Summary:

• Quick recap of things from past notes: homebuilders, brokers,Japan, et al.

• Contrarian considerations of a company going to or comingback from the grave

• Finally, we wonder about riding the brakes on auto relatedissues

A Quick Recap:

Over the past few months, the prices of homebuilder shares appear to be sinking into their foundations, and the recent fed funds rate hike added to fears that the industry will slow. The tension we guessed was building among traders seemed enough. It didn't take much for the herd to stampede after the news of a shortfall in numbers from a homebuilder like MHO - a 16 percent drop in orders in the recent quarter. We're not picking on MHO. In fact, all the homebuilders look like this. The biggest homebuilder in terms of revenue, DR Horton (DHI) reported a 15 percent rise in orders, and their shares got taken down as well. Notwithstanding recent strength and a pop-up in shares, we see the trend as down, like it or not.

Everyone now, not just us, continue to be watchful of homebuilders. Another area we were wondering about, brokers, has recent news prompting Merrill Lynch shares to decline. Merrill reported a 10 percent rise in profits to $1.1 Billion, with EPS up to $1.06 per share from $1.00, but below analyst estimates of $1.09 per share - due in part to a 44 percent drop in trading revenue. Merrill would also chase hedge fund prime brokerage business, and build up its forex and futures businesses - which helped earnings at firms like Goldman Sachs and Morgan Stanley. (We fear what the consequence will be, are hedge fund-related revenues part of the latest crop of inflating assets which liquidity has been drawn to?) June has proven to be a tough month for business and it may be so for more than just this mega-broker. Is it all just part of a summer slowdown?

The parliamentary elections in Japan were unfavorable for Prime Minister Koizumi, when the Liberal Democratic party failed to achieve its goal of 51 of the 121 seats available. Koizumi's popularity has dropped from 90 percent when he first got the job down to 40 percent, a sharp reduction in the political arsenal that helped his attempt at structural reform. While changes in the upper house won't change the government, it may tip the direction voters may lean towards for general elections in 2007, if they don't see results. Traders in Yen looked on the bright side of the election, ignored the pension fund contribution scandal overshadowing Koizumi, and bid up the currency after the election. In addition, the Bank of Japan also issued its view that "solid" growth would likely exceed forecasts. We're not sure if this is more "solid" than the last time it expressed such optimism in 1997, but we will go with the price direction. We offer updated charts below. We'll be watchful and wonder if the trends we identified are still in place for equities and the Yen. As for our currency, official numbers recently released for May 2004 show that the US trade deficit narrowed, courtesy of export growth, from $48.1B to $46B. Our concern about the overhang on the US dollar remains in place.

The deal beween OMI and Stelmar Shipping appears officially dead. We had noted this a few market notes ago when we made an observation of the dip we saw in the Baltic Dry Index. Jilted suitor OMI will focus on the ships it is acquiring from Athenian Sea Carriers and Arcadia Ship Management, and move away from what it characterized as the Stelmar board's "complete unwillingness" to consider a deal.

Contrarian Considerations:

In the aftermath of the fed funds rate hike, we also observe a brief glimmer of hope for the homebuilding crowd, given recent action in the bond traders, particularly the biggest of them all, Bill Gross of Pimco. It was reported a couple of weeks ago, that having figured the hysteria (which we still feel admittedly) about the deficit, over foreign creditors' exposure to Treasuries and inflation, was priced in, Pimco bought two and five year notes and sold European paper. His team's first apparent turnaround in its stance in a year, going long for what they see as a "value" proposition, may help characterize that our alarm is premature. Their preparation for a secondhalf moderation in growth means they see both lower inflation and therefore lower odds for aggressive Fed rate policies. We see little point in fading this team's trades, but we will continue to fret, even if it seems that the yield curve will flatten thanks to lower growth prospects, in light of the recent lower volatility in the bond markets. Pimco leads us to reconsider how this will resonate as far as housing and credit are concerned, about which quite a few folks still fret. Included is an updated chart of the MBA index refinancing index. There was a pickup in recent activity which has fallen again. We don't know if there is a bullish change in the fixed income arena, but it may be part of the saw-tooth wrangling that goes on as markets adjust to new realities like the start of a possible rate hike trend, which appears to be unfolding at a pace slower than we anticipated. Mr. Gross' contrarian value call looks right, but we're also fixated on the lower volatility which feels like the calm before a storm.

Speaking of things contrarian, we unofficially usher in an attempt to start a separate look at ideas from a contrarian point of view, which we plan to post in the future as a separate edition of market notes. In the last few months, we have followed the news regarding the vagaries of the tussle in Russia over Yukos, one of the big players both in Russia, and on the global energy market. We were tempted to consider a contrarian tack in the action but we have to remember the recent tragic killing of Forbes' Russian editor. We last read that the car involved in the killing was found but not the killer. Balancing the value of the energy reserves versus the sovereign risks, displayed by the recent power play between the State and the Company, represents the trading story. We thought about the possible turnaround or concession that could recover value, but perhaps its best left alone for now.

