There's nothing like a potential act of war to press the 'pause' button on a bear market in bonds. The sinking of a South Korean warship in disputed waters (well, disputed by North Korea) initially raised concerns that the sinking was at the hands of Kim Jong-Il's minions; while no one is really sure yet if that is true, or whether such an action would be part of an intentional provocation or a spastic exercise of diplomacy by other means (my bet is on spastic), the point is - as it always is when the Supreme Leader is concerned - that no one is really sure of what's likely to happen next. It seemed prudent to cover short positions in bonds in such a context, but as the weekend has passed without further incident this has probably faded as a bullish influence.

Some bond bears were probably also scared by the fact that CNBC asked the question on Friday, "Time To Sell Bonds To Buy Stocks?" (Remind me when they last asked whether it was time to sell stocks to buy...anything?) They're half right this time, I think, but I don't like having them as company either. Balancing the Groucho effect ("I don't want to belong to any club that would accept people like me as a member") is the Holiday Inn Express effect (in which people develop amazing abilities unrelated to their backgrounds: "Are you a doctor?" "No, but I stayed at a Holiday Inn Express last night"). Barron's, specifically Michael Santoli, who writes the "Streetwise" column, sought to explain why rising yields are good for stocks. When equity guys are busy telling the bond vigilantes why they're not scared of them...they're scared of them.

During a day in which there was little in the way of economic data, several Fed speakers were on the tape. While it is ordinarily very important to listen attentively to comments from Fed officials, these days it isn't so crucial because we know what conditions will lead to meaningful tightening and they (much lower unemployment rate, some sign of broad core inflation including housing) aren't going to happen any time soon. Why? Dr. Bernanke is fighting a desperate rear guard action against those people who reasonably question whether the Fed has been all it's cracked up to be. The threat is real; Fed Governor Kevin Warsh on Friday stated that Fed credibility would suffer if independence was lost. Although this statement raises other questions (namely, "what credibility??), it is indicative of the FOMC's mood. If you think Bernanke is going to tighten rates meaningfully when Unemployment is near 10%...or 9%...or 8%...and risk having the Fed's independence stripped, I think you ought to think again. Of course, this means that the de facto independence of the Fed is questionable, but anyone who thinks that this is a fight the Fed should pick shortly after the bottom of the worst recession in at least 30 and maybe 80 years, please raise your hand. I didn't think so.

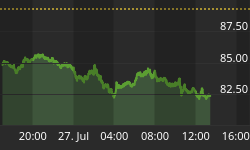

After a rough week for bonds, the South Korean news helped tame rates into the weekend. June 10y Note futures closed +13/32nds, with 10y yields down to 3.85%. Swap spreads widened another basis point or so, continuing the so-far-pretty-tepid bounce.

On Monday, Personal Income and Consumption Expenditures for February will be released (Consensus: +0.1% for PI, +0.3% for CE; +0.1% month/month core PCE with Y/Y core PCE falling to 1.3%). Although the development of core PCE is important, for this week it is far more important how the market gets positioned for Payrolls on a Friday that will likely have thin trading conditions (and stocks completely closed).

A Word About Current Value In Long TIPS

When investors are thinking about what assets to include in their portfolios, they obviously care about both risk and return. Of course, the problem is that they care about a priori risk and return, which are unknowable, and so tend to populate portfolio allocation simulations with estimates of long-run returns that are no better than guesses (we tend to have a better sense of long-run variances, although what causes problems there is that the distribution is not normal). This is why equities are so dominant in many portfolios, despite their evident short-term risk: generally, investors make one of three key errors in looking at long-run equity returns:

- They use long-run historical nominal returns to form the estimate. Investors shouldn't care about nominal returns at all, so this is clearly incorrect.

- They use long-run historical real returns. This is better, but it neglects the fact that most historical periods which terminate in the last decade-plus will also reflect multiple expansion as a source of return. There is no good reason to expect that the multiple expansion of the last eighty years will repeat over the next eighty.

- They use a tortured interpretation of the Capital Asset Pricing Model to back out high expected returns for equities. "Stocks are riskier; therefore, they should have a higher return." The CAPM isn't meant to be a causal model but rather an observation about how capital assets should be priced. If riskiness implies more return, then lottery tickets should be the best investment.

But we can look at long-term data in a more thoughtful way and get a better sense for what a fair return to equities is, in the long run. Brad Cornell and Rob Arnott wrote a short article ("The 'Basic Speed Law' for Capital Markets Returns") that pointed out three important long-term truisms. First, the long-run growth rate of per-capita GDP in the U.S., a measure closely related to productivity growth, has been around 2% for the last 100 years. Second, if the real economy is growing around 2% per capita in the long run, then earnings in the corporate sector must also be limited to roughly that growth (since otherwise it would soon become larger than the economy itself). And third, if the growth of earnings is limited similarly, then stock price index growth must be limited to something similar as well, net of valuation changes.

The version of the chart which appears below is sourced from Census, BEA, and Robert J Shiller data, and updated through the end of 2009. Over the last 80 years, the compounded growth rate of real per capita GDP has been 2.1%; for real earnings it is 2.6%; and for stock prices it is 1.8%. However, those rates are computed using arbitrary end points - December 1929 and December 2009. A better way is to run an exponential regression, and on the chart the straight lines are the results of that regression (the line appears straight because the axes are loglinear, so the regression line is linear in log space). The growth rates then are 2.25% for real per capita GDP, 1.74% for real earnings (n.b., if you take out 2008Q4-2009Q3, the coefficient is 1.95%), and 2.87% for the real stock price growth rate.

I hope you like 2%, because that's what you're gettin'.

Now, 2.87% as a long-run real growth rate for equities doesn't sound great, but it's actually even exaggerated because over that period, equity multiples expanded from 13.3x earnings to 21.6x earnings, so a bunch of that return is coming from multiple expansion that may not repeat. If the current multiple is fair (I think it's high, but let's be generous), then the long-run expected return to equities ought to be similar to the long-run expected growth in earnings, which is limited to the long-run growth in GDP per capita. Or, roughly, 2-2.25% (There really isn't a lot of difference here, actually; real GDP uses the GDP deflator to measure price inflation, while real earnings uses CPI; the latter is generally about 0.25% or so higher, so these are essentially both 2%, if you use CPI, or 2.25%, if you want to use the deflator.)

That's what you can expect to get from equities in the truly long-run. With that long-run growth, of course, comes a ton of volatility. Meanwhile, you can get a 30-year real yield of 2.17% from TIPS, with much less volatility (and no volatility at a horizon equal to the duration of the bond). Moreover, remember TIPS pay based on CPI, which is the "faster" of the two inflation measures used above.

So, unless you are into market timing, TIPS are currently priced to produce a long-run real return equal to stocks, with less volatility. That's a decent deal! If we get a big rate sell-off, that deal may get better still, but while the short end of the TIPS curve doesn't look terribly attractive the long end remains reasonable.