Summary of Index Daily Closings for Week Ending July 2, 2004

| Date | DJIA | Transports | S&P | NASDAQ | Jun 30 Yr Treas Bonds |

| June 28 | 10337.09 | 3177.97 | 1133.52 | 2019.82 | 104^28 |

| June 29 | 10413.43 | 3184.71 | 1136.23 | 2034.93 | 105^14 |

| June 30 | 10435.48 | 3204.31 | 1140.84 | 2047.79 | 106^12 |

| July 1 | 10334.20 | 3171.88 | 1128.98 | 2015.50 | 106^26 |

| July 2 | 10282.83 | 3146.17 | 1125.38 | 2006.66 | 108^01 |

| SHORT TERM FORECAST (Next Two Weeks) | ||||

| TREND | PROBABILITY | Legend | ||

| Substantial Rise | Low | |||

| Market Rise | Medium | Very High | 80% | |

| Sideways | Medium | High | 60% | |

| Market Decline | High | Medium | 40% | |

| Substantial Decline | Medium | Low | 20% | |

| Very Low Under | 20% | |||

| INTERMEDIATE TERM FORECAST (Next 12 Weeks) | ||||

| TREND | PROBABILITY | Substantial | 800 points+ (DJIA) | |

| Substantial Rise | Low | Market Move | 200 to 800 points (DJIA) | |

| Market Rise | Medium | Sideways | Up or Down 200 (DJIA) | |

| Sideways | Medium | |||

| Market Decline | High | |||

| Substantial Decline | High | |||

This week the Dow Jones Industrial Average closed down 89.01, in line with last week's Short-term TII reading of negative (-34.00). Markets marked time before June 30th, watching to see how the Iraq changeover would work, wondering what the Fed would do with interest rates, while at the same time holding onto second quarter gains for rosy quarter-end reporting. That behind them, they largely ignored the usual pre-Fourth of July holiday euphoria and sold off the second the calendar flipped. The sell-off occurred a few days earlier than we anticipated and we believe markets will continue that trend when folks come back from the long weekend. July portends to be a clean-out-the-attic month.

The DJIA is turning south and about to bust below its 50 day moving average once again. Its MACD fell below zero and is heading down. The Relative Strength Indicator has plenty of room to fall from here as it is nowhere near oversold territory. For those keeping score at home, the Industrials never surpassed their April 6th high of 10,570 which means its Bearish pattern of declining tops remains intact. Ditto for the S&P 500 and ditto for the NASDAQ Composite except its MACD remains just a hair above zero - but is turning negative.

| Equities Markets Technical Indicator Index (TII) ™ | ||||

| Week Ended | Short Term Index | Intermediate Term Index | ||

| Feb 27, 2004 | (31.00) | (20.17) | Scale | |

| Mar 5, 2004 | 16.00 | (17.17) | ||

| Mar 12, 2004 | ( 9.00) | (14.70) | (100) to +100 | |

| Mar 19, 2004 | (12.00) | (27.60) | ||

| Mar 26, 2004 | 73.00 | (38.35) | (Negative) Bearish | |

| Apr 2, 2004 | (3.00) | (35.61) | Positive Bullish | |

| Apr 16, 2004 | (43.00) | (29.90) | ||

| Apr 23, 2004 | 94.00 | (22.69) | ||

| Apr 30, 2004 | (33.25) | (34.88) | ||

| May 7, 2004 | (28.75) | (47.75) | ||

| May 14, 2004 | (25.75) | (66.45) | ||

| May 21, 2004 | 22.00 | (67.23) | ||

| May 28, 2004 | ( 3.50) | (48.48) | ||

| June 4, 2004 | (55.75) | (34.07) | ||

| June 11, 2004 | (77.75) | (25.92) | ||

| June 18, 2004 | (40.25) | (31.17) | ||

| June 25, 2004 | (34.00) | (26.10) | ||

| July 2, 2004 | (41.50) | (27.64) | ||

This week the Short-term Technical Indicator Index comes in at negative (41.50), indicating a market decline is probable. This indicator is a useful predictor of equity market moves over the next two weeks, both as to direction and to a lesser extent strength of move. For example, readings near zero indicate narrow sideways moves are probable. Readings closer to +/-100 indicate with a higher degree of confidence that an impulsive move up or down is likely over the short run. Market conditions can change on a dime, or the Plunge Protection Team can come in and temporarily stop market slides, so it may be unwise to trade off this weekly measured indicator.