Speaking of contrarian, we were chagrined in part to be too late to mention a more than passing interest, and most decidedly anti-herd, in MCI (MCIP is the new ticker). Yes, that MCI, that once strode as a titan in the mega-cap leagues, as Yukos still does on its home turf (for now). We were piqued by all the sturm and drang about the death of the rebirth of MCI. We were expecting people to sagely comment that the post-Chapter 11 recovery would be followed by a sequel default, a "chapter 22". But we saw potential value there. Unfortunately (or fortunately for those like minded), so do firms like Leucadia National (LUK), among the most astute value and distressed investors around. Right after we were wondering how to mention this in a separate document, our tentatively entitled Contrarian Market Note, word got out that LUK was asking regulators for permission for possibly acquiring half of MCI. If you feel like a low risk way to play MCI, if the margin of safety in the shares isn't visible by your estimation, perhaps its best to consider going long LUK instead, assuming they buy MCI.

We were in word, bummed. We were hoping to start our first Contrarian Market Note with a quick and dirty look at MCI. Value investors Fairholme Funds, another group of astute investors, also saw value, did their homework and went long the bonds and now have the new shares. Their assessment of the viability of MCI came from their guesstimate that MCI contracts in the business and government clients were cause for going long. They also own LUK shares, courtesy, we believe, of an earlier acquisition of WilTel bonds, another distressed "new economy" broadband play. Perhaps we can consider looking at this from a trend-trading perspective strangely enough, as LUK awaits permission to make another potential purchase. We leave you with charts of LUK and MCIA, and caution.

Taken for a Ride? Riding the brakes with auto-related shares

We close this market note with consideration of securities at the intersection between automobiles and retail, and that would be car-makers and sellers. Shown below are a few charts of the action already in progress in these shares, and its possible that more is to come. We write as quarterly earnings dominate the readers' attention. We suspect, as usual, that we'll go to the bottom of the pile, but at least we'll make the cut (for recyling at the bottom of bird cages as people focus on heading out for summer vacations). The recent survey of Americans mentioned that for the summer, fifty percent of the surveyed look forward to traveling. That may be a prop for some auto and retail stories but the longer term trend may not be as sunny as the vistas hopefully to be enjoyed by vacationers. The survey we read about noted that a minimum trip of 75 miles with cash used for most expenses, and not credit. Something like 70% of those with 75k+ earnings are looking forward to a trip. Happy trails and send us a postcard.

An observation about the carmakers starting an ascent up the mountain of growth imagined in China: The potential value of the Middle Kingdom for four-wheeled wonders is understandable, given the tremendous growth, while the US market is propped up by zero percent financing and cash incentives. With the apparent recent historical US auto sales bumping up against 16-17 million units, supported by aggressive loosening of credit, the future sales question may not be solved by China quite yet. There is slowing in China, perhaps temporary in our mind, but very real - so rescue from abroad will not be soon or great enough. Recent releases from the China Association of Automobile Manufacturers point to the slowing, with a 2.2 percent rise year over year for June car sales, the lowest increase in over two years. Auto loans used to finance purchases, have dropped from about 40 percent of sales a year ago to 10 percent. As most readers are well aware, the average U.S. auto sales volume since 2002 has been around 16.7 million but the seasonally adjusted annual rate dropped to 15.4 million units. Facing overseas competition, the gradually rising credit cost environment, and any resurgence in energy costs, its no surprise that the incentives have to be maintained. No quick rescue from the East.

In contrast to the slowdown in performance, what is not ending are incentives. For June 2004, GM attempted a less tempting customer loyalty program, causing a 15% drop in sales. We read that Autodata, a vendor tracking auto industry sales and incentives, reported that GM incentives on average declined from $4,325 in May to 4,091 in June. Average incentives, from Ford in the same periods, rose from $3,515 to $3,679 but to no avail. Early July, the big 3 US makers reported sales declines, hence the recent incentives reported, which we mention in this note.

In contrast, the big 3 Japan makers (Toyota (TM), Honda (HMC) and Nissan (NSANY)) reported better business, bolstering our views from prior notes about trends for Japan. Nissan reported a 9% rise in sales in June, Toyota managed 5.2% and despite a 1.1 million vehicle recall for transmission repairs, Honda reported a 1.1% increase in sales. Two disparate data points include the 19% year over year drop we read about for SUV sales in June 2004 and the 200% rise in sales for Japanese hybrid car Prius ("Only" 4,219 units, but it's a start.)

