paribus, are also likely to experience disappointment.

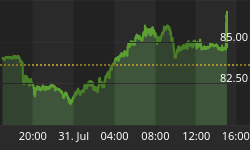

As the widely used trade-weighted index for the dollar is a meaningless measure in a world where currency values are dominated by financial transactions, the above chart of the dollar's value is more useful. As can be observed in that chart, the value of the dollar has now been rallying for a number of weeks. Each plot in that chart represents the closing value of the dollar on a weekly basis.

In a world where U.S. dollars are becoming relatively rarer, little reason exists for the value of the dollar to fall against other currencies. $Gold is simply another world money. Just as the Euro has declined against the dollar, so should have the value of $Gold. Those movements are the same phenomenon. Comments such that $Gold is down because the dollar is up, quite frankly, are gibberish.

Until such time as the quantity of dollars rises, the value of $Gold should change little. $Gold should remain lethargic in such an environment. It, however, may soon complete the A-wave in an A-B-C correction. With that view, a B-wave rally is possible in the next few weeks. From that move should develop a C-wave correction that takes $Gold to a Summer bottom. Dollar-based buyers should be aggressive in these corrections.

Investors in other currencies have now learned the wisdom of owning Gold. Too many continued to be invested in financial assets that clearly were priced at vulnerable levels. EU investors certainly did not expect Greece to spoil their asset values. Greece is insignificant in terms of its economic importance to the EU. Greek financial problems simply raised to the surface the EU's yet unfinished nature. Investors should not rely on currencies retaining value in all financial environments. Those living in Euros and British pounds should be buying Gold as a defense against the political and structural problems of the EU on any price weakness.

GOLD THOUGHTS come from Ned W. Schmidt,CFA,CEBS as part of a joyous mission to save investors from the financial abyss of paper assets. He is publisher of The Value View Gold Report, monthly, and Trading Thoughts, weekly. To receive these reports, go to www.valueviewgoldreport.com.