Oil Market Summary from: 05/10/2010 to 05/14/2010

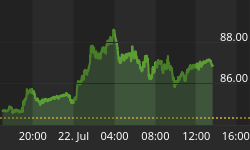

Crude oil prices plunged nearly 4% on Friday and were off almost 20% from their 18-month high less than two weeks ago, as the euro continued to lose ground against the dollar and U.S. oil inventories continued to build.

The benchmark West Texas Intermediate contract settled at $71.61 a barrel on Friday, down $2.79 on the day, compared with $75.11 a week earlier, and the lowest price in three months. Oil prices hit an 18-month high of $87.15 on May 3.

The euro on Friday reached its lowest point against the dollar since October 2008, falling below $1.24 from just above $1.25 on the previous day. As the dollar strengthens, it puts downward pressure on oil prices.

Oil futures fell below $71 a barrel in intraday trading, and analysts now feel that prices may test the $70 threshold. OPEC has repeatedly said it would like oil prices to stay in a range of $70 to $80 a barrel, and the oil cartel might be prompted to cut production if prices fell below $70.

The buildup of inventories continued to weigh on the Nymex contract. The European benchmark, ICE's Brent crude, which normally trades at a discount to WTI, settled at $77.18 on Friday.

The weekly inventory report from the U.S. Energy Information Administration on Wednesday showed an increase of 1.95 million barrels in oil stocks. In Cushing, Okla., the delivery point for Nymex crude, inventories rose by 784,000 barrels to a record 37 million barrels.

The oil price decline on Friday came in spite of an increase in the Reuters/University of Michigan consumer sentiment index for May. The index rose to 73.3 from 72.2 in April, indicating a possible pickup in demand.

Also on Friday, it was announced that U.S. retail sales rose 0.4% in April, to $366.4 billion - the seventh straight month sales have risen.

Pressure on the euro continued even though European leaders last weekend agreed on a nearly $1 trillion package to back euro zone members and the European Central Bank reversed its earlier position and agreed to buy member's government bonds to counter selling pressure in international bond markets.

While the oil spill in the Gulf of Mexico has seemed to have little direct effect on prices, President Barack Obama pledged on Friday that the U.S. government would review its regulatory procedures for oil companies in the wake of the accident.

Earlier in the week, the administration said it would split up the government agency responsible for offshore drilling so that supervisory and enforcement responsibilities would be separate from leasing and revenue collection.

By Darrell Delamaide for Oilprice.com who offer detailed analysis on Crude oil, Geopolitics, Gold and most other Commodities. They also provide free political and economic intelligence to help investors gain a greater understanding of world events and the impact they have on certain regions and sectors. Visit: http://www.oilprice.com