At home market share has been reduced, while lower margins from the cost of incentives may add insult to injury. Further "slights" to the margins will come from such things as GM cutting of lease payments by up to $1,500 on some models. We guess offers such as paying $250 to those who test-drive and still buy a competitor's car were losing bets on consumer behavior - as GM attempted. GM's sales dropped 15.5% versus a year ago. Ford's sales, for the twelfth time, fell, with sales dropping 17%. Pulling ahead, DCX reported a ninth month of sales increases, 5.2% year over year, thanks to bold offerings like the 300C sedan. Right now, available until August, GM's zero percent financing can be up to 6 years for 2004 SUVs, trucks, and we read of $4,000 cash back or zero percent for up to 5 years for passenger vehicles, with deals for some 2005 vehicles ready. Ford also has hefty cash back deals and zero percent financing. We almost feel tempted to run out and get something.

We anticipate a pop-up in July sales as a result of incentives, but can the carmakers keep it up? The April inventory accumulation was followed by May incentives and production cutbacks, so we would not be surprised by a repeat. The Big 3 will not be alone, as Volkswagen, with a 12% drop in June sales reported year-over-year, has joined the financing fray for the first time with zero percent financing for Jetta and Passat models. (Hurry, the offer stands until July 31.) A contrarian indicator for the automakers, perversely enough, in our eyes popped up when we saw the relatively low favor Ford shares had among analysts, at 30%, and 25% for GM. (Where was this kind of caution a few years ago?)

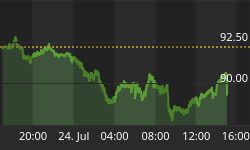

With the depreciation of new cars triggered as a buyer drives the new ride off the lot, perhaps the consumer is better off with used cars. So what then for Carmax (KMX), Autonation (AN) and United Auto Group (UAG)? On average, we observe that new vehicle can lose 20%+ in the first year, followed by 15% in year two. Considering a used car as the new car or avoiding the replacement of the old ride through repairs and upkeep, seems worthwhile given the prospect of servicing new car payments, even with 0% financing, but we're not so sure about the shares. We read that commercial truck sales are picking up. Heavy-duty trucks points to increased commercial activity and spending, but we are still troubled by the weakness of non-commercial buyers of vehicles. Hence, our quick look at car-sellers. Autonation (AN) could be considered one of the bell weathers of the sector, and does seems structured to become a successful model, but recent events point to overall weakness from car-buyers.

AN reported lower sales volume, with Q2'04 earnings ratcheted down to $0.34 - 0.35 per share from the earlier corporate guesstimate of 0.38 - 0.40 per share. Some of the braking is attributed to weakness related to Ford and GM dealerships. AN has also reversed itself, pulling back full year earnings per share to $1.40. The ostensibly cheap p/e in car-makers exists within a context of liquidity boosted consumer spending over these last few years. The low multiples point to the also low margins in the business. What could happen were the Fed tap the brakes lightly at its measured pace over the next few quarters? What will the impact be for the 365 AN dealerships? Lower sales volume, as indicated for June, higher inventories, pushed down gross margins, are just a start. Used carsellers and car parts shares may need be in need of repair. As in past market notes, we show a few charts to broach the subject.

(A minor detour: The Financial Accounting Standards Board (FASB) proposed including the earnings impact of contingent convertible, or "CoCo" bonds. Holders can convert the CoCos to shares usually when the related equity rises by a certain amount higher than the conversion price. GM has about $8B of these bonds and we read that an adoption of this rule, perhaps by early next year could mean a hit to EPS of about $0.80 -0.90 against the full year 2004 EPS estimates of about $7.00, but without cash charges. GM's 8B in CoCos, half of which was issued for funding needs at the pension fund, could become 140+ million shares.)

Last metrics and parting thoughts:

In keeping with the sentiments expressed by Gross and Pimco, June producer prices were reported as falling. Overall producer prices dropped 0.3 percent (following a 0.8 percent srise in May) and excluding food and energy costs, the core figure rose 0.2 percent. Expectations for the overall producer price index and the core number, were for a rise of 0.2 percent for June. Over the past year, producer prices have risen 4 percent. At the same time, industrial production dropped 0.3 percent for June (and the May increase was revised down to 0.9 percent), but business inventories rose for a ninth month in a row in May indicating business optimism. Retail sales fell 1.1 percent in June, the biggest dip since February 2003, and unsurprisingly auto sales were the culprit. ISM non-manufacturing index data indicated new orders and employment elements were up but that the overall ISM index still fell from 65.2 to 59.9, from May to June 2004. Layoffs planned declined, but so did planned hiring. While a 50+ rating on the index is still a positive indicator, these type of numbers do not reassure us.

Lastly and most significantly for this Market Note, average incentives for vehicles sold in the US rose 4.7% from a year ago (to $2,747), according vendor Edmunds, and yet sales in the US dropped 2.0%.