The Intermediate-term Technical Indicator Index is useful for monitoring what's over the horizon - over the next twelve weeks. It serves as an early warning system for unforeseen trend changes of considerable magnitude. This week the Intermediate-term TII comes in at negative (27.64).

We presented and analyzed the Broker Dealer Index ($XBD) in June 30th's Mid-week Market Update (see archives at www.technicalindicatorindex.com) showing a large Bearish Head & Shoulders Top formation with a downside target of 92. This Index was above 148 as recently as March 2004. Prices continue to trace out a 4th wave triangle as part of its Right Shoulder. Even worse, if you examine the Right Shoulder carefully, it is forming another Bearish Head & Shoulders Pattern within the Right Shoulder. This development is ominous for stocks as this index is a proxy for retail stock transactions.

As for the Consumer, who accounts for 70% of GDP, the Retail Holders (RTH) average has formed a massive spread-eagle Bearish Head & Shoulders Top. The Morgan Stanley Consumer Index ($CMR) has formed a Huge Triple Top. And the Dow Jones Retail Index ($DJTRETE) has formed a Bearish Head & Shoulders Top with its MACD breaking down hard.

The next set of charts offer analogs between three famous crashes of the past eighty years and the current price setup in the Dow Jones Industrial Average. The results are sobering.

The above chart compares the price action leading up to the stock market crash of 1929 with today. When I first drew up this analog, the top for 1929 was a bit more abrupt than today's. But that stands to reason since the Fed is pumping M-3 into the system like gangbusters today, and did not back in 1929. Huge liquidity infusions would have the affect of prolonging a top. When I adjusted 1929's top slightly, by extending the time between prices at point A and point B by a mere seven weeks, this analog correlated extremely well, as depicted above. Except for extending the top by seven weeks for 1929, all other prices and times are actual, unadjusted.

The next chart on page 4 compares the price and time patterns for today with 1987. If we view 1987's as a smaller scale of today's move, a model so to speak, the two patterns compare favorably. What is particularly striking to me is the similarity between the topping patterns then and now. Both patterns experienced long ascensions, without corrections of any significance, until topping. Then each experienced a gentle sloping pattern of descending tops. Out of nowhere, from a gentle sloping decline, the DJIA crashed violently in 1987. You would have never expected a crash based on the price patterns of 1987 or 1929, yet they occurred.

The third analog presented compares now with 2002. These analogs were on the money until June when we are getting a small rally (still within descending tops) in 2004 whereas the crash had begun in 2002. Still, even in 2002, there was a minor correlative rally of similar slope, but differing time and extent. This breakdown can be explained by the April/May 2004 crisis liquidity pump by the Fed.

What's the point of these three analogs? The point is, the psychological condition of the present equity market as measured by the Dow Jones Industrial Average is fragile. The pattern tells us that crashes can occur from this type of price action over the period of time we have experienced. These analogs do not guarantee we are about to have a stock market crash, but they do tell us that we are in a position of high risk to have one. One bad news event, one unexpected financial disaster could trigger a massive sell-off in equities. We are on thin ice. The patterns indicate widespread distribution of stocks from strong hands to weak hands, long price run-ups without normal healthy corrections, overvalued price-earnings ratios, and complacent sentiment, a time that is ripe for a 15 percent plus correction, a swift, vertical descent. We've shown you five Asian markets that are in the midst of crashes as we speak (see issues 59 and 61 in the archives of www.technicalindicatorindex.com). The Gold and Silver stocks are in the midst of crashes. The Semiconductors are crashing as well. To see other markets crashing at a time when the DJIA is in a pattern analogous to three other major crashes is nothing less than a flashing neon light. Add to this the upside Dow Theory Bearish non-confirmation, the ominous set-up pattern Three Peaks and a Domed House (see Tim Wood's outstanding newsletter at www.cyclesman.com for the details of this ominous baby), the stratospheric, crash-territory readings of the S&P 500 to VIX ratio, and we've got one major league Bearish set-up, the likes of which have not been seen in ages.

