U.S. stock futures markets posted daily closing price reversal tops on Thursday, sending a signal that a correction may be looming. It is going to take a break through Thursday's lows however to confirm the formation which would then trigger the possibility of a 2 to 3 day break or 50% correction of the last rally.

Early in the trading session, good news from J.P. Morgan underpinned U.S. equities for a short-time before the markets caved in due to pressure from the weakening economy.

On Wednesday the Fed released a less than stellar outlook for the economy, but it was Thursday's bearish inflation and manufacturing reports which encouraged investors to take profits, driving stock prices lower.

Throughout this week, stock prices have been driven higher by investor optimism and a bullish outlook for strong earnings. Investors for the most part chose to ignore economic data, but the Fed's outlook yesterday and today's reports finally made them sit up and take notice. The bottom line is, despite better than expected earnings during the second quarter, the economy is losing steam. Traders could begin pricing in the prospects of a double-dip recession, thereby pressuring equities.

September Treasury Bonds surged on Wednesday following the release of the Fed's dismal outlook for the economy. This drop in yields was a strong sign that interest rates were headed lower and that the Fed would keep its benchmark interest rate low for a prolonged period of time.

On Thursday, this market continued to move higher as money flowed out of equities and into the fixed income market. A new higher bottom was formed at 125'07. Upside momentum indicates that the market could test the high for the year at 128'19 over the near-term.

August Gold finished slightly lower but remained rangebound as traders assess the current trading conditions. On one hand, the bulls want to buy gold because of the weakening Dollar, but the bears want to sell gold because of the possibility of a deflationary scenario developing in the U.S. In addition, the soaring Euro may be prompting the unraveling of more Long Gold/Short Dollar spread positions. Until market conditions are clarified, I'm leaning to the short-side as the main trend is down and the market has yet to correct to the major 50% level at $1158.30.

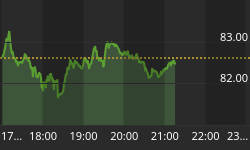

Overnight stock futures are showing slight gains. Selling in Asia and a 4.2% drop in Google stock is likely capping the market in the pre-market. News that Goldman Sachs reached a $550,000,000 settlement with the SEC has had very little impact on the market. Trading has also been light ahead of the release of earnings data from Citigroup, General Electric and Bank of America.

September Treasuries are trading flat ahead of the opening. Expectations are for T-Bond and T-Note yields to continue to drop amid concerns about a weakening U.S. economy and speculation the Fed is likely to keep interest rates at historically low levels for a prolonged period of time.

The U.S. Dollar is gaining ground against most major currencies with the exception of the Euro and the Japanese Yen. The September Euro is still showing strength due to the upbeat news regarding the Spanish debt auction. Gains could be limited if weakness prevails in the U.S. equity markets and if traders begin to pare positions ahead of next week's European bank stress test data. The September Japanese Yen is rising toward its highest level of 2010 as signs the U.S. economy is losing momentum added to speculation the Fed will leave interest rates near zero.

This morning the U.S. government is expected to announce that household sentiment deteriorated and consumer inflation fell. Both of these reports are expected to weigh on the Dollar and could trigger a decline in the U.S. equity markets once traders digest this morning's earnings news from Citigroup, Bank of America and General Electric.