What Wall Street really needed right now, as they attempt to mobilize against the potentially-disastrous Volcker Rule and any number of other populist nostrums, was for one of their number to be caught with its hand in the cookie jar. To be sure, Goldman generally acts as if it owns the cookie jar, but pride goeth before a fall and...whoops.

Of course, Goldman will survive and probably settle for what amounts to a slap on the wrist, as will any other firms later charged by the SEC in similar actions; I suspect this is mostly about the government gaining a tempo¹ over the finance industry.

Prior to the SEC's announcement, it was looking like another day of the same in equities. Indices were lower overnight, and bonds considerably higher, as further details on the latest Greece 'deal' makes it appear that it isn't really much of a deal, and as investors start to must about the impact on commerce of the dumping of Icelandic ash all over Europe, grounding planes across the continent. Housing Starts were stronger-than-expected, while Michigan Sentiment actually declined unexpectedly, so you can get whatever you want out of the data. But once the market opened, sure enough stocks rallied. It is disturbing when this happens every day, because it implies that investors have come to fear "not being long" more than they fear losing money because the market falls. If we are not already at that stage, we were getting there.

But after the SEC announcement that it is suing Goldman, the market went into retreat...not just Goldman, and not just financials, but lots of sectors that have nothing to do with them. Nearly 7 stocks on the NYSE fell for every 1 that rose. That would seem to indicate some people are treating this as if they have suddenly concluded that "aha! This is the thing that might do it." (It was interestingly not on the list of worries I posted yesterday, which is probably a sine qua non for it actually being an important event.)

CNBC provided its usual humorous background chatter, with talking heads debating whether stocks were down because "they" (retail investors) "feel they don't have a fighting chance on Wall Street." "This is their big fear, that the game is rigged." Come on, folks, the S&P was down 1.25% at the time (-1.6% at the close), after being up around 80% from the lows a year ago. It is probably true that retail investors in aggregate don't have a fighting chance to be active traders against professionals, but...this is presently a hiccup. Sometimes the market goes down, even in bull markets.

That being said, an overextended market doesn't need a lot of encouragement to pull back, and so perhaps this turns into a modest correction. If it does not - if investors jump right back in to "buy the dip" on Monday - then the psychology really is starting to get over-the-top and bubbly.

Curiously, bonds responded aggressively to the selloff in stocks, +22/32nds on the day for TYM0 with the 10y yield all the way down to 3.77%, and the VIX also jumped from 15.89 to 18.36. These both seem to be outsized reactions to a fairly minor selloff in stocks, and this might indicate a stronger undercurrent of risk aversion is at work (finally). Oil prices dropped $2.27, but that is probably unrelated: commodities generally were mixed.

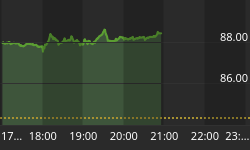

I am still medium-term bearish on bonds. The market has now rallied back enough that an imminent breakdown is unlikely, but as the chart below (source: Bloomberg) shows, bearish fixed-income traders can consider leaning short at this level with risk fairly well-defined. Anything more than a handful of basis-points of further rally, however, would make me near-term neutral at least (and if we were not in a fairly bearish seasonal period, I'd probably be turning bullish on a break through).

Bearish traders can consider leaning on this level with technical value

There is no data of note on Monday (just Leading Indicators, which is an amalgamation of lots of indicators we have already seen), so technical factors and news events (further SEC filings, further Greece news) will be more important.

Footnote:

¹This is a term from chess (wikipedia entry). The side that has the initiative is the one which is making the moves to force the opponent's response, essentially driving the action; when one side gains a tempo he is more in control of the game than he was previously.