And that's just the technical analysis. The fundamentals have their own problems. Rising interest rates inside a debt bubble economy, record derivatives positions, carry-trade unwinding risks, Fannie Mae and Freddie Mac balance sheet risks, Middle East political tensions and a war that won't let our soldiers go home, unsatisfactory jobs growth, wasted tax reductions offset by rising fuel charges, rising inflation, declining support for a Republican incumbent president, and on and on.

The charts on the next page compare the Dow Transportation Average with the Dow Industrial Average. Both have completed tops by virtue of terminating patterns for their respective primary degree Elliott Waves 2 up of an eventual 5 down (1 down, 2 up, 3 down, 4 up, 5 down).

The Trannies have completed a Parabolic Spike Top, a reliable termination pattern, representing speculative excess, a final blow-off peak. We saw one earlier in the year in Silver. Parabolic ascension does not lend itself to moderate declines or soft landings. These vertical tops lead to crashes - vertical declines. Worse, the subsequent crash occurs within a very short time duration from when the vertical rise is recognizable. Near the top of this rise, the last week of June, volume dropped off markedly, sort of like being on a roller coaster where your speed slows at the top of a hill just prior to a breathtaking reversal down. Given the nearly 2 percent decline in the Trannies on July 1st and 2nd, it appears the descent has begun. The Transportation Average spike also counts well as a wave 5, completing an impulse five-wave C up of primary degree 2 up.

The Dow Industrials also appear to have completed a top, but by virtue of a terminating failed 5th wave of a final wave C up. These patterns of failure are often seen in 5th waves of impulsive waves (which we've had since March 2003). According to Elliott Wave technician Glenn Neely, Mastering Elliott Wave, Windsor Books, 1990, he states on page 11-4, "As a general rule, 5th wave Failures are only possible when the 3rd wave is the Extended move. The 4th wave should be the most complex of the two corrective phases. Wave 4 should retrace more of wave 3 than wave 2 does of wave 1." He further states, "A 5th wave can Fail in an Impulse pattern only under one of the following circumstances . . . If the Impulse pattern (containing the Failure) is the c-wave of one (and only one) larger Degree." The current 5th wave failure in the Dow Industrials meets all these requirements. Adding to the evidence that the Industrials have completed their rally since March 2003 is the Fibonacci phi relationship between the number of trading days from the beginning of the Bear market to the bottom of primary degree Elliott wave 1 down as compared to the number of trading days from 10/9/02, the wave 1 bottom, to June 23, 2004, the primary degree Elliott Wave 2 Top. From 10/14/00 to 6/23/04 there were 1115 trading days. From 10/14/00 to 10/9/02 there were 687 trading days. From 10/9/02 to 6/23/04, there were 428 trading days. 687 (+2) is a Fibonacci .618 of 1115. 428 (-2) is .382 of 1115. This phi relationship defining tops and bottoms has occurred for every single top or bottom since the Bear Market began. It would stand to reason that the phi mate of the very important 10/9/02 low, primary degree wave 1, would be a very important top, primary degree wave 2. This, it would seem, we have.

Of course, we also continue to operate under a Dow Theory "Sell" signal, which has been subsequently followed by a Bearish Dow Theory upside nonconfirmation. The fact that wave 5 failed to exceed wave 3 of C of 2 up in the Industrials, but did not fail in the Trannies, gives us this Dow theory nonconfirmation. As of Friday's close, the Industrials were a very large 455 points away from confirming the Trannies' latest up move. Odds are decreasing by the day that this is going to occur. In fact, in our June 25th issue, no. 61, we showed that over the past five years - encompassing the entire Bear Market - every single time we had a Transportation Average/Industrial Average price divergence, a stock market crash occurred shortly thereafter - within two to three months.

