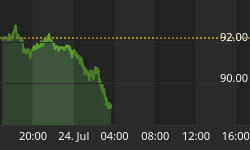

I'll be the first to admit that I do not know how the Greece debt crisis/saga will end. What I do know is that when the rating agencies first warned on Greece's debt back in December this should have been when policy makers urgently started to develop contingency options (assuming some were not already in place). And while delaying any bailout may well have been a ploy squeeze as much cooperation from Greece as possible, it is clear with panic spreading from the debt markets to the equity (and countless other) markets that this tactic has been played in full. The 16 euro-zone leaders are meeting today to try and finalize Greece's bailout and stop contagion.

For his part, ECB President, Jean-Claude Trichet, said yesterday that the bank was not discussing the possibility of purchasing eurozone government debt - "We did not discuss the matter. I have nothing more to say on it". If Mr. Trichet's intentions were to frighten already spooked investors, bravo!, although Trichet may have done well to remember how quickly Treasury Secretary Paulson backpedaled when he tried to draw the bailout line in the sand with Lehman (it took 2-days before AIG arrived).

"Either the governing council is guilty of gross dereliction of duty, or the ECB is treating journalists and analysts as ignorant children". Lombard Street's Gabriel Stein

Suffice to say, it is definitely time for all parties concerned to realize that the 11-year old experiment that is the Euro is unlikely to last another 11-years without dramatic changes. With many looking for a Greece default/debt restructuring in the years ahead and the reality that any future bailouts efforts could be considerably larger than Greece, exactly what 'changes' are required to keep the euro intact are not known at this time...

Stub Quote Nonsense Not Stubby Fingers

One of the first explanations of yesterday's dramatic plunge in the U.S. markets was that a trader pressed 'B' instead of 'M' (igniting the sale of a billion+ shares instead of million+ shares in, reportedly, PG). This theory, while still being investigated, does not explain why Accenture Plc, Exelon, and Philip Morris each declined by more than 90% and why the Nasdaq has cancelled trades in hundreds of stocks that crashed by 60% or more.

Common sense suggests that regulators should have quick access to exactly who, or what, was doing the selling as stocks plunged and/or why certain pockets of the market were seemingly completely bereft of any buying. Moreover, if the regulators do not have immediate access to this information the question becomes, why not? Perhaps the SEC will file another lawsuit to divert attention away from its ineptness on this front. After all, it was arguably the SEC that was at least partially responsible for the severity of yesterday's meltdown:

"Rapid-fire orders trigger what the NYSE calls liquidity replenishment points, or LRPs, shifting the market into auctions. While the system is designed to restore order on the Big Board, trading is so fast during times of panic that orders routed past the exchange may swamp other venues and exhaust buy orders....

That's when prices may plummet as orders execute against so-called stub quotes from market makers. Brokers can set the quotes as low as a penny a share because they're never expected to be used."

And why are stub quotes, which are never expected to be used, placed at all? Because market makers need to deploy such bids to comply with rules and requirements. In the case the Nasdaq, before it filed to relax the rules (SEC filing) a market maker had to maintain quotes that were "reasonably related to the prevailing market". This is no longer the case and, as TheStreet reported back in August 2007, there have been instances when both the Nasdaq and NYSE Arca both cancelled penny per share trades in an illiquid market (i.e. Comfort USA in August 2007). It may be a stretch to conclude that regulators made a big mistake by allowing 'stub quotes' to take the place of reasonable market making: tighter spread alone may not have prevented yesterday's debacle. However, the question of whether market makers are trying to make markets or manipulate markets has always been around, and deserves to acquire greater attention thanks to the stub quotes issue.

While stub quotes help explain why ridiculously low bids were in place, they do not explain why anyone/thing was dumping stocks at such low levels. Attempting damage control, NYSE Euronext Chief Operating Officer, Larry Leibowitz, told Bloomberg that the 'selloff snowballed because of orders sent to venues with no investors willing to match them.' What Mr. Leibowitz neglected to mention is that if no 'matching' took place stocks would have simply stopped trading. We know this was not the case. Rather, and as Mr. Leibowitz concedes, someone or something continued to trade even as chaos took over:

"Electronic markets actually traded all the way through the slower New York Stock Exchange markets where we were trying to slow down trading."

Drawing on the stub hub hits and lighten fast wave of sell orders, many have speculated that computerized trading was to blame. Perhaps the computers, which are not capable of panic, were informed to place sell orders as low as a penny simply because they're never expected to be used...

Worry not! If history holds the SEC will get to the bottom of things, debate the matter for a decade or so, and then proclaim that market makers must maintain quotes that are reasonably related to the prevailing market. Until then the manipulation market making many investors have come to know and love persists, and will probably continue to do so for a lot longer than the euro experiment.