Kudos should be given to Zoran Gayer whose Elliott Wave analysis is published weekly on www.safehaven.com for being one of the first to call the 5th wave terminating failure in the DJIA. He called this many months ago, long before it was apparent.

The Economy:

The value of technical analysis is that it reads the fundamentals before they happen. Markets discount the future, and technical analysis offers us the tools to read the market's language. That said, we are starting to see deterioration in the fundamentals. Here's what we learned this week:

Construction Spending rose 0.3 percent in May after declining a revised 1.2 percent in April. That's a net decline over those two months. I continue to see increasing corporate office vacancy signs popping up in the Philadelphia area as more and more building go up. Feels like the top of the real estate market.

The Commerce Department reported that Consumer Spending rose 1 percent in May. While that may seem strong, we were told that half of the increase was due to inflation, not unit purchases. That may change soon as the Federal Reserve raised short-term interest rates by 25 basis points. Consumers who have taken out Home Equity lines will see an increase in their bills next month. This, combined with higher gasoline prices, will act like a tax and reduce disposable income.

The Chicago Purchasing Managers's Index of Manufacturing in the Chicago area showed a marked decline to 56.4 in June from 68 in May. That's a seventeen percent decline. Still, above 50 indicates growth. The National Association of Supply Management's ISM U.S. Index came in at 61.1 for June, down from 62.8 in May, and the weakest reading in eight months. Inside the number, new orders fell 23.6 percent (in one month!) and production slowed by 24 percent. Dismal.

Initial Jobless Claims rose again, reported to be 351,000 for the week ended June 26th according to the Labor Department. Friday's Non-farm Payrolls number disappointed, reported up 112,000, far below previous monthly figures. Construction and manufacturing suffered.

This is all on the heels of a big drop in Durable Goods Orders for April and May.

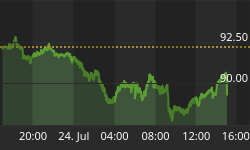

Above is a chart (courtesy of www.stockcharts.com) of the Philadelphia Semiconductor Index ($SOX) showing a massive Bearish Head & Shoulders pattern. Pretty much everything we buy these days has a chip in it, so this pattern portends badly for spending. By measuring the distance from the Head to the Neckline, and subtracting that from the value at the Neckline, we get a minimum downside target of 290. The Elliott Wave count indicates prices are finishing up a symmetrical triangle wave 2 that will lead to a wave 3 push south. After 3 down should be a 4 up correction followed by a wave 5 down into the 290 area.

The Moving Average Convergence.Divergence has reached zero and is breaking down. Since the Relative Strength Indicator is not oversold, there is plenty of room for prices to fall.

Money Supply, the Dollar & Gold:

M-3 declined slightly during the latest reporting week, down about $10.4 billion on a seasonally adjusted basis. Non-seasonally adjusted was down $50.8 billion. M-3 declines can come from either the Federal Reserve selling securities to the economy, or by a reduction in total borrowing. Since May 17th, M-3's growth has been stagnant, up a mere $16.3 billion over five weeks, an annualized growth rate of 1.8 percent. So it appears that the Fed caused or allowed massive infusions in liquidity during the April/ May period when Asian equity markets collapsed and the U.S. equity markets slid. Then, given the recent equity market rally that took the DJIA from 9,852 on May 12th to10,487 on June 25th, 2004, the Fed took their foot off the accelerator and was content to let M-3 plateau. As we have shown in prior issues, plateaus generally lead to equity market corrections.

The Trade-weighted U.S. Dollar looks as if it is headed for the low 80s and perhaps even the 70s. The chart below shows a Bearish Head & Shoulders that formed under the roof of its long-term declining trend-channel. The Right Shoulder has completed and prices have fallen below the neckline, confirming the validity of the pattern. The minimum downside target is the 84 area with more downside potential. Both its 50 day and 200 day moving averages are falling - Bearish. The RSI is not yet at oversold levels and the MACD is breaking down. Not good.

The Gold Mining Stocks ($HUI) chart shows that price action for the past week merely moved closer to the tip of the Symmetrical Triangle, perfectly along the borders. This continuation pattern is just about completed and we look for a breakout lower over the next week to ten days. The Elliott Wave count considers this triangle as a corrective Wave 4, meaning next for the HUI is a sharp decline wave 5. If wave 5 tends toward equality with wave 1, then expect a drop of about 45 points from wave 4, someplace below 150. The down trend-channel also points to that target price. The overall price pattern for the past year is a textbook perfect Bearish Rounded Top. With prices due east (picture a globe), the next direction is a near vertical move south. That would coincide with our crash forecast for most major equity averages starting over the next several weeks. Wave 5 down will be another crash for this average, the second since April 2004, something around 20 to 25 percent below current levels. It is interesting that the HUI's pattern is in tune with stock averages rather than the precious metals at this time. The MACD is breaking down below zero.

Gold the Metal has formed a Bearish Double Top, and for the first time in three years, its 50 day moving average has declined decisively below its 200 day moving average. Gold must rise for it to stay inside its 3 year long-term rising trend-channel. It cannot afford to move sideways or it could find itself breaking below the trend. To be honest, it looks like Gold is at great risk of heading lower. How can that be, given our forecast for a declining dollar? It could be that Gold is sensing massive deflation on the way, perhaps in the form of worldwide equity markets crashing and economies slowing. The Fed would respond with massive infusions of liquidity, that event is discounted by the trade-weighted dollar pattern, but perhaps it will only be the U.S. fiat currency that takes a dive, not the Euro.

Bonds and Interest Rates:

Just going by the charts, about the same time that most financial assets will be deflating, the pattern for U.S. Treasury Notes indicates they will be rallying. The ten year note should reach somewhere between 111 and 113.75 to complete wave 2 up.

This would make sense if equity markets are crashing, a flight to quality driving U.S. Treasury notes higher. But the rally should be short-lived as Elliott Wave 3 down takes force. Wave 3's sell-off could occur from Foreign Investor selling, concerned about the dollar as the Fed responds to crashes with cargo planes full of M-3. Sounds like a novel, I know, but all the charts appear to be threading together a coherent Crash scenario.

The short-term rally scenario is supported by a rising MACD, now above zero, and an RSI that is not overbought.

U.S. Treasuries have been moving inversely to equities over the past couple of days, so it stands to reason this relationship will continue. Plus we know that the bond genius of the world, Pimco's Bill Gross is buying Treasuries. Asian equity markets continue to plummet, so for the moment, U.S. Treasuries seem like a safe place to be. Thus, why shouldn't they rise?

Bottom Line:

The deflationary, equity market crash scenario is coming together at this time. Even M-3, the Fed's best tool to boost markets, has been sluggish of late. That may not be by design, but rather the velocity of money may be stalling. There is no guarantee that equities are about to crash, but the charts and patterns of most major averages suggest that if there ever was a time when markets are fragile, when markets could plummet from some trigger event, it is now. The Three Peaks and a Domed House pattern monitored so well by Tim Wood (www.cyclesman.com) is calling for an imminent crash. Should the number of new 52 week lows rise to over 90 and the number of new 52 week highs remain over 90 and the McClellan Oscillator drop below zero - a very likely scenario on the next big decline day, we'll also have another stock market crash warning, a Hindenburg Omen, so named and monitored by Kennedy Gammage (the Richland Report, P.O. Box 222, La Jolla, CA 92038). Caution is warranted.

"But He was pierced through for our transgressions

He was crushed for our iniquities

The chastening for our well-being fell upon Him,

And by His scourging we are healed.

All of us like sheep have gone astray,

Each of us has turned to his own way;

But the Lord has caused the iniquity of us all

To fall on Him."

Isaiah 53: 5, 6

Please check out Nelson Hultberg's excellent article "Cornered Rats and the PPT" in the Guest Article section at www.technicalindicatorindex.com. In it he explains how the Plunge Protection Team works.

Special Note: Be sure to register under the subscribers' section at www.technicalindicatorindex.com for e-mail notifications of our new mid-week market analysis, usually available on either Tuesdays or Wednesdays. These midweek updates will only be available via e-mail and in the future will not be posted on the web.

| Key Economic Statistics | ||||||||

| Date | VIX | Mar. U.S. $ | Euro | CRB | Gold | Silver | Crude Oil | 1 Week Avg. M-3 |

| 1/30/04 | 16.46 | 87.48 | 124.42 | 262.10 | 402.9 | 6.25 | 33.05 | 8901.7 b |

| 2/06/04 | 16.00 | 86.15 | 126.83 | 260.50 | 403.6 | 6.27 | 32.43 | 8891.6 b |

| 2/13/04 | 15.62 | 85.68 | 127.25 | 264.85 | 410.8 | 6.58 | 34.56 | 8904.2 b |

| 2/20/04 | 16.05 | 87.40 | 126.96 | 264.50 | 397.5 | 6.53 | 34.25 | 8942.7 b |

| 2/27/04 | 14.53 | 87.89 | 124.52 | 273.90 | 396.8 | 6.71 | 36.16 | 8962.4 b |

| 3/05/04 | 14.52 | 88.75 | 123.28 | 274.00 | 401.6 | 6.99 | 37.26 | 8974.1 b |

| 3/12/04 | 18.21 | 89.60 | 121.80 | 272.00 | 395.6 | 7.06 | 36.19 | 8964.0 b |

| 3/19/04 | 19.15 | 88.56 | 122.47 | 280.20 | 412.7 | 7.56 | 37.62 | 9005.8 b |

| 3/26/04 | 17.12 | 89.30 | 120.90 | 278.25 | 422.3 | 7.71 | 35.73 | 9015.3 b |

| 4/02/04 | 15.81 | 88.80 | 121.12 | 280.00 | 421.1 | 8.15 | 34.39 | 9071.5 b |

| 4/08/04 | 16.38 | 89.82 | 120.56 | 284.00 | 419.9 | 8.09 | 37.14 | 9059.6 b |

| 4/16/04 | 15.00 | 90.18 | 119.50 | 276.75 | 401.6 | 7.14 | 37.74 | 9075.0b |

| 4/23/04 | 14.01 | 91.34 | 118.18 | 267.50 | 395.7 | 6.16 | 36.46 | 9080.8 b |

| 4/30/04 | 16.69 | 90.76 | 119.70 | 270.75 | 387.5 | 6.07 | 37.38 | 9128.2 b |

| 5/07/04 | 18.13 | 91.30 | 118.83 | 270.40 | 379.1 | 5.58 | 39.93 | 9185.3 b |

| 5/14/04 | 18.47 | 91.81 | 118.69 | 267.00 | 377.1 | 5.72 | 41.38 | 9187.5 b |

| 5/21/04 | 18.44 | 90.53 | 120.05 | 268.75 | 384.9 | 5.87 | 39.93 | 9233.5 b |

| 5/28/04 | 15.52 | 88.98 | 122.10 | 276.25 | 394.0 | 6.11 | 39.88 | 9207.7 b |

| 6/04/04 | 16.57 | 88.50 | 122.93 | 274.75 | 391.7 | 5.81 | 38.49 | 9212.3 b |

| 6/11/04 | 15.10 | 89.23 | 121.01 | 269.25 | 386.6 | 5.78 | 38.45 | 9221.3 b |

| 6/18/04 | 14.95 | 89.41 | 121.17 | 267.75 | 395.7 | 5.98 | 39.00 | 9260.2 b |

| 6/25/04 | 15.19 | 89.22 | 121.41 | 270.75 | 403.2 | 6.12 | 37.55 | 9249.8b |

| 7/02/04 | 15.15 | 88.18 | 123.09 | 265.50 | 398.7 | 6.01 | 38.39 | - |

Note: Dollar, CRB, Gold, and Silver down. Euro and